Mixed outlook for residential property in 2017

The downside risks relating to Australia’s leveraged property market have been well documented, with the possibility of tighter lending rates on investment loans in 2017, and an oversupply of inner city apartments looming in Brisbane, Melbourne, and potentially Canberra. That said, we’ve known about the pipeline of apartments for a long time now, interest rates remain at stimulatory levels, and well-located, established capital city property will often continue to perform well. Year-on-year credit growth pertaining to investors ticked back up to 5.3pc in October from 4.6pc in August, so there’s a possibility that APRA may need to implement further macroprudential measures in 2017, although higher lending rates for investor loans may negate the need for intervention. For now, Sydney and Melbourne still appear to be carrying reasonable momentum into the new year, as do house prices in most capital cities ex-Perth and Darwin, but the outlook for higher density and inner city apartment stock is generally less upbeat. In this wire we identify areas of value, and the data investors should be watching.

Events, triggers, or data that investors should be watching out for

Defaults on new apartment sales to non-residents have been a known risk for some time, and as such developers, regulators, and other interested parties are monitoring the volume of failed transactions closely. The federal government is acutely aware of the risks, and has recently eased rules to allow non-residents to purchase off-the-plan apartments that have failed to settle.

In terms of specific trends to watch closely, we know from international experiences in the US and certain countries in Europe that a downturn in building approvals can foreshadow an impending market correction. That is, when developers begin to doubt their ability to secure profitable sales, this can prove to be an accurate bellwether for market sentiment over the months ahead.

By way of a domestic example, detached house approvals peaked in Perth in Q4 2014 as the resources boom faded, and the house price index for that city had peaked before the next quarter was out.

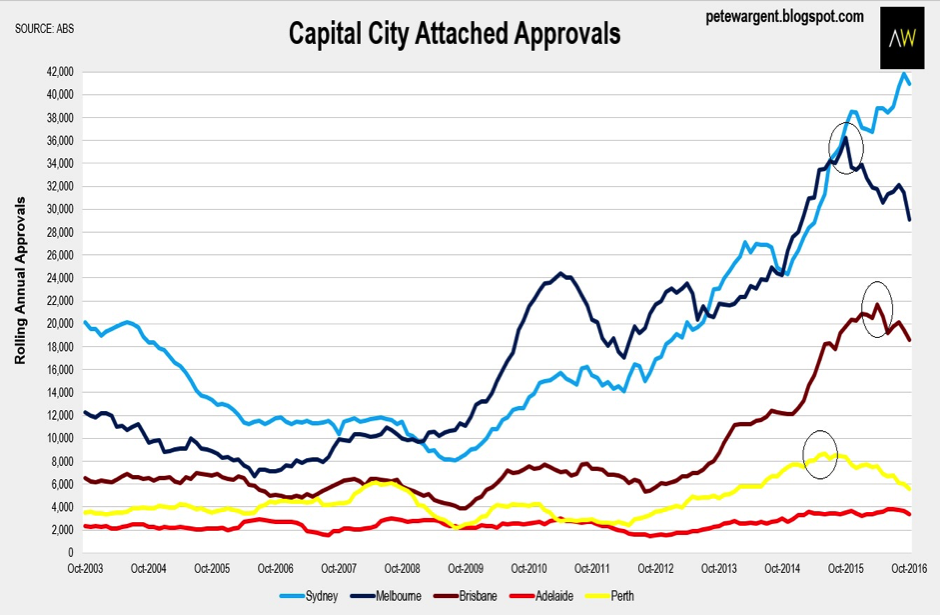

Multi-unit approvals figures at the capital city level are inevitably ‘lumpier’ by nature and can be materially skewed by occasional large projects. However, it looks to be increasingly clear that attached dwelling approvals in Brisbane and Melbourne have already peaked earlier in 2016, and are now retracing from unprecedented highs.

