TOL - 17th Nov, 2022

Shares may have bottomed

At last, it seems some of the bad news for shares appears to be abating. It’s certainly been a rough year. Thanks to a combination of high inflation, hawkish central banks, a surging US dollar, a war in Ukraine, along with other geopolitical tensions and rising recession risks, bonds and shares have had poor returns.

It’s been the rise in inflation that has been the key driver. From their highs late last year or early this year, to their lows in October, US and global shares fell around 25%. Australian shares held up better thanks to strong resource earnings and a less hawkish RBA, but still fell 16% to their low in June and held just above this in October.

Bonds, which are normally a source of stability in the face of share market falls, have had their biggest losses in decades as rising inflation pushed yields up. Tech stocks and cryptocurrencies, being amongst the biggest winners of easy money and the pandemic lockdowns, have been amongst the biggest losers from monetary tightening and reopening, with crypto land still in turmoil.

Never miss an update

Get the latest insights from me in your inbox when they’re published.

Advertisement

But, from their recent lows, global and Australian shares are up 10% or so.

In fact, Australian shares are now only down about 4% year to date. Shares

may have run a bit ahead of things in the near term as they often do, but

the big question remains, is this rebound sustainable?

Some better news

Bear markets are known for their periodic spikes higher as investors’ short positions are squeezed, often after a bit of less bad news. In the tech wreck and GFC, bear market rallies were up to 20% or so. And of course, we have seen two bear market rallies into March and August that proved short-lived. But this time there’s been fundamental improvement:

First, it’s been a long time coming, but underlying US inflation finally

appears to be easing. Headline inflation in October dropped to

7.7% year-on-year (YoY) (well down from a peak of 9.1% in June) but more importantly

core (ex-food and energy) inflation came in at a slower-than-expected

0.3% month-on-month, easing to 6.3% YoY from 6.6% YoY. Prices for used cars,

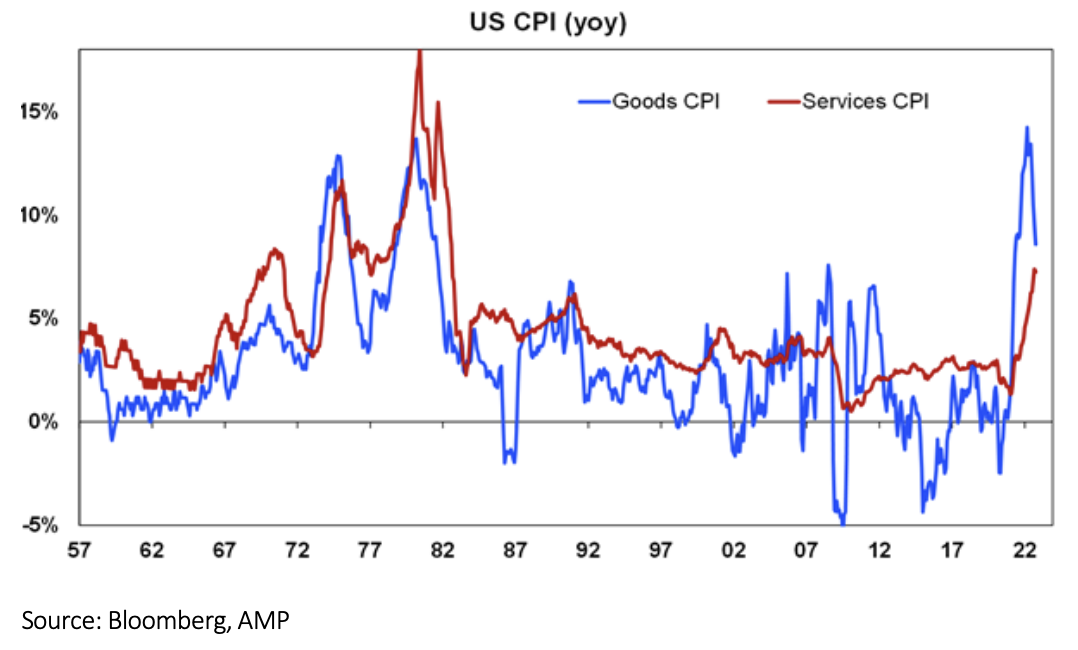

household furnishings, medical care and airfares fell. US goods price

inflation has rolled over and this tends to lead services price inflation.

