Real assets to underpin infrastructure-led recovery

•

Sponsored

Print Wire

Ahead of the upcoming Pinnacle 2020 Virtual Summit, we asked three Real Asset and Infrastructure managers to share a chart from their presentation and explain its importance.

For Resolution Capital’s Jan de Vos, the current dislocation between public and private markets presents opportunities for investors as subdued share prices reflect uncertainty around short-term earnings visibility, rather than any fundamental impairment. Riparian Capital Partners Nick Waters discusses how the uncorrelated nature of agriculture, food and water makes these asset classes crucial to diversification. Finally, Palisade Investment Partner’s Roger Lloyd offers an insight into the robust pipeline of new investment opportunities that will potentially underpin the ‘infrastructure-led recovery’.

The current environment of low growth and low interest rates supports listed real assets and our experts will examine not only the fundamental merits of the sector but also the pitfalls to avoid.

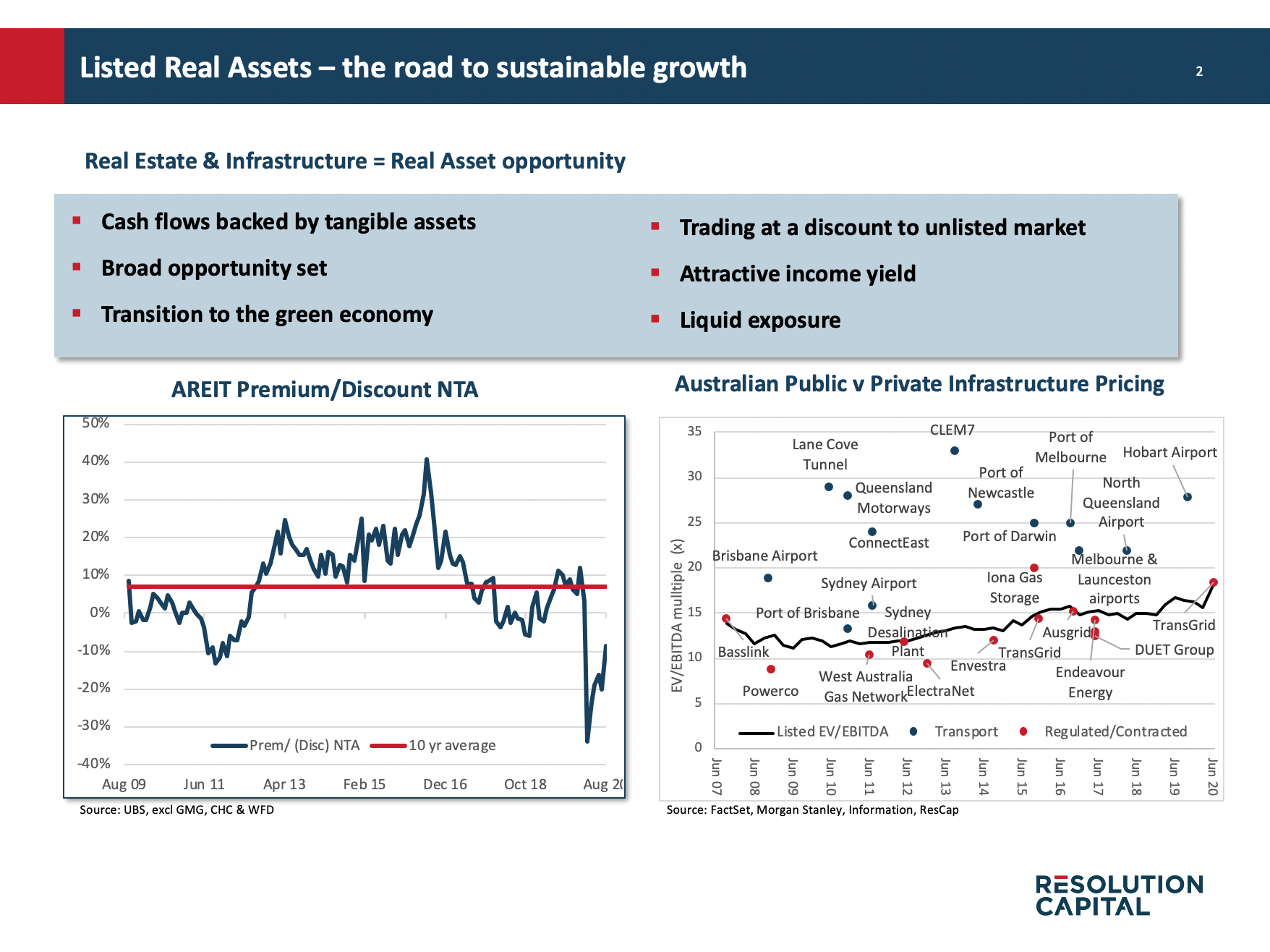

Dislocation between public and private markets

Jan de Vos, Real Assets Portfolio Manager, Resolution Capital

General equities markets have been driven higher by the tech darlings, whilst 80% of global bond yields are now less than 1%. Typically listed Real Assets are under-represented in investment portfolios even though the combination of listed real estate and infrastructure can provide diversification benefits and an attractive income yield backed by cashflows from tangible assets.

Click on the image to enlarge

The slide above shows the current pricing dislocation between the public and private markets, both in the real estate and infrastructure sectors.

We believe the current dislocation between public and private markets presents opportunities for investors as the current listed share prices reflect some uncertainty around short-term earnings visibility, rather than any fundamental impairment of the underlying assets.

The importance of liquidity was also highlighted during the COVID-19 period, with many investors needing to change asset allocations.

Listed real assets can deliver long term cashflows with growth embedded in the revenue stream. Essential infrastructure such as data centres, mobile phone towers and logistics are good examples of sectors benefiting from strong secular growth trends with the huge increase in data usage and e-commerce with COVID-19 accelerating this trend.

