Small caps turned “Upside Down” as fundamentals fly out the window

One of the shows that helped cement Netflix’s popularity as a streaming service is Stranger Things. The science-fiction thriller centres around the rural town of Hawkins, Indiana, where the nearby Hawkins National Laboratory conducts secret experiments and inadvertently creates a portal into an alternate dimension known as the “Upside Down”. The influence of this new world transcends into the old: people disappear, things stop making sense and dangerous monsters lurk in the shadows.

In a way, the stock market is experiencing its own Stranger Things moment. Fundamentals no longer matter, stocks with negative cash flows are outperforming proven businesses and the shadowy apparatuses of governments and central banks are distorting market functioning.

Here, I cover how three small-cap managers who spoke at the annual Pinnacle Investment Summit yesterday are navigating an asset class turned “Upside Down”. The fundies, from Spheria, Longwave and Firetrail, discuss whether quality should matter, the dangers of chasing expensive stocks and areas where they’re finding value.

2 key distortions

To set the scene Marcus Burns, Portfolio Manager at Spheria points out that central banks have unleashed record liquidity into economies. In Australia, money supply has soared nearly 40% in the last 12 months; while this is buffering the financial impact of COVID-19, it has created two upside-down circumstances in investing today.

- The first is the stimulus distortion whereby the $750 weekly JobKeeper benefit has intersected with an economy where sectors such as tourism and leisure are shuttered. As a result, consumer spending has been forced into retail and caused share prices in that sector to re-rate in the short-term.

- The second is the interest rate distortion whereby low and negative rates globally have triggered a further extension of growth names over value, causing retail investors to aggressively chase momentum stocks, particularly in small and micro caps, and hyped up interest in gold as an inflation hedge.

Together, Burns says these factors have coalesced and given way to the “rise of speculative stocks” beyond conceivable multiples. Investors are taking the view that the “less you earn, the more you’re worth”.

