TOL - 7th Jan, 2025

New data suggests your exposure to “overvalued” ASX bank shares is greater than you think

ASX banks are considered overvalued by most major brokers, but have delivered some of the best returns in 2024. Should you stick with them?

Aussie investors love their bank shares. In my experience as a research analyst for over 20 years, I’ve learned that when discussing bank shares with most Aussie investors, there’s really only one bone of contention – which one do I add to my portfolio? I must admit that I’ve often framed my research reports in this fashion, because I know that even if I recommended selling a particular ASX bank stock(s), that call would generally fall on deaf ears!

I’ve followed the 2024 ASX-bank share price boom very carefully this year, most recently publishing a 3-parter discussing valuations of the sector versus historical norms, major broker bank sector recommendations, and bank sector technical analysis factors. Not surprisingly, given the popularity of ASX banks with Aussie investors, they’ve been three of the most-read articles on our platform this year.

Today, I came across a fascinating research article by Morgan Stanley that considers the ASX bank sector overvaluation conundrum from a different angle: Exposure. Who’s been hoovering up bank shares in 2024, and therefore causing the overvaluations discussed in my recent articles? And more importantly – what does this mean for Aussie investors looking to grow their wealth in 2025?

Let’s investigate!

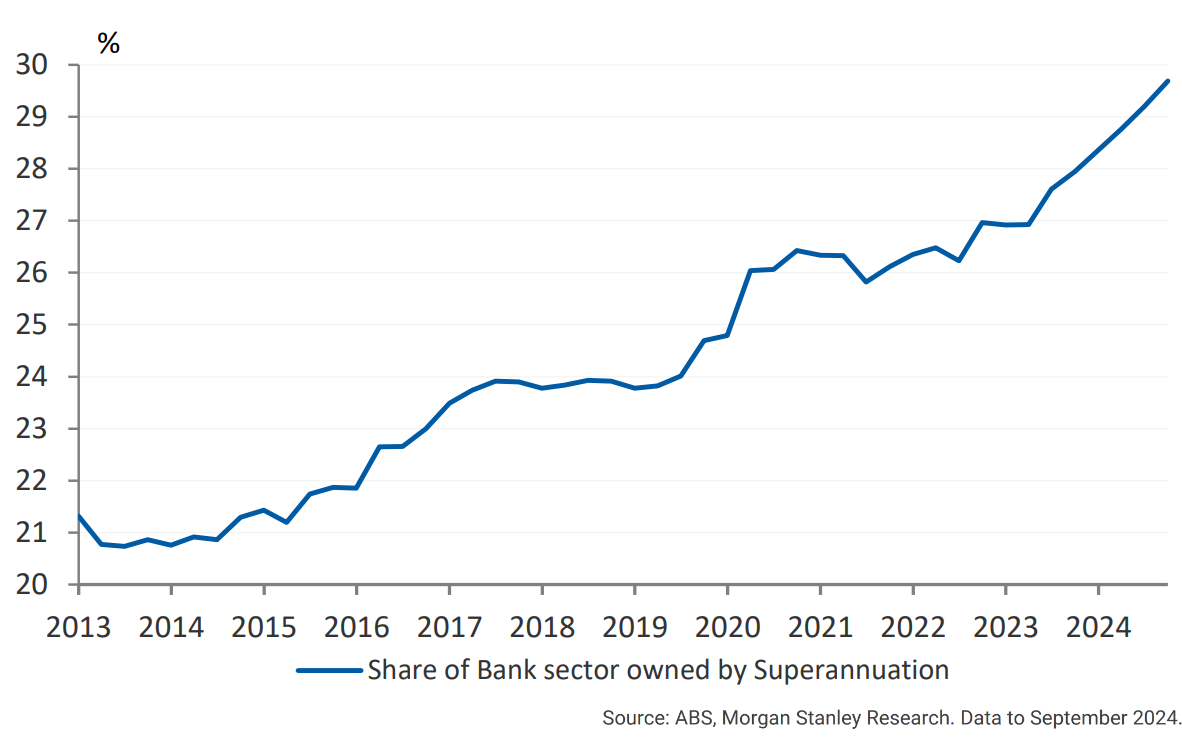

The banks’ run in 2024 really was “super”

In its latest research note on the ASX bank sector, Morgan Stanley cites new data from the Australian Bureau of Statistics (“ABS”) indicating the superannuation sector collectively now owns close to 30% of outstanding ASX bank shares, up around 2% from last year. The broker concludes that these super funds, along with passive flows from exchange traded funds (“ETFs”) are to blame for pushing ASX bank sector valuations to “extremes”.

How did we get here? Consider that super contributions from hard-working Aussies are flooding into the big super funds each day at the rate of 11.5% of our collective incomes (the current superannuation guarantee rate), and all that cash has got to go somewhere.

You’ve selected an investing option for your super, right? You know, there are low-risk options all the way up to more aggressive options?