While there are always sub-trends and markets within markets, this looks ominous for the high-rise apartment sector in these two cities in 2017 (indeed annualised ‘high-rise’ apartment approvals for blocks of four or more storeys moved beyond their peak in all three of the most populous states during the third quarter of 2016).

In Sydney, despite something of a pullback in attached dwelling approvals in the month of October, building permits are still tracking at historically high levels. This is partly a reflection of the prolonged lull in construction prior to the recent boom wherein residential building activity in the harbour city plumbed half century lows.

Summarily, Sydney construction activity is still playing catch up for the time being, and prices may continue to rise for a while longer yet.

Sectors presenting good opportunities

Many market commentators rarely invest in property, let alone have a track record of success, and so necessarily adopt a macro view. This is useful to a point, but of course there are opportunities at the micro level if you are in the market every day.

In recent years, we’ve been looking to pick up off-market terraces in in Sydney – often in need of renovation or with the option to add an extra bedroom and bathroom - in areas such as Bondi Junction, Paddington, and especially Surry Hills, which we believed would benefit from a combination of Chinese capital and the CBD & SE Light Rail project.

In the apartment markets, for much of the last five years or so we’ve been buying in Sydney’s beachside eastern suburbs and the garden suburbs of the lower north shore, where the unit supply response has been less significant. However, after nearly half a decade of gains, we think that there is a fair chance that apartment prices in Sydney may peak within the next year.

Granted, you need deep pockets to buy in Sydney these days, but that’s not to say that opportunities don’t exist elsewhere in Australia. Through 2016 we’ve mostly been buying detached houses in Brisbane in the $600,000 to $850,000 price range, within a 3 to 9-kilometre radius of the Central Business District.

In middle-ring Brisbane, we typically source off-market houses close to train links and sought after schools, often older houses with development potential (flood-free sites only), such as those on 600+ square metre blocks with LMR zoning, splitter blocks, or simply knockdown post-war homes.

Generally, these are not high-yielding investments with gross yields typically of ~4pc or lower, but while today may not be the ideal stage of the cycle to develop a LMR site with medium density product, the option to landbank for capital growth and undertake such a development in a future market cycle can be compelling. Probably more than in any other city, in Brisbane it is vital to understand your strategy clearly, and accordingly to then buy well: the right property, in the right place, at the right price.

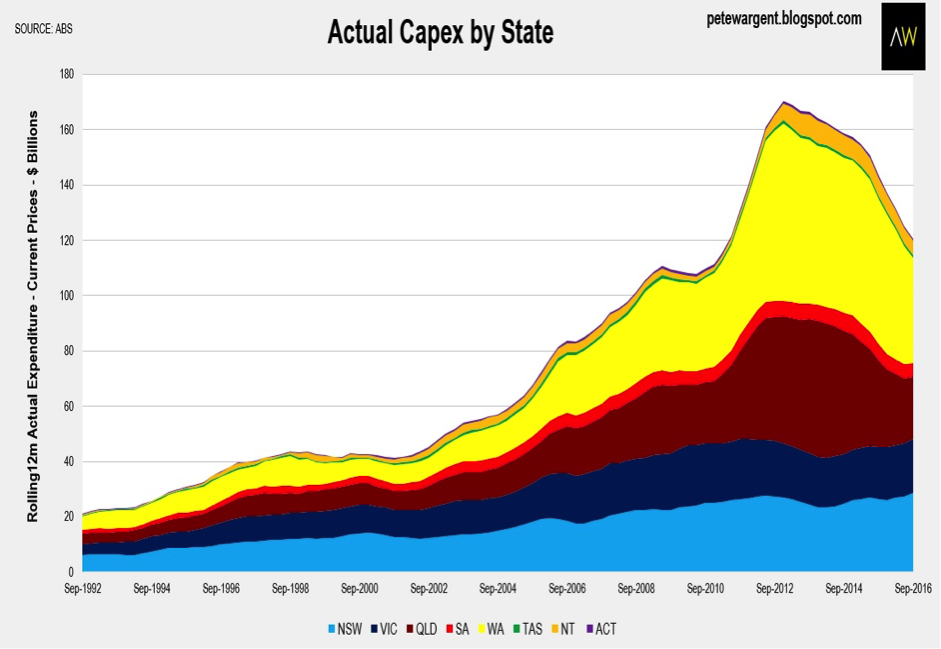

The latest private capital expenditure figures released in the past week confirmed what we already knew: that Queensland took much of its medicine between Q1 2013 and Q1 2016 as many of its larger resources projects transitioned from construction to production.