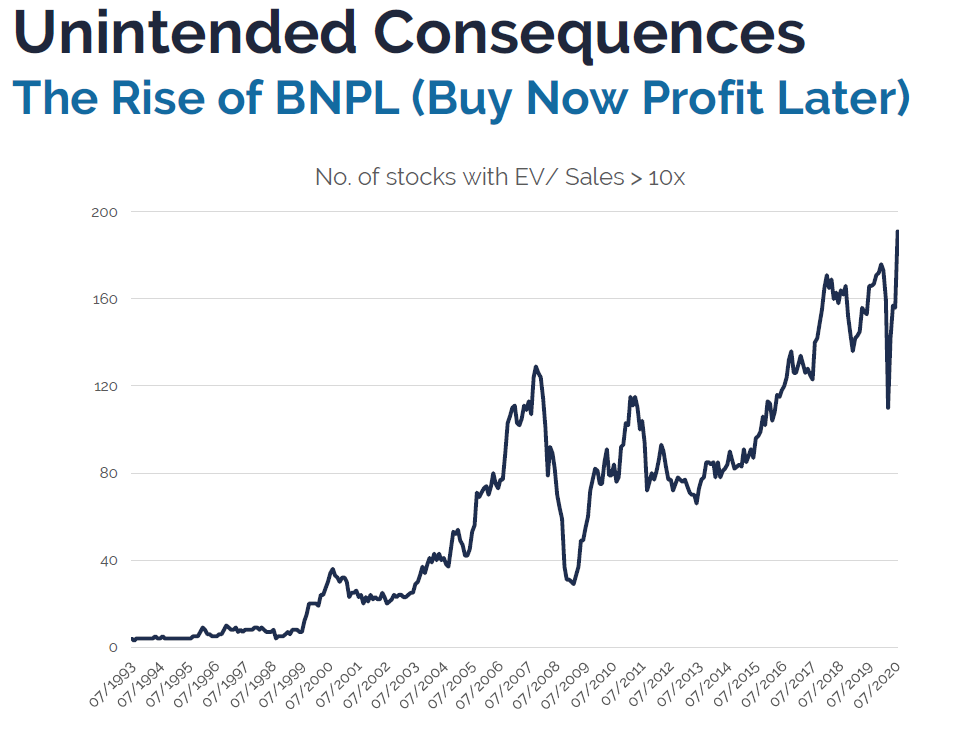

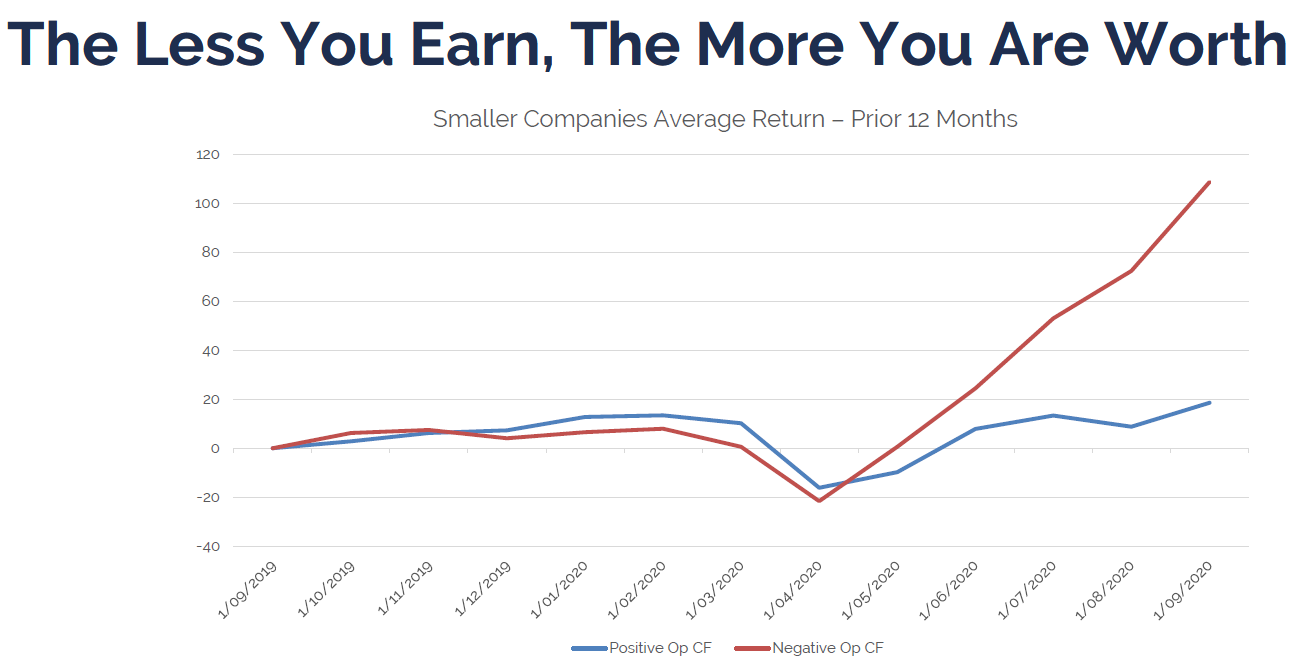

To underscore his points, Burns refers to the charts below which shows a surge in the number of companies with enterprise value (EV)/sales multiples at 10 times or greater, and the recent outperformance of stocks with negative cashflows. This bucket includes thematics investors have become all too familiar with including the “Buy Now, Profit Later wannabes”, resources stocks and technology disruptors.

Click to enlarge

Chart Source: Bloomberg data, ASX stocks with market cap > $50m and EV/trailing sales multiple over 10x

Click to enlarge

Chart Source: Bloomberg data: simple average return of stocks between ($50m and 3.0bn market cap divided into positive op cash flow and negative op cash flow over prior 12 months.

“In normal investing parlance an EV/Sales ratio of 5-6 is considered to be fully priced. An EV/Sales of 10 or above is considered rarefied and is reserved for stocks with incredibly high growth rates and margins. You don’t see that commonly. But in Australia this has soared to nearly 200 companies. To put that into context that is about 10% of the number of companies listed on the ASX.”