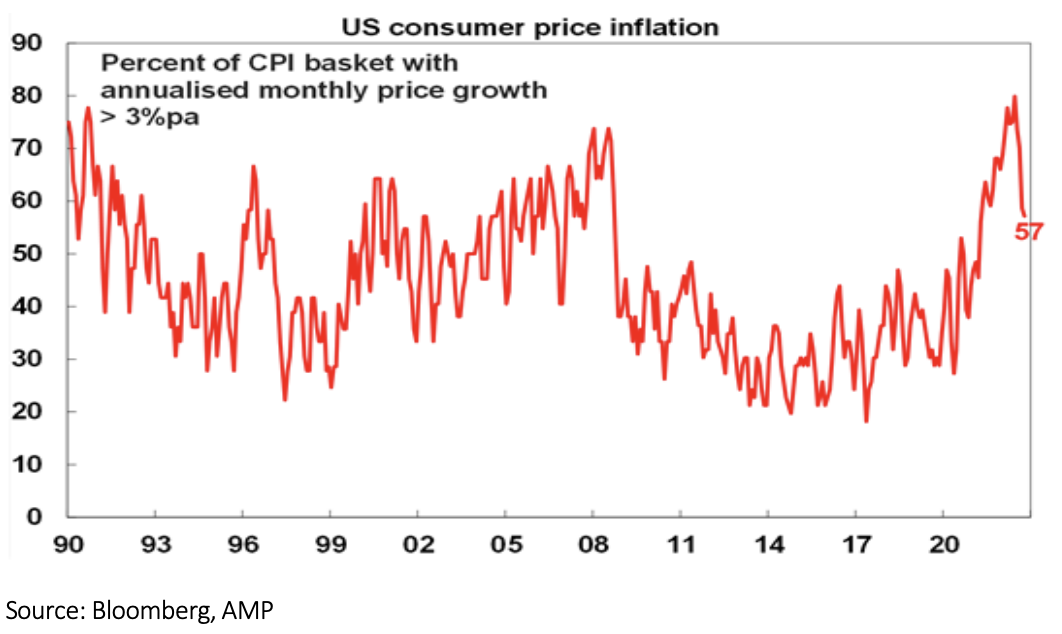

What’s more, the proportion of CPI components with annualised

monthly inflation above 3% YoY is falling sharply.