We believe real assets are a sector that is expected to grow with many governments around the world looking to privatise real assets to assist with funding needs.

During the summit, we will be highlighting how the current environment of low growth and low interest rates is supportive for listed real assets as well as the fundamental merits of the sector. Just as importantly we will highlight the pitfalls to avoid, as well as some of the unique exposures the sector can provide for investors.

Investing in water as a genuine source of alternative beta

Nick Waters, Managing Partner, Riparian Capital Partners

Ahead of the Pinnacle 2020 Virtual Summit, we wanted to share what we believe is one of the most advantageous attributes of investing in agriculture, food and water – the uncorrelated nature of these asset classes compared to broader financial markets.

The correlation analysis below will be part of our summit presentation focussing on Australian Water Entitlements. You can see (in dark green) the negative correlation water entitlement investments have had to the ASX200, the S&P 500, MSCI World Price Index, Australian and US 10-year bonds and the AUS/USD Spot over the past 10 years.

These negative correlations are evidence that water entitlements are one of few accessible and liquid asset classes providing a genuine source of alternative beta.

Click on the image to enlarge

During the Summit, we’ll dive further into the dynamics of these correlations, whether now is the right time to consider investing in water and if those uncorrelated positive returns can continue. We believe the lack of correlation will be sustained over the long term. Key drivers of water market returns are inherently different to the primary drivers of other traditional asset classes. Structural tailwinds supporting water entitlement values over the next decade are agricultural commodity prices, irrigation productivity gains, demand arising from new crop plantings and existing orchards maturing, as well as ongoing available supply of water, which is reducing due to climate change.

Finally, we think it’s important to point out the role water entitlements play in the sustainability of agriculture in Australia. Australia has developed one of the most functional and sophisticated water entitlement markets in the world - this market efficiently allocates a scarce resource, supports the development and expansion of the agriculture industry plus provides capital to improve the financial efficiency of farming operations.