Unfortunately, this strategy doesn’t work

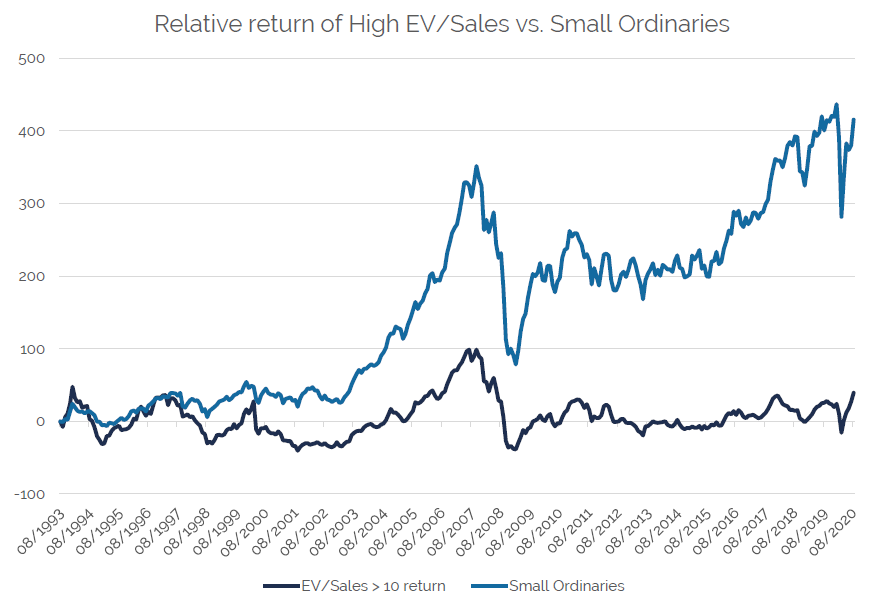

While some investors may be enjoying short-term returns on the likes of Afterpay, Zip, Sezzle and beyond, chasing expensive stocks is a strategy that’s fraught with danger. As Burns shows in the next chart, stocks that trade on ludicrous EV/Sales ratios dramatically underperform over the long-term. Since 1993, the ASX Small Ordinaries Index has delivered a gain of just over 400%, while those exhibiting high EV/Sales ratios have not even doubled.

Click to enlarge

Chart Source: Bloomberg data, ASX stocks with market cap > $50m and EV/trailing sales multiple over 10x

Benjamin Graham, the father of value investing, once said: “In the short run, the market is a voting machine but in the long run, it is a weighing machine”. Burns believes that investors will eventually revert to prizing stocks that generate positive cash flow and that this is the biggest opportunity in small caps right now.

“It does pay to focus on cash flow long-term even though short-term we’ve seen this upside-down world where hype, disruption and a whole bunch of non-fundamental things are driving the stock market.”

For these reasons, Spheria is steering away from the “hot” thematics and focusing on companies with attractive valuations, balance sheets and free cash flow generation.

Why quality matters now more than ever

Building on Burns’ points, David Wanis, CIO and Portfolio Manager at Longwave Capital, urges investors to focus on high-quality businesses in small caps.