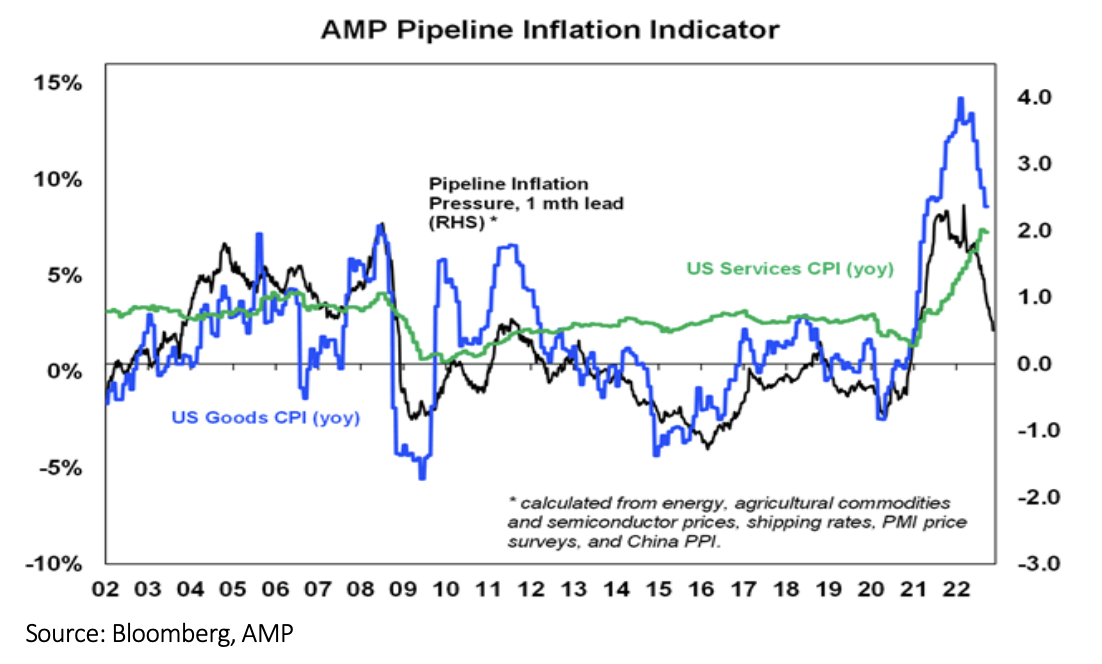

This is all consistent with falls in our Pipeline Inflation Indicator due to

easing supply constraints, freight rates, commodity prices and cost

pressures in business surveys. This Indicator correlates more with

goods inflation (which is slowing), but this guides services inflation, so it's

likely to slow too. A year ago global growth, US wages, rents,

commodity prices, US public spending, anecdotes, car prices, money

supply growth, freight rates and business surveys were all pointing up

for US inflation. Now they are all slowing, or pointing down.

Inflation in Australia is lagging behind the US by around six months, so it should

start to decline here from early next year as well. And Australian shares

take their directional lead from the US most of the time anyway. Why?

Central banks are slowing or moving to slow their rate hikes

This started with the RBA dropping to 0.25% hikes, the Bank of Canada dropping to a 0.5% hike, the ECB sounding less hawkish, the Fed opening the door to slowing down (with lower inflation data adding to its likelihood) and the Bank of England pushing back against market expectations for how high it will raise rates. The common denominator is that rates are now around neutral or restrictive and there is a need to allow for the lags with which monetary policy impacts economic activity. Of course, central banks are still hawkish as inflation is too high and jobs markets are still too tight, so more rate hikes are likely. But a slowing in the pace reduces the risk of hard landings.

The US dollar and bond yields are showing signs of rolling over

This is significant as the rise in both have been key elements of this bear market. A rollover in the $US will reduce the risk of a financial accident in emerging countries and will stop exporting US inflation globally, and lower bond yields will ease the valuation pressure on shares.

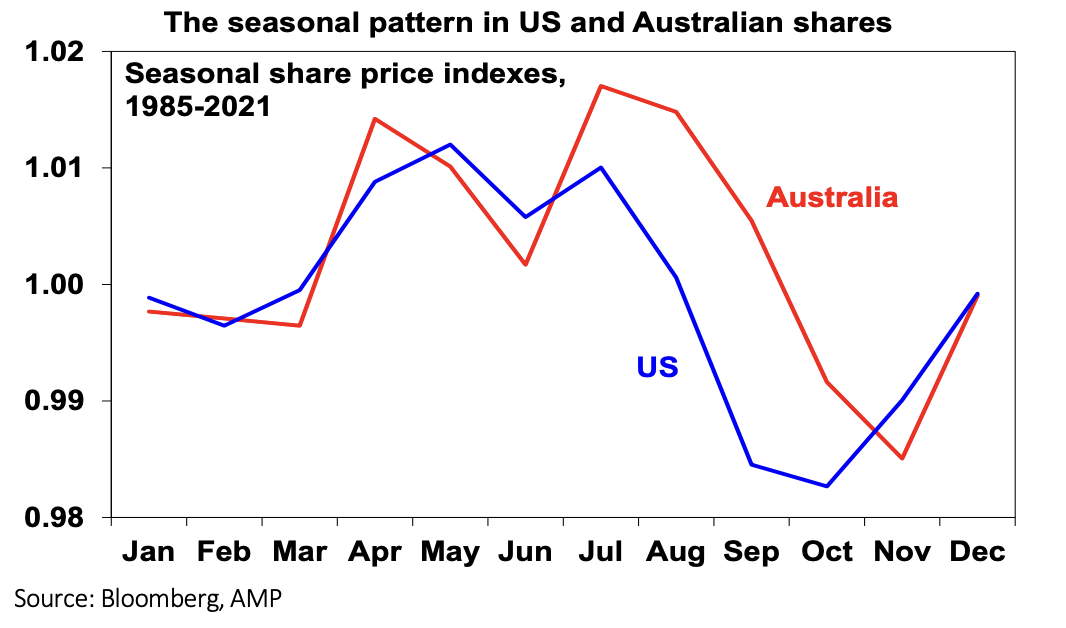

This is now traditionally a Santa Rally period

We have now entered a positive part of the year for shares from a

seasonal perspective, with US, global and Australian shares tending to

rally from October/November into year-end and out to the middle of

the next year, reflecting an end to tax loss selling in the US, new year

cheer and a lack of capital raising over the Christmas/New Year period.