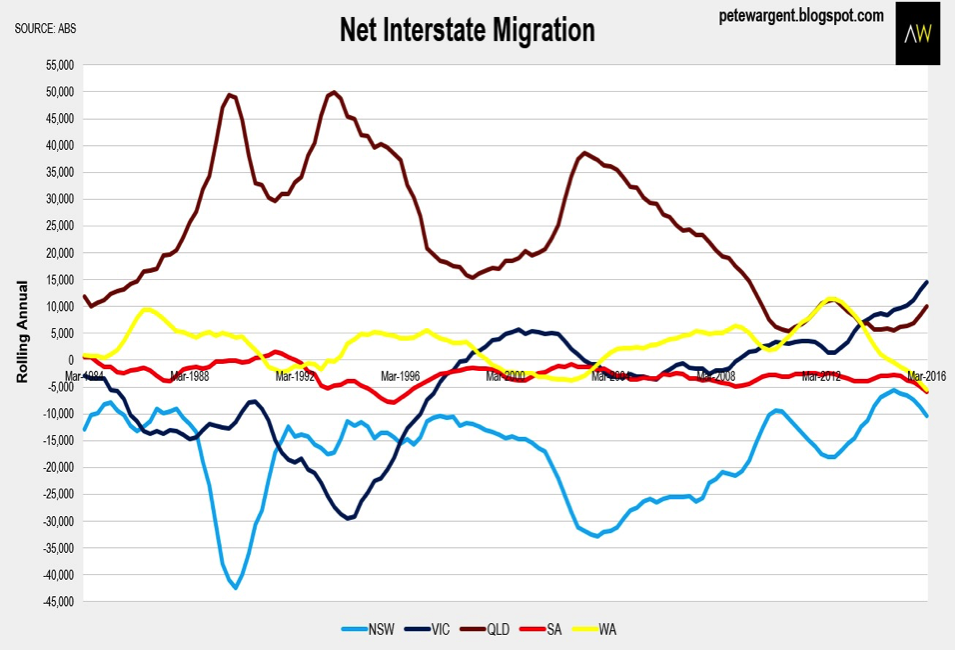

With inbound interstate migration into Queensland now on the rise again since Q1 2015 – an expected trend at this stage of the cycle as the ratio of prices in Sydney to Brisbane becomes ever more stretched - there are finally brighter days ahead for the Sunshine State, albeit with an imposing oversupply of apartments in Brisbane’s CBD and inner city fringe. A dollar-driven surge in tourism and a timely boost for coal prices are assisting the economic rebound.

For Perth, the capex figures unsurprisingly confirmed that the economic downturn will continue through 2017, with a lack of employment opportunities flipping net interstate migration in Western Australia from a strong positive to negative. Vacancy rates remain high in Perth, the stock overhang accentuated by the migration east, and rents and prices consequently remain in decline.

Victoria has benefited from the economic weakness of Perth and Adelaide to the extent that inbound net interstate migration has hit a record high, with Melbourne recording enormous population growth in 2016.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Co-founder of AllenWargent Property Buyers - "the better way to buy property".

Veteran property market analyst & investor.

4 topics

Co-founder of AllenWargent Property Buyers - "the better way to buy property". Veteran property market analyst & investor.

Co-founder of AllenWargent Property Buyers - "the better way to buy property". Veteran property market analyst & investor.

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

This recently triggered market signal has never failed to predict gains

Ophir Asset Management

Equities

How you can use AI to know when to sell

Minotaur Capital