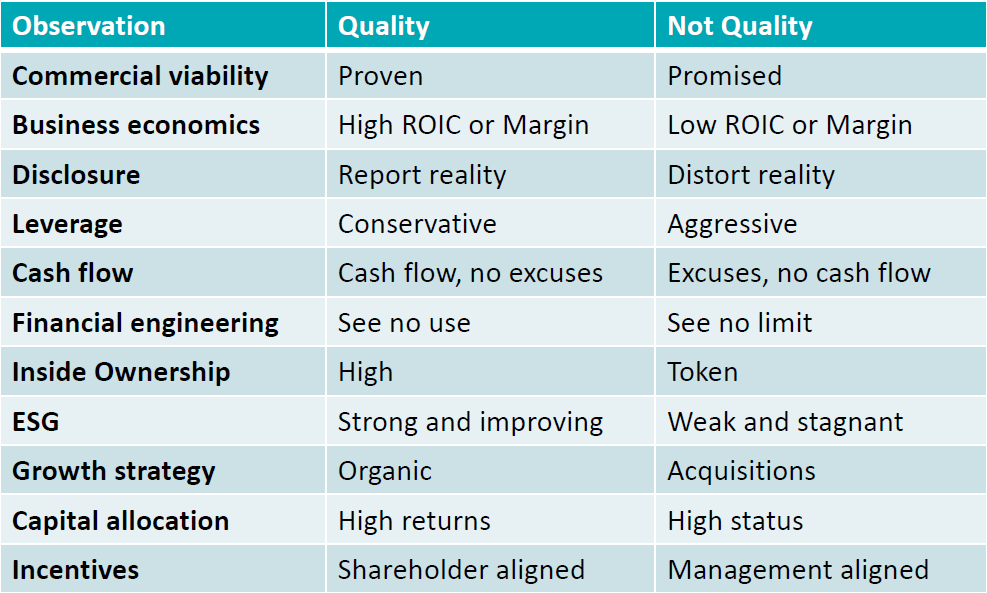

“Quality is the non-negotiable golden rule that determines success in small cap investing.”

But what exactly is quality? Wanis explains that while quality is in the eye of the beholder, the subjectivity pertaining to this metric creates inefficiencies in the universe which investors can exploit. Longwave has developed an 11-point checklist provided below to assess quality. For investors, the key is to form a view on how many, and which criteria, need to be ticked off to meet their own quality thresholds.

Wanis adds that the focus on quality shouldn’t mean that valuation is irrelevant. Rather, quality should always come first, and proof of the benefits of this approach is shown in the performance chart below.

Click to enlarge

Source: MSCI, Longwave Capital Partners.

“The risk of looking at value first is that investors get caught in the value trap; that you end up with low-quality businesses, and those low-quality businesses in small caps do have a propensity to fail more often and end up on the loser side of the portfolio," he says.

