Macquarie hybrid soars, Genworth pulls bond issue, and housing bears run for hills

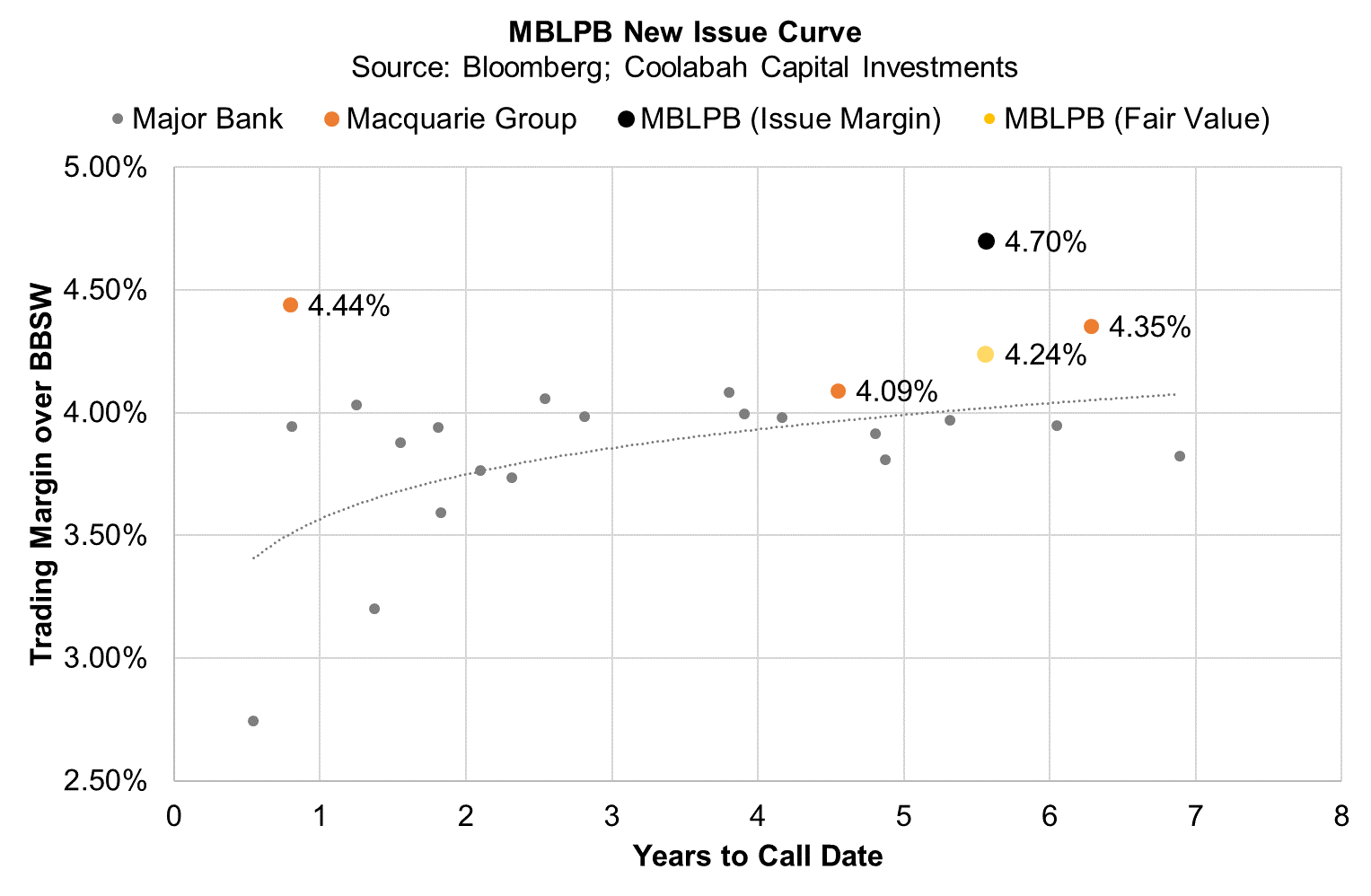

As we had projected here days ago, Macquarie's new hybrid security (ASX: MLBPC - it was initially marketed as MBLPB) listed on the ASX at a massive premium to face value, trading up from its $100 issue price to as high as $103 (we bought a decent chunk in the original deal). That represents tremendous spread compression from the issue margin of 4.7% above the quarterly bank bill swap rate (BBSW) to around 4.1% (ie, a 60 basis point reduction). Regular readers might recall that I recently presented our analysis forecasting that MBLPC's price would rise from $100 to up to $102.57, and it did not fail to disappoint. Specifically, I wrote:

Based on Friday's ASX pricing, it looks like the interpolated credit spread for MBLPC would be around 4.24% above the swap rate (given it sits between two other Macquarie Group hybrids---MQGPC and MQGPD---in terms of tenor), which suggests a clean price of about $102.11 (or a capital gain of more than 2% above its $100 face value) in lieu of the 46 basis points of prospective credit spread compression from the 4.7% issue margin...

If investors were to price in this superior creditworthiness (ie, the higher rating) by, say, reducing MBLPC’s trading margin 10 basis points tighter than its currently interpolated spread using the Macquarie Group hybrid curve (ie, down from 4.24% to 4.14%), this would increase the expected clean price $0.46 to $102.57.