No, I didn’t think so. Around 70% of Australians don’t make a choice, and are therefore invested in the default “balanced” option with their respective super fund. The typical balanced option invests around 40% of its capital into Australian shares.

Consider now that the major banks make up over 20% of the benchmark S&P/ASX 200, and that means billions of dollars are earmarked for investment in our bank stocks each year.

Aussie investors are also flocking index and other “high yield” ETFs that are again heavily weighted towards ASX bank stocks. It’s important to note that the Australian share component of the typical balanced super option, as well as index tracking ETFs, are “passive” investments.

This means managers of these vehicles simply aim to track the benchmark S&P/ASX 200, investing in alignment with the weightings of the constituents of the index. They do not conduct research into the valuations of the assets they are purchasing. They could be purchasing the most overvalued assets in the history of markets – and they would continue to do so – as this is their mandate.

This implies that the default option for the vast majority of Aussie investors is: Autopilot

That’s the demand side. Consider also that this autopilot investing is happening at a time that each of the Big 4 banks have either run, or are close to completing, multi-billion dollar share buyback schemes – further diminishing the supply of bank shares. Add in the fact that markets are rising, implying there are fewer shares available for sale more generally.

Demand versus supply. It’s the oldest relationship in economics, and the upshot is bank share prices have rocketed in 2024. According to the major brokers (see article 2 above!), the current environment of massive demand for shares of ASX bank stocks versus their limited supply is pushing valuations in the sector to record high multiples – by several standard deviations from the mean in some cases.

All you can eat and then some…

That’s all good news, right? I mean ASX bank stocks are going gang-busters, and if you’ve checked your super account balance lately, there’s very little reason to complain.

Yes and no. 🤔

The major implication for investors is this: Even if you don’t own bank shares directly, your super fund probably holds them on your behalf in substantial quantities. You are exposed to their current overvaluations (assuming the major brokers are correct).

If you do own bank shares directly in a portfolio outside of your superannuation guarantee-linked superannuation fund – you’ve potentially got substantially greater exposure to their overvaluations than you may have realised.

Either way, nearly everyone reading this sentence has some skin in the game if valuations in the ASX bank sector revert to historical norms.

This can happen in two ways:

- Either ASX bank sector earnings increase dramatically to improve valuations (this is not generally forecast by the major brokers); or

- ASX bank sector share prices fall substantially (this is generally forecast by the major brokers via their current target prices – again see article 2 above!).

Many professional investors consider it prudent to rebalance one’s portfolio periodically as the relative ratios of the stocks and or sectors they own changes due to share price movements. For example, if they find that an investment in one stock or sector has become substantially overweight relative to the benchmark weighting due to strong performance, they may sell down that holding(s) and redistribute the capital across other stocks or sectors.

Investors have a choice whether to stick with their current bank exposure in 2025 and trust that the prevailing environment of excess demand for their shares will continue, or rebalance in favour of beaten-down sectors such as Resources and Energy, which the major brokers generally consider to be closer to their long-run valuation norms.

Warnings from the regulators

According to Morgan Stanley, the heavy concentration of investor exposure to ASX bank stocks, has caught the attention of both the Reserve Bank of Australia (“RBA”) and the Council of Financial Regulators (“CFR”), who have each recently warned of possible stability risks.

The broker notes that regulators are concerned super funds have too much exposure to both debt (i.e., by buying bonds and other fixed-interest assets the banks issue to assist with their funding) and equity (i.e., shares) of ASX bank stocks. An APRA review slated for 2025 will examine whether superannuation ownership levels could pose systemic stability issues.

Warnings from Morgan Stanley

Morgan Stanley poses the following key risks for the sector, and for Aussie investors going forward:

- Current price-to-earnings multiples are around seven times above the long-run average, and dividend yields have compressed significantly.

- If regulators intervene with respect to super fund ownership levels – bank stocks could face a valuation reset.

- More generally, a slowdown in super fund or passive fund buying could trigger a marked de-rating if other active investors are not prepared to step in at these prices.

Conclusions

Australians’ super funds have grown into major owners of ASX bank stocks, resulting in everyday Aussie investors accumulating considerable exposure to the sector – whether they realise it or not.

Morgan Stanley’s analysis points to the substantial role that the super industry and passive ETFs are playing in propping up historically lofty valuations across ASX bank stocks. These high multiples and the concentration of ownership are attracting regulatory scrutiny – which poses its own set of risks for sector valuations.

Any regulatory shifts or a reduction in super fund net buying, could see a notable recalibration of bank share prices.

Given these risks, it is essential for investors to understand how much exposure to ASX bank stocks lies under the hood of their chosen super option, and consider this alongside any direct investments they may hold.

This article first appeared on Market Index on Tuesday 24 December 2024.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

{kind=link}

{kind=link}

5 topics

8 stocks mentioned

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

What a 40% year taught us: 4 lessons from the past 12 months (and 3 new stocks to buy)

Seneca Financial Solutions