With the Party Congress over, China is focussing on boosting its economy

China has announced 20 measures to “optimise” its COVID policy – with some easing in controls and measures to step up medical preparations including vaccinations and treatments. It looks likely to exit from zero-COVID around March next year. And it has announced 16 measures to support its ailing property sector. The latest upswing in COVID cases will cause short-term disruption, but an exit from zero-COVID and increased property construction work means Chinese growth will likely surprise on the upside next year, which could boost global growth. This is not to say that China’s longer-term growth potential is not trending down (with slowing workforce growth, greater Government intervention reducing dynamism, trade tensions with the West and its property issues), but it will still see cyclical swings.

In addition, longer-term inflation expectations remain reasonably “well anchored” suggesting that it should be easier for central banks to get inflation back down than it was in the 1980s when deep recessions were needed to break entrenched inflation psychology.

There is a rising chance we have seen the low in shares and we remain

optimistic on shares on a 12-month horizon, as investors will start to focus

on monetary easing from late next year and then economic recovery.

What are the risks?

There are four main risks:

1. Inflation could surge anew or remain sticky at high levels necessitating more aggressive rate hikes. This is possible and we remain of the view that inflation will be higher over the medium term as the world is now more inflation prone. However, slowing growth is known to slow inflation so there is still likely to be a cyclical downswing in inflation.

2. Recession – this is likely in Europe, with about a 50% probability in the US and about a 40% probability in Australia. Deutsche Bank has pointed out that since 1950 the third year of the US presidential cycle has not had recessions in quarters 2 to 4 and this may partly explain why shares have been strong in the third year. So, if the US has a recession next year it may break the record of positive returns after the midterms. A counter is that the share slump this year has been consistent with mid-term election year slumps and it may have discounted a mild recession, which would not preclude shares from having their typical post-mid-term rally even if there is a recession next year, providing its mild.

3. Geopolitics could worsen. Russia could escalate further in Ukraine. Problems in the Middle East could also escalate given the failure to return to the 2015 nuclear agreement with Iran, social unrest in Iran and the return of Netanyahu as Israeli PM increasing the risk Israel will take action against Iran’s nuclear capability. China could move on integrating Taiwan. And tensions could be fanned if President Biden adopts a more hawkish foreign policy stance. But getting geopolitical problems right is never easy and some of these could go the other way.

4. Republican control of the US House will likely lead to brinkmanship in

funding the US Government and increasing its debt ceiling.

What about the latest problems in crypto land? Bitcoin has fallen to a new

cycle low on liquidity issues at the FTX crypto exchange (now bankrupt).

Cryptos were a beneficiary of easy money and have been suffering from its

withdrawal. Financial accidents are common outcomes of Fed tightening and the crypto problems could go further. This may be bad for crypto traders

but it's unlikely to have a major impact on global growth and share markets

as investor and financial system exposure to it is relatively low. It's good

news for gold though as the crypto craze was sucking the life out of it.

A final comment

The ride for shares may still remain choppy and new lows can’t be ruled out.

But the increasing evidence of a peak in US inflation and central banks

slowing their rate hikes along with positive seasonals and the track record of

US shares rallying after the mid-terms indicate we may have seen the low

and add to our confidence that the next 12 months will be positive for

shares. The same is also likely to apply for the $A, being a cyclical currency.

Never miss an insight

Enjoy this wire? Hit the ‘like’ button to let us know. Stay up to date with my content by hitting the ‘follow’ button below and you’ll be notified every time I post a wire.

Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies (“Livewire Contributors”). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

3 topics

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Expertise

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets