Opening the door to income

Australians have a love affair with property. But there are a number of ways to own property – and earn an income from it. Two of these include listed real estate investment trusts or REITS and unlisted property funds.

Most REITs were in good shape as COVID-19 hit but that doesn’t mean all property classes have performed the same. Retail has taken a significant hit thanks to the ongoing lockdowns and the acceleration of ecommerce, while offices, warehouses and healthcare facilities are still showing strong demand.

Individual real estate assets attract varying levels of income, so investors need to be selective when choosing their investments. Here, I discuss the differences between REITs and unlisted funds, and give a rundown on which sectors look set to shine

Two ways to invest

For the past five months, Australia has experienced an historically low cash rate of 0.25%. While low rates are great for variable household mortgages or other loans, they are wanting for savings accounts, term deposits and any other cash-related investment vehicle.

Across the four major Australian banks, interest rates paid on term deposits held for 12 months and payable on maturity, averaged 0.85% (1). So investors with these types of income-investments might prefer to seek alternative vehicles, such as commercial property, to generate revenue and, subsequently, pay regular, higher returns.

There are two typical ways of investing in commercial property, outside of owning an asset outright: through listed or unlisted funds.

Listed Funds

Property funds listed on an exchange are referred to as Real Estate Investment Trusts (REITs) or Australian REITs (A-REITs). Investors can buy or sell their shares in these funds at any time. This makes them highly liquid.

Unlisted Funds

Unlisted property funds are entities not available on a security exchange, such as the ASX. They are often referred to as property syndicates as they involve the syndication of ownership of a single property or group of properties, to investors. Unlisted funds specify the period an asset or assets will be owned – usually five to seven years – and typically provide monthly or quarterly returns (distributions) based on the net rental income received from the tenants. The fund's assets are typically divested at the end of the term and the funds are returned to investors. There is also the potential for a capital gain.

Property funds can also be closed or open-ended.

Closed-ended means the number of units in the fund is fixed. No additional units are issued or redeemed during the term of the fund. This type of fund generally has lower volatility than a listed fund as the assets are usually valued once or twice a year and the unit price is updated at the time of valuation.

Open-ended funds are similar, except investors can enter or leave the fund during the duration of the fund, when there is a liquidity facility in place. Investors can withdraw their investment at designated intervals, usually monthly or quarterly.

Key Metrics

When deciding which property fund is best for you, there are several key metrics to consider. These are the drivers that can deliver stable rental income and, therefore increase the likelihood of attractive returns. They include:

- Weighted Average Lease Expiry (WALE).

The average number of years a property has secured a tenant(s). The more years the better, as it provides greater assurance of rent revenue, which better translates into certainty of returns.

- Tenant Profile

The type of tenant renting underlines how effectively it can pay its rent. Tenants whose businesses are resilient against economic or political uncertainly are highly desired. These include government agencies, ASX-listed entities, multinational corporations, large grocery store chains and large medical operators.

- Asset Quality and Location

This is especially important if you are investing in a single asset fund. An asset’s location and quality determine its desirability and demand from tenants, which can translate into stable income and potential for rental growth.

- Trusted Manager

The fund manager is the entity responsible for overseeing the operation and financial management of the properties. Ideally you want a manager that is experienced, has operated throughout several property cycles and has a strong track record of delivering returns to investors.

How the different types of property are performing

Residential

There are no pure residential A-REITs on the ASX. The most common form of ownership is by direct investment. Compared to commercial properties, residential investments typically have shorter leases (usually six to 12 months), ambiguous and inconsistent quality of tenants, higher overheads and lower income returns. According to Domain Group’s June 2020 Rent Report (2), median rental yields for houses across Australia’s capital cities were 3.75% and 4.22% for units.

Retail

Isolation and social-distancing restrictions throughout March to June 2020 limited shoppers from physically buying in-store. Consequently, shops have been less likely to meet rental commitments. The COVID period has escalated the growing decline of footfall in retail precincts and according to KPMG there has been an 8.1% cumulative decline throughout three years to March 2020 (3); and a predicated further fall to 11.7% throughout 2020. Additionally, JLL research showed mall vacancies have reached a 20-year high, rising 5.1% in June 2020 from 3.8% in December 2019.

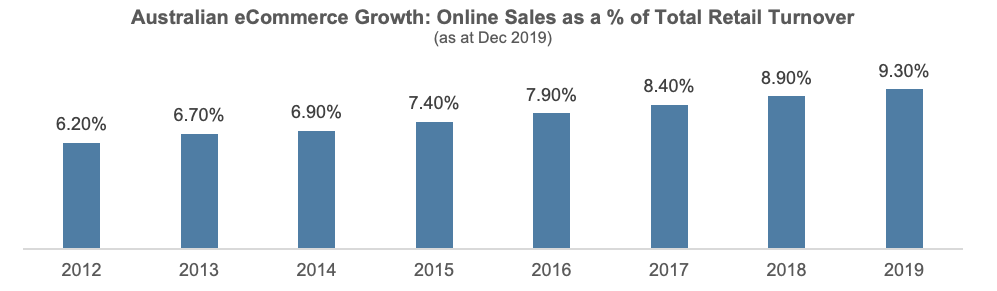

However, online shopping has steadily increased year-on-year, creating a positive impact on logistics and warehouse property. The graph below illustrates the strength of online shopping. Online retail sales grow on average $2 billion year-on-year and as at 2019 Year End, reached $30 billion (4).