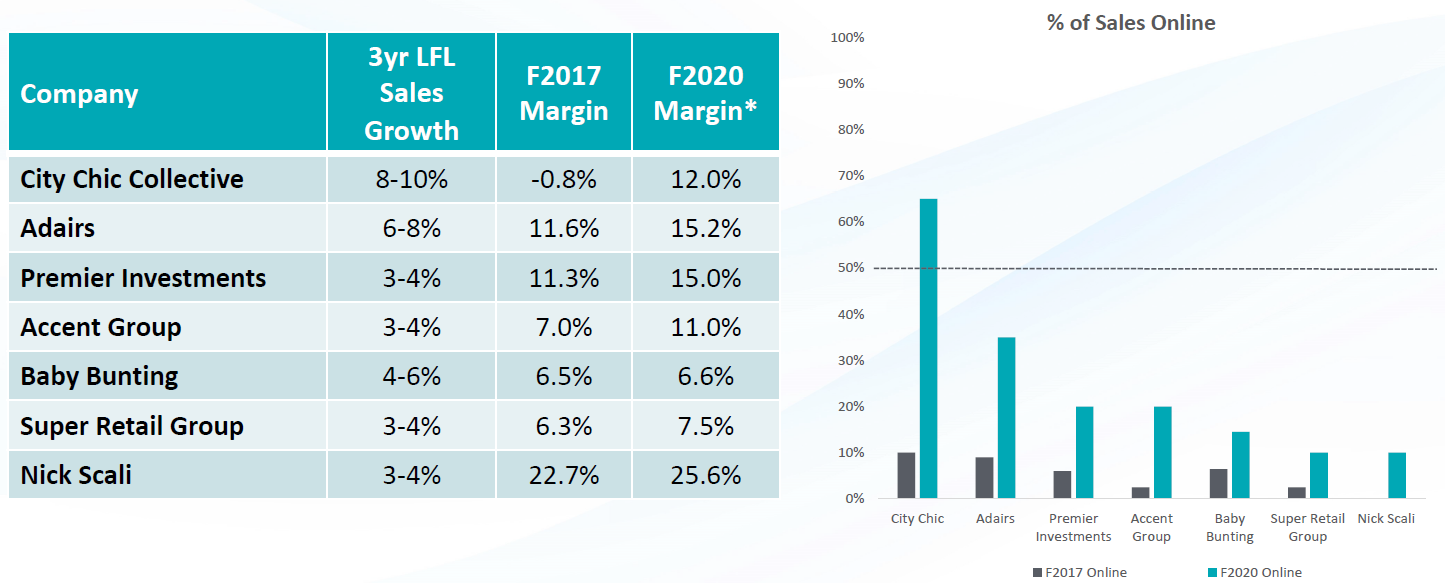

Quality stocks thematic: Select retailers shifting to online sales

While Wanis agrees that looking at the retail sector is “fraught with noise” amid lockdowns, stimulus payments and the recession we’re currently in, Longwave takes a 3-5-year view when investing in companies. On that basis, the selected retailers Longwave has picked out below offer a compelling opportunity as they shift more of their sales online.

Click to enlarge

Source: Longwave Capital Partners, Company Accounts. * estimated F2020 margin for Premier Investments

Wanis says these companies possess three attractive drivers:

- The first is that while COVID-19 has accelerated adoption of online purchasing, boosting sales via the web has been a stated goal for these businesses.

- The second is that like-for-like sales growth has been positive, which means consumers identify with their brand and products.

- The third is that Longwave expects their operating margins to improve as the percentage of sales online moves closer to 50%. In particular, online sales are far more productive that what an employee could generate in-store while warehouse rent is one-tenth of that of a shopping centre.

“There is a huge economic incentive to move sales online, so we think these are going to be even better businesses in the future," he says.

2 big opportunities in under-researched small caps

In the context of requiring careful stock selection in the current environment whilst exploiting inefficiencies in the small cap asset class, Matthew Fist, Portfolio Manager of the Firetrail Australian Small Companies Fund offered two punchy stock ideas.

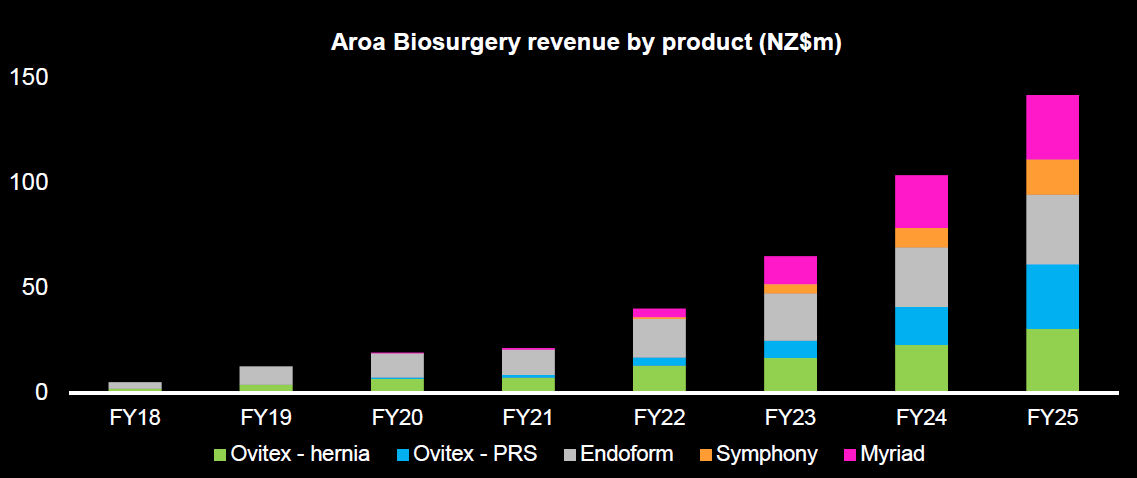

Aroa Biosurgery (ASX:ARX)

The newly listed ASX biotech of New Zealand origin focuses on improving the rate and quality of healing in complex wounds and soft tissue regeneration. Fist explains that the company’s products are derived from the fourth stomach of sheep and can be used to patch up a person’s skin or organs.

Firetrail is one of Aroa’s largest institutional investors. Fist says the Firetrail team’s conversations with surgeons and a review of scientific evidence has confirmed the superior technology of Aroa’s products.

“This results in two things: 1) Lower occurrence rates, and 2) Lower complications compared to the alternatives. This is extremely important because patients, surgeons and medical insurance companies aren’t that keen on doing these procedures twice for obvious reasons.”

