The ASX 200 is getting smashed, but is now the big opportunity you’ve been waiting for?

To buy or not to buy. That is the question. Fundamentals, technicals, and how historical moves played out. We’ve got you covered.

To buy or not to buy? That is the question 🤔.

Investors who have been patiently waiting for a pull back in the Australian stock market finally have their opportunity to buy. Don’t they?

Well, we have corrected – of that there can be no question! Since the 14 February peak of 8616, the S&P/ASX 200 has lost 680 points or about 7.9% of its value based on yesterday’s closing price of 7934. It was as bad as 883 points and 10.2% down at the lowest point of this correction, 7733, set on 12 March.

“Correction” – what does that term even mean? If Aussie stocks have just had a “correction”, does this mean they were “incorrect” before? As in, they shouldn’t have been as high as they were in the first place?

Maybe, and we’ll expand on that topic soon, but for now, let’s clarify that a correction relating to the stock market is defined as a 10% or greater decline from a market peak. It’s not to be confused with a bear market, which is defined as a 20% or greater decline from a market peak.

Let’s investigate whether investors are right to jump in now and take advantage of the current correction in terms of fundamental valuations, as well as where the Australian stock market sits in terms of whether this correction could transform into a rampaging bear market.

Buy, or wait for a better entry point? Let’s dive in!

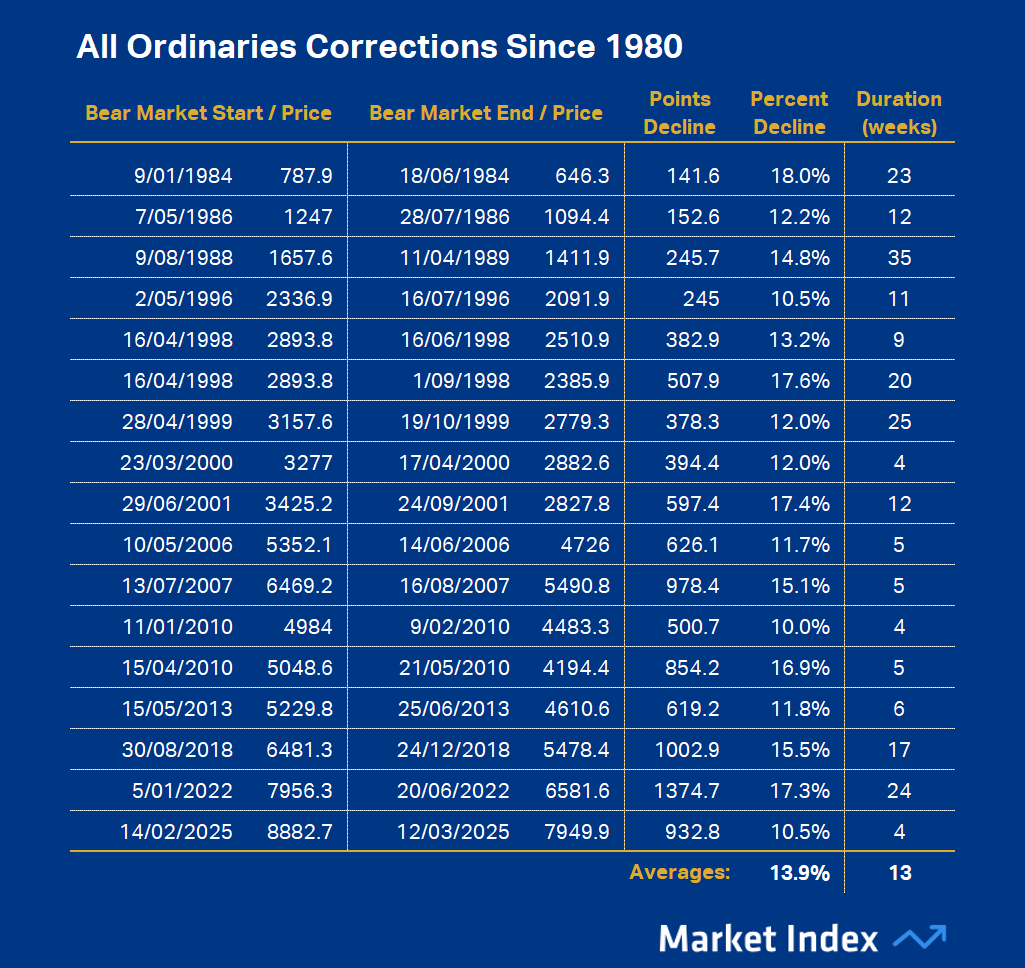

ASX corrections and bear markets since 1980

Let’s do some research into corrections versus bear markets on the Australian stock market. I want to go way back, to 1980, so I’m going to use the All Ordinaries instead of the current benchmark ASX 200 as that index only began in 2000. (The All Ordinaries preceded the ASX 200 as the main benchmark, and therefore we have more data for it.)