Source: JLL Research, NAB

Logistics/Warehouse

These large properties usually house storage, manufacturing and logistics tenants and are typically between 5,000sqm and 20,000sqm. They are generally located along key transport corridors, such as road arterials, rail freight lines, shipping ports and airports. They are usually let on five to seven-year leases though purpose-built facilities attract longer terms. Demand for this asset class has been growing significantly in recent years due to the growth in ecommerce and its need for well-located warehouses to service customers.

According to JLL research, the average vacancy rate across Australia’s Eastern seaboard states was 3.8% at 2019 year end. Throughout 2019, retail accounted for 22% of industrial take-up, behind transport, postal and warehousing.

Office

Offices, particularly large office towers, have benefited from strong investor appetite throughout the past couple of decades. As towers attract multiple tenants, they are well diversified as the ability to generate income usually isn’t reliant on one company. Lease terms are generally between three and 10 years.

In recent weeks, workers have started to return to their offices in most cities. There has been recent negative press coverage regarding future demand, however, we believe offices have a mid to long-term positive outlook. We don’t believe the recent working from home thematic will significantly affect demand for office space.

Healthcare

Healthcare property encompasses medical facilities – from primary care, such as GPs and medical centres; secondary health, such as day hospitals; tertiary health including private hospitals; allied health such as dentists and physiotherapists; and ancillary health, such as pharmacies and childcare provisions. These assets are typically held in unlisted funds.

According to MSCI’s research for the December 2019 year-end, hospital market yields were 6.11% and medical centres, 5.97%. Healthcare assets can attract 10 to 30-year lease lengths, depending on the nature of the asset.

Due to an ageing population’s reliance on medical facilities, as well as rising chronic diseases, such as diabetes, this asset class’ demand looks very likely to continue growing.

Putting property types in perspective

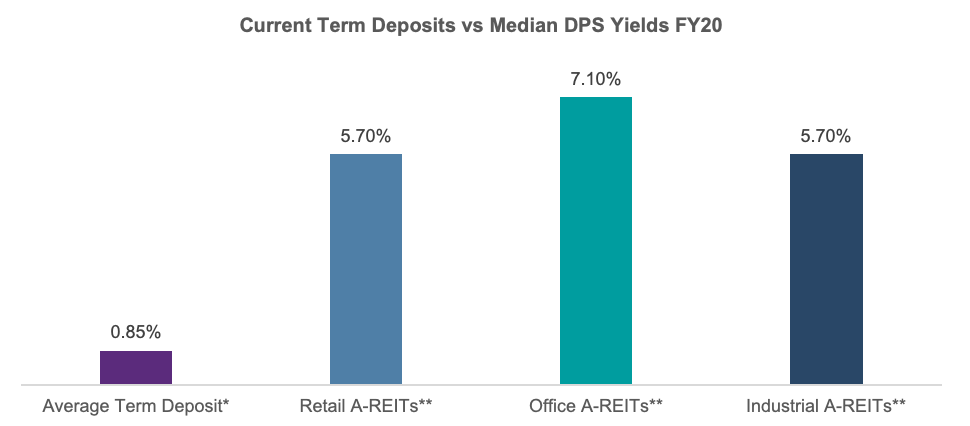

Comparing listed income returns (see below) across similar periods, shows an argument for investing in real estate property funds however risks differ between asset classes and sectors including the risk of capital loss.

Source: *Average across Australia’s four major banks as at 20 July 2020. ** Moelis Research based on Factset, Bloomberg, company disclosures as at 17 July 2020

Conclusion

In summary, while different real estate assets attract varying levels of income, in the current to long-term period, offices, warehouses and healthcare facilities continue to show strong demand. More specifically, they offer a significant premium to term deposits, albeit with higher risks of capital loss. Whether an investor wishes to invest in unlisted fixed term funds, unlisted open-ended funds or a REIT, depends on his or her risk appetite and desire for liquidity.

Open the door to generating income from property

Centuria Capital specialises in property investment management. We have a 35-year track record of delivering value to our investors through listed and unlisted property funds. Learn more about our listed funds here, or about our unlisted funds here.

Footnotes

- NAB Term Deposit interest rate for investments of $5,000 - $499,999 held for 12months is 0.95%; CBA Term Deposits interest rate for investments of from $50,000 to $1,999,999 held for 12 months is 0.85%; Westpac Term Deposit interest rate for investments of between $5,000 and $2,000,000 held for 12 months is 0.85%; ANZ Advanced Notice Term Deposit interest rate for investments of $5,000 to $99,999 held for 12 months is 0.75%

- https://www.domain.com.au/research/rental-report/june-2020/

- KPMG Beyond COVID-19 June 2020

- JLL Research Report: Australian Industrial Investment Review & Outlook 2020

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Jason Huljich’s 24-year real estate career spans the Australian commercial and industrial real estate sectors. He co-founded Centuria Capital, with Joint CEO, John McBain. Jason collectively oversees $16.8 billion of AUM (as at 23 June 2021) and c.300 staff throughout Australasia.

He is chiefly responsible for the company’s real estate portfolio and funds management operations including the ASX-200 listed Centuria Industrial REIT (CIP), ASX-300 listed Centurial Office REIT (COF), as well as Centuria's unlisted real estate funds.

1 topic

3 stocks mentioned

Jason Huljich’s 24-year real estate career spans the Australian commercial and industrial real estate sectors. He co-founded Centuria Capital, with Joint CEO, John McBain. Jason collectively oversees $16.8 billion of AUM (as at 23 June 2021) and...

Expertise

Jason Huljich’s 24-year real estate career spans the Australian commercial and industrial real estate sectors. He co-founded Centuria Capital, with Joint CEO, John McBain. Jason collectively oversees $16.8 billion of AUM (as at 23 June 2021) and...

Expertise

Comments

Comments

Sign In or Join Free to comment