Despite the benefits, Aroa’s products are cheaper when compared to peers yet gross margins are above 75%. Firetrail expects the company’s revenues to grow strongly (see below forecasts) on the back of new and existing products. Fist says while the stock may be expensive, the fundie has a high level of conviction in the science.

Click to enlarge

Source: Firetrail Forecasts

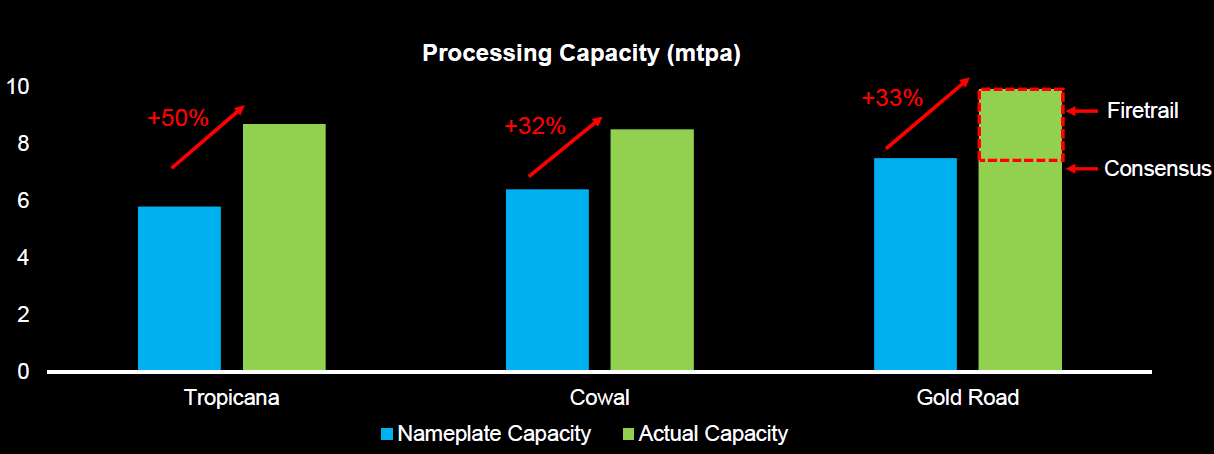

Gold Road Resources (ASX:GOR)

While the gold sector is running hot and valuations across the board are stretched, Fist reckons Gold Road Resources has significant re-rating potential.

He frames the opportunity by contextualising the forecast processing capacity for Gold Road’s mine versus peers IGO (formerly Independence Group) and Evolution Mining. In a simple sense, each mine is given a “nameplate” or nominal processing capacity during the feasibility and construction process. However, tweaks and upgrades over time result in an increase to that capacity, as the Tropicana and Cowal mines show.

Below, Fist shows that the market is assuming GOR will only meet its nameplate processing capacity and ignoring any upside.

Source: Company Data, Consensus Expectations, Firetrail Forecasts

“Based on our bottom-up work and benchmarking of similar plant designs, we expect Gold Road’s processing capacity to increase to 10 million tonnes over the next two years or some 30%.”

This would result in a material 45% uplift to GOR’s cash flow and a far higher discounted cash flow valuation, Fist says.

“Gold Road is a long-life, low-cost and materially undervalued company, and it is misunderstood by the market,” he concludes.

Pinnacle's 2020 Virtual Summit continues tomorrow

Throughout the week, Pinnacle will bring together some of the brightest minds in Australian investment management to help you build more robust, resilient portfolios.

In case you missed it, my colleague Glenn Freeman wrote a wire on '3 infrastructure strategies tipped to catch the COVID snap-back' covering views on real assets and infrastructure from Resolution Capital, Riparian and Palisade. Wednesday's sessions will focus on:

- The greatest risks and opportunities in global equities right now,

- The merits for investors of listed closed and open-ended vehicles, LIC discounts and ETF performance during a crisis.

Click here to register for both events and to view the full schedule.

Like this wire? Let us know by hitting the 'like' button to the left. Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire.

Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

3 topics

12 stocks mentioned

2 contributors mentioned

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management