While MBLPC now seems fully priced on a relative cross-sectional basis, we believe there is still a lot of upside on a bottom-up outright fundamentals basis given our expectation that the major banks' five-year hybrid curve will compress towards its pre-crisis levels around 270bps over BBSW (vs current levels at circa 394bps). Assuming, for example, an 8.8% probability of default and a 0% recovery rate, we have the minimum fair value required return for a five-year major bank hybrid at about 184bps over BBSW before any considerations around liquidity risk premia.

Genworth First Loss Piece Pulled

The other big news yesterday was that the mortgage loss insurer Genworth was forced to pull its Tier 2 subordinated bond issue even after the joint lead managers had confidently broadcast that there was $200 million of indicative interest for the deal at a proposed credit spread of 500bps over BBSW. We had zero interest for two reasons:

- In contrast to all other Tier 2 bonds issued by listed banks, Genworth's security does not convert into its listed equity in a default event (specifically, when APRA declares that Genworth has reached the point of non-viability). Instead, this security bizarrely gets zeroed, or written off completely. Genworth had previously issued equity-converting Tier 2, but moved to the full write-off structure with their previous issue. When I quizzed the company at the time on why they would not allow the bond to be converted into equity in default (as had previously been the case), I was told that Genworth's largest shareholder, its US parent company, did not want to suffer equity dilution in such a scenario. In short, Genworth is saying that it wants bondholders to be wiped out before its shareholders have to wear any pain, which means that Genworth's Tier 2 bond is effectively subordinated to equity. It is therefore the first-loss piece;

- This brings me to my second concern. Genworth is providing first-loss insurance for residential mortgage lenders in the event their borrowers default and cannot repay their loans. Setting aside debate around the state of the housing market right now (see below), we know that the first loss equity tranche in warehouses funding home loans are generally demanding returns of around 10%. So why would anyone be stupid enough to accept a 5% return from a the first-loss equity tranche that is effectively going to be forced to wear all the risk in any non-viability event? The obvious answer is that when investors really thought about it, they decided that was indeed a dud trade at its proposed price. If Genworth were to re-rack the spread wider to, say, 1000bps, I might have interest.

Housing Bears Running for the Hills

Yesterday we had the first of the housing bears caught in our cross-hairs: the once-grizzly UBS conceded:

"Looking forward, we had expected home prices could drop 10%, but it could be smaller now. We await policy details to review our outlook"

Yeah, the bears are gonna start running for the hills when they realise the wolverine is about to BBQ them. Expect lots of moaning, groaning and endless excuses. They will all likely roll out the ole "Steve Keen". "Oh, but if it were not for low interest rates and stimulatory fiscal policy and other counter-cyclical stuff, we would have been right!"

Another housing bear started to get the willies today. AMP's Shane Oliver writes:

"When we first looked at the impact of the intensifying shutdown of the Australian economy on the housing market...the risk was that a deeper downturn with say 10% unemployment could see a 20% fall in prices". Oliver continues: "Subsequent government support measures along with an earlier reopening of the economy have reduced the risk of worse case scenarios for home prices. Our worst-case scenario for a 20% decline in prices and those of others seeing 30% plus falls are unlikely thanks to support measures and the earlier reopening of the economy."

But this particular grizzly is still putting up a fight, concluding, "Our base case is for national average prices to fall around 5-10% into next year."

In more bad news for the bears, CoreLogic's daily index has increased for two days consecutively in Sydney, Melbourne and across the 8 capital cities (yes, I know that is not much to get excited about)...This debate is ultimately an empirical question, and I am having fun with it in the meantime!

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

........

General Disclaimer:

Past performance does not assure future returns. All investments carry risks, including that the value of investments may vary, future returns may differ from past returns, and that your capital is not guaranteed. This information has been prepared by Coolabah Capital Investments Pty Ltd (ACN 153 327 872). It is general information only and is not intended to provide you with financial advice. You should not rely on any information herein in making any investment decisions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. The Product Disclosure Statement (PDS) for the funds should be considered before deciding whether to acquire or hold units in it. A PDS for these products can be obtained by visiting www.coolabahcapital.com. Neither Coolabah Capital Investments Pty Ltd, EQT Responsible Entity Services Ltd (ACN 101 103 011), Equity Trustees Ltd (ACN 004 031 298) nor their respective shareholders, directors and associated businesses assume any liability to investors in connection with any investment in the funds, or guarantees the performance of any obligations to investors, the performance of the funds or any particular rate of return. The repayment of capital is not guaranteed. Investments in the funds are not deposits or liabilities of any of the above-mentioned parties, nor of any Authorised Deposit-taking Institution. The funds are subject to investment risks, which could include delays in repayment and/or loss of income and capital invested. Past performance is not an indicator of nor assures any future returns or risks. Coolabah Capital Institutional Investments Pty Ltd holds Australian Financial Services Licence No. 482238 and is an authorised representative #001277030 of EQT Responsible Entity Services Ltd that holds Australian Financial Services Licence No. 223271. Equity Trustees Ltd that holds Australian Financial Services Licence No. 240975.

Forward-Looking Disclaimer:

This information may contain some forward-looking statements. These statements are not guarantees of future performance and undue reliance should not be placed on them. Such forward-looking statements necessarily involve known and unknown risks and uncertainties, which may cause actual performance and financial results in future periods to differ materially from any projections of future performance or result expressed or implied by such forward-looking statements. Coolabah Capital Investments Pty Ltd undertakes no obligation to update forward-looking statements if circumstances or management’s estimates or opinions should change except as required by applicable securities laws. The reader is cautioned not to rely on forward-looking statements.

3 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets