Liquidity crisis shocks investors

Unlisted property and debt markets are facing a huge liquidity crunch

In the AFR I write that the commercial real estate market, and the non-bank lenders that finance it, face burgeoning liquidity crises. This echoes similar dynamics playing out in the commercial property and sub-prime corporate lending sectors overseas.

Investors say many unlisted property trusts are now being frozen as investors rush for the exits, while the fund managers that operate these trusts are reluctant to sell the underlying assets to liberate their clients’ money because they know the prices they would obtain for these properties would be miles below their inflated NTAs.

A derivative issue is that a 20 per cent to 30 per cent reduction in official NTAs would force many properties’ loan-to-value ratios to leap to levels that would threaten to breach these funds’ internal leverage targets and their lenders’ debt covenants, which could precipitate defaults and forced sales, driving prices down even further.

Never miss an update

Get the latest insights from me in your inbox when they’re published.

Advertisement

Similar challenges have emerged in the US and European commercial real estate and non-bank lending markets. Brand-name REITs have gated investor withdrawals. And large global fund managers are defaulting on their commercial property loans.

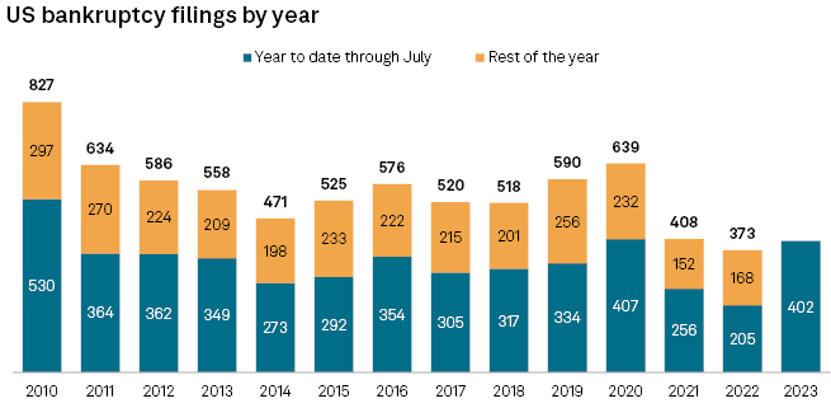

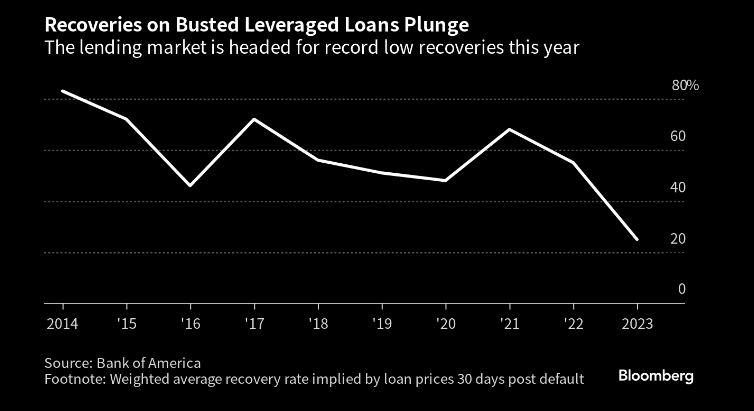

Even in the ostensibly strong US economy bankruptcy filings are on track for their worst year since the global financial crisis. As corporate defaults soar, the recovery rate on non-bank loans to these companies, known as “leveraged loans”, has plunged to the worst level on record.

The chief financial officer of a commercial property group wrote to me to relay his own anxieties about his industry and the non-banks that finance it.

“I have been concerned for a number of years that investors in funds [lending to commercial property] are not being adequately compensated for the risk they are taking,” he wrote.

“My view is that this is further increased by concentration risk as often these loan books and associated businesses are not diversified and heavily overweight residential property developers and commercial property (similar to the industry-specific exposure of Silicon Valley Bank).

“A number of these funds are currently experiencing liquidity issues due to severe construction delays, which are delaying settlements on residential projects and the subsequent repayment of [their] loan facilities.

“The problem downstream is that these non-bank lenders have unfunded commitments on other development projects as they were expecting to be able to recycle these loan repayments. As these trusts are not APRA regulated, diversified, and do not hold sufficient liquidity buffers, they are not adequately capitalised and have been approaching large family offices for emergency funding.”

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

........

Investment Disclaimer

Past performance does not assure future returns. All investments carry risks, including that the value of investments may vary, future returns may differ from past returns, and that your capital is not guaranteed. This information has been prepared by Coolabah Capital Investments Pty Ltd (ACN 153 327 872). It is general information only and is not intended to provide you with financial advice. You should not rely on any information herein in making any investment decisions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. The Product Disclosure Statement (PDS) for the funds should be considered before deciding whether to acquire or hold units in it. A PDS for these products can be obtained by visiting www.coolabahcapital.com. Neither Coolabah Capital Investments Pty Ltd, EQT Responsible Entity Services Ltd (ACN 101 103 011), Equity Trustees Ltd (ACN 004 031 298) nor their respective shareholders, directors and associated businesses assume any liability to investors in connection with any investment in the funds, or guarantees the performance of any obligations to investors, the performance of the funds or any particular rate of return. The repayment of capital is not guaranteed. Investments in the funds are not deposits or liabilities of any of the above-mentioned parties, nor of any Authorised Deposit-taking Institution. The funds are subject to investment risks, which could include delays in repayment and/or loss of income and capital invested. Past performance is not an indicator of nor assures any future returns or risks. Coolabah Capital Institutional Investments Pty Ltd holds Australian Financial Services Licence No. 482238 and is an authorised representative #001277030 of EQT Responsible Entity Services Ltd that holds Australian Financial Services Licence No. 223271. Equity Trustees Ltd that holds Australian Financial Services Licence No. 240975.

Forward-Looking Disclaimer

This presentation contains some forward-looking information. These statements are not guarantees of future performance and undue reliance should not be placed on them. Such forward-looking statements necessarily involve known and unknown risks and uncertainties, which may cause actual performance and financial results in future periods to differ materially from any projections of future performance or result expressed or implied by such forward-looking statements. Although forward-looking statements contained in this presentation are based upon what Coolabah Capital Investments Pty Ltd believes are reasonable assumptions, there can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Coolabah Capital Investments Pty Ltd undertakes no obligation to update forward-looking statements if circumstances or management’s estimates or opinions should change except as required by applicable securities laws. The reader is cautioned not to place undue reliance on forward-looking statements.

4 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Investing like Warren Buffett in an uncertain market

Livewire Markets