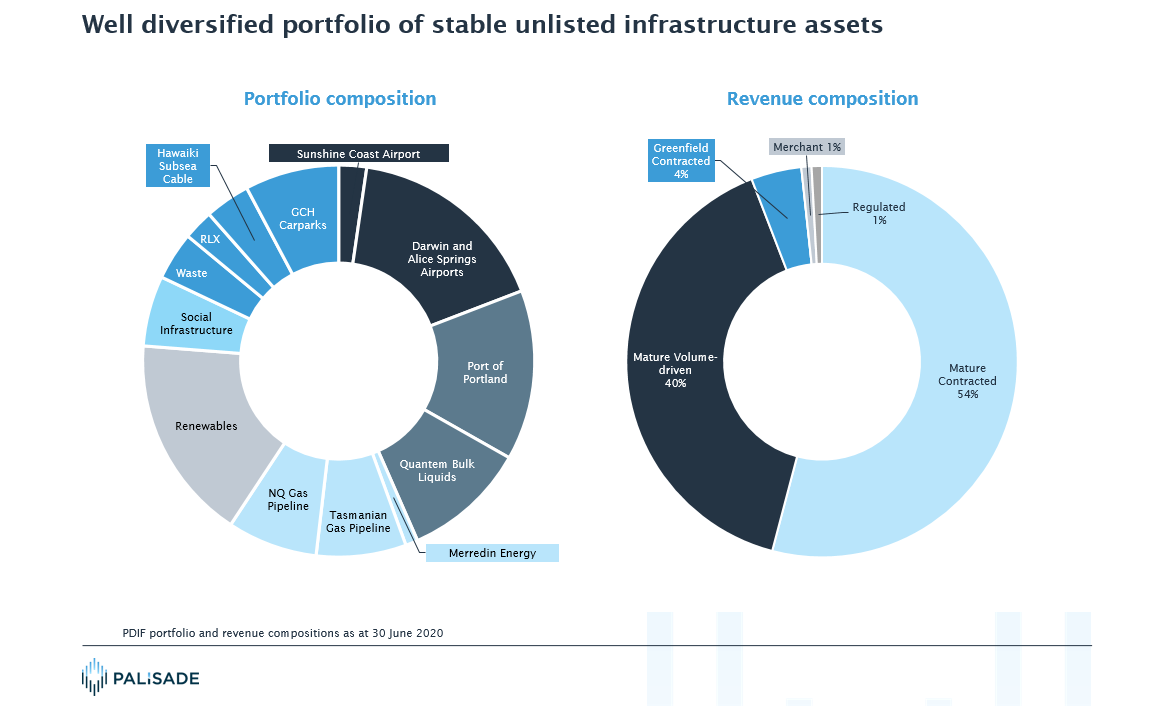

Discovering the assets likely to benefit from an ‘infrastructure-led’ recovery

Roger Lloyd, Palisade Investment Partners, Managing Director and CEO

Unlisted infrastructure has traditionally been a difficult asset class for non-institutional investors to access. Ahead of the Pinnacle 2020 Virtual Summit, we wanted to share an image which outlines the unique portfolio we have developed for our flagship infrastructure fund (PDIF) since Palisade’s establishment over 12 years ago, and the assets and sectors our new wholesale feeder vehicle, as an investor in PDIF, will gain access to.

Click on the image to enlarge

Palisade’s investment philosophy is to invest in defensive, stable unlisted infrastructure assets in Australia and New Zealand, with a deliberate focus on the “mid-market”. In our view mid-market infrastructure in Australia is characterised by a greater supply of transactions and less competing capital. This allows for superior risk-adjusted returns relative to large-cap unlisted infrastructure, and with a lower level of volatility than listed counterparts. Furthermore, by targeting smaller assets within the infrastructure landscape, Palisade is able to invest in controlling positions on behalf of our clients, maximising our ability to actively manage these assets.

Our mid-market focus also allows us to invest capital within defined sector verticals, including airports, ports and bulk liquids storage, pipelines, renewable energy, social infrastructure and waste treatment. This diversification provides investors with significant downside protection, particularly during periods of heightened volatility.

During the summit I’ll provide an insight into the robust pipeline of new investment opportunities we are currently seeing, particularly as governments and corporates seek support from private capital to invest in infrastructure in the current COVID-19 environment as a means of providing balance sheet relief and driving the “infrastructure-led” recovery.

Register for the Pinnacle 2020 Virtual Summit

Hear from some of Australia’s most experienced investors in Real Assets and Infrastructure as they discuss the key trends shaping the sector and how investors can gain exposure. A Q&A session will follow, hosted by Louis Christopher, Managing Director of SQM Research.

You can register for the session here, or view the entire event calendar here

Important Information: Please be advised that the Pinnacle 2020 Virtual Summit is designed for sophisticated investors only

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

3 topics

3 contributors mentioned

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets