Liberation (or rather Retro) Day - some initial thoughts

Every so often the US casts its mind back to the 1950s it seems (eg American Graffiti and Happy Days in the 1970s) and so it is again!

Here are some initial thoughts on Trump’s tariff announcements:

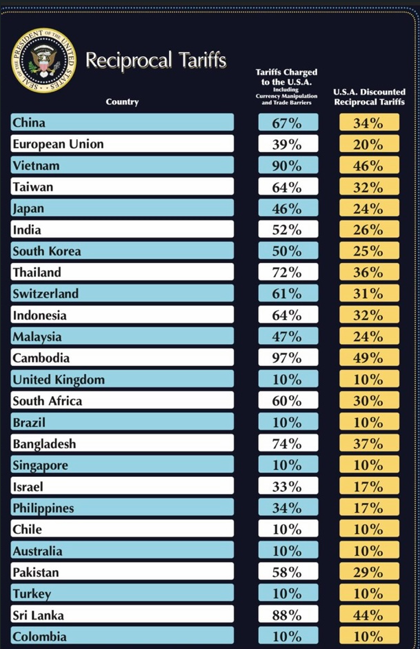

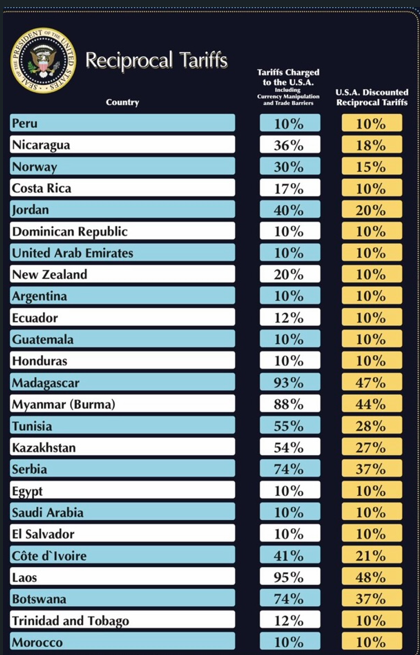

Basically, Trump is putting a 10% tariff on all imports from all countries (except those imports already hit from Canada and Mexico and autos, steel and aluminium which have their own tariffs and sectors like pharmaceuticals and copper which will likely see their own tariffs) but higher reciprocal tariffs on many countries to offset the Trump Administration’s calculation of what barriers US exports to those countries face. This appears to allow for tariff but also non-tariff barriers, manipulated exchange rates, bio security laws and VATs/GSTs (which Trump mistakenly sees as protectionist).

It's all a bit confusing given the way it's been presented, eg China at 34% in the big table, but it's really 54% based on comments by Treasury Secretary Scott Bessent

Never miss an update

Get the latest insights from me in your inbox when they’re published.

Advertisement

But overall it looks worse than markets expected with 10% on all countries and much higher rates on many. While some countries may be able to negotiate the reciprocal tariffs down many won’t eg if they cover things like VATs/GSTs which are not protectionist or valid biosecurity laws.

And there is still more sectoral tariffs to come, including on pharmaceuticals.

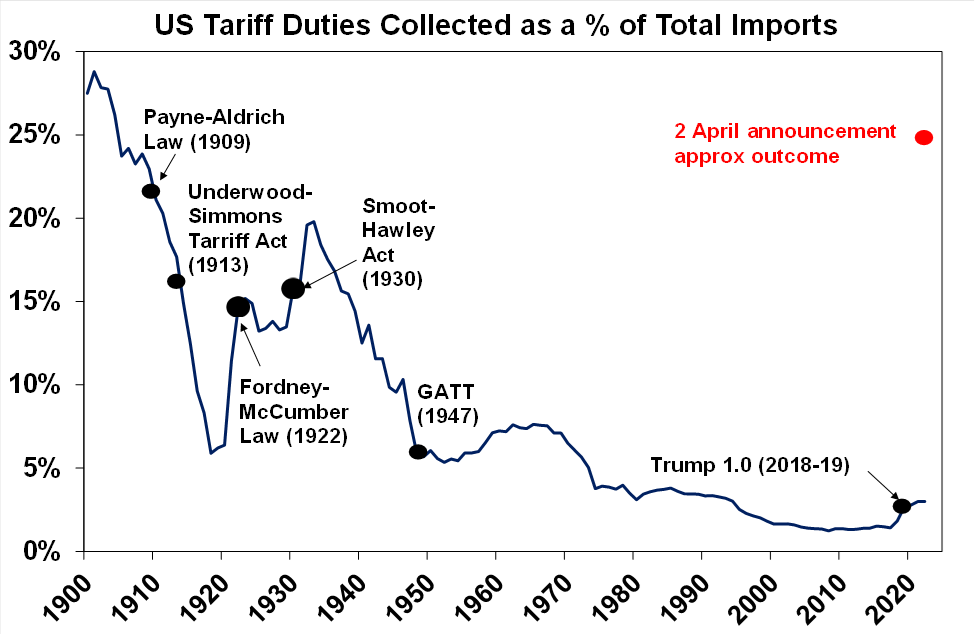

Our rough calculation is that the 2nd April announcement will take the US average tariff rate to above levels seen in the 1930s after the Smoot/Hawley tariffs which will in turn add to the risk of a US recession – via a further blow to confidence and supply chain disruptions – and a bigger hit to global growth. The risk of a US recession is probably now around 40%, and global growth could be pushed towards 2% (from around 3% currently) depending on how significant retaliation is and how countries like China respond with policy stimulus.

For Australia, the 10% tariff is bad news for the industries affected. Pharmaceuticals (worth $2bn a year) are not currently included but look likely to see their own tariff down the track. However, only 5% of Australian exports go to the US, worth about 0.9% of GDP, and much of this will still continue, albeit they are now more expensive in the US. So all up the direct hit to GDP growth is probably around just 0.2%. However, the bigger threat comes from the threat to global growth, particularly in China and Asia, which will likely result in less demand for our exports.

Assuming that Australia does not retaliate and the $A does not crash then Trump’s tariffs pose more of a threat to growth than causing higher inflation here and so add to the case for more RBA rate cuts.

Given the even bigger threat to global growth it looks like share markets will have a further leg down. Consistent with this US futures are now down 3.5%.

Our assessment remains that shares will have a 15% plus correction measured from this year’s high. A 10% fall in US shares was not enough to put pressure on Trump but a 15% plus fall likely will at some point resulting in some moderation in the tariffs and refocus on the market positive aspects of his agenda (like tax cuts and de-regulation). And eventually the Fed will likely respond with rate cuts, although this may be delayed given US tariffs will also add to US inflation.

This in turn will then create buying opportunities for investors as shares had become a bit overvalued, but there may be a way to go yet.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision, please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

3 topics

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Expertise

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Investing like Warren Buffett in an uncertain market

Livewire Markets