There have been 17 corrections (including this one) and 12 bear markets since 1980 – so that’s one major market downturn approximately every 18 months on average. The last one occurred in 2023 – so the timing of the current downturn is about spot on.

{kind=link}

As far as corrections go, 10% can be just the start of it, though. The average All Ordinaries correction since 1980 lasted approximately 13 weeks and sliced around 14% off the Aussie stock prices. Corrections greater than 15% were not uncommon, however, and whilst 7 of the 17 lasted less than a couple of months, there were nearly as many corrections that lasted for the better part of 6 months. It’s worth noting that the current correction deserves an asterisk because of its ongoing nature…ba-ba-baaammm 🚨!

{kind=link}

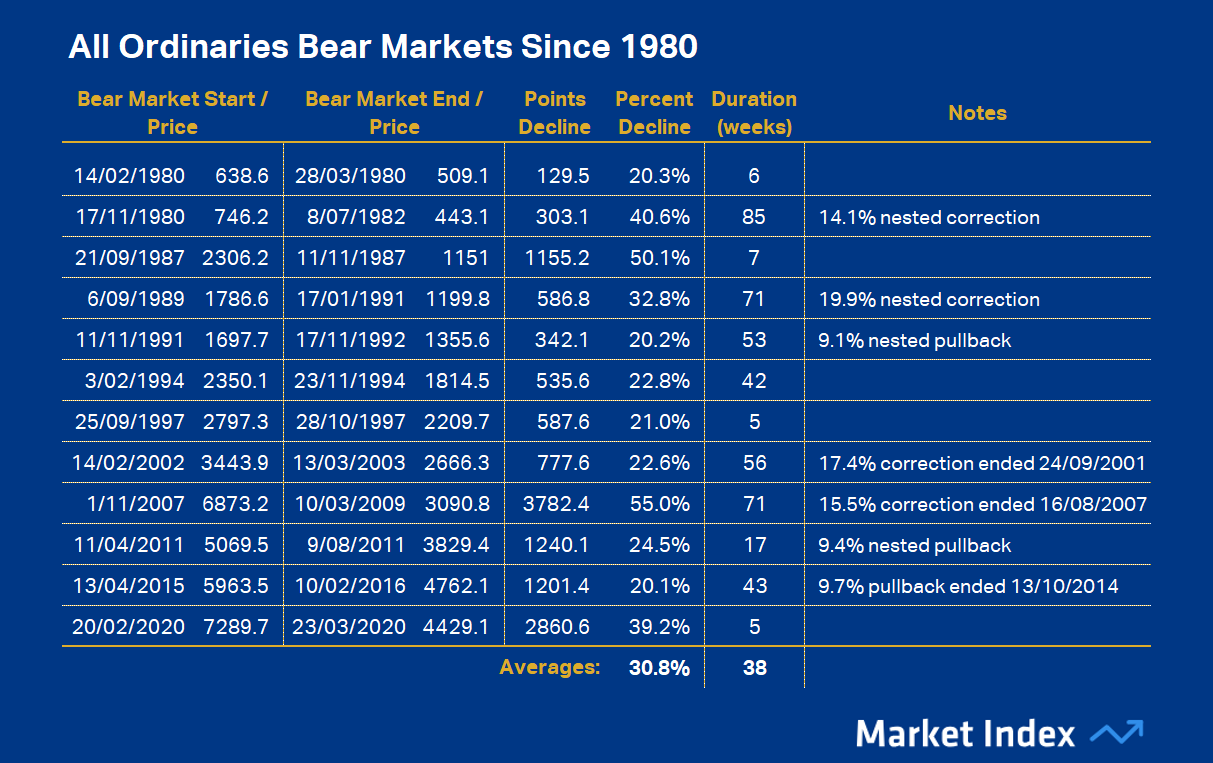

Ok, bear markets now, and this is where things get really ugly! 12 in 45 years, that’s one every 3 years and 9 months. That feels way more common than it should – but that’s the thing about bear markets (and corrections) – they can occur at any time!

It was usually a combination of different stock price crushing factors that caused the last 12 bear markets – from recession, to political upheaval, to credit crunches, and to pandemics. This time it might even be a global trade war…(Cue the ba-ba-baaammm again 🚨!)

Yes, you never quite know when a bear market is about to pop up. Like 1987’s “Black Monday” induced 50% in 7 weeks – at least that was short and sharp – or 2007’s “Big Short” in which Aussie stocks lost a devastating 55% over 71 weeks during the worst global economic slowdown since the Great Depression.

The average bear market, however, saw 30.8% wiped off the All Ordinaries with an average duration of 38 weeks (approx. 9 months). But, within the averages, there are some interesting bear market notes to observe that may help provide context for the current market gyrations.

Corrections and near-correction pullbacks preceding bear markets are common. The 2002 and 2007 bear markets occurred within 6 months of corrections, and the 2015 bear market occurred within 6 months of a 9.7% pullback.

Then there are what I call “nested” corrections and nested near-correction pullbacks that occur during the early stages of a bear market. This means that the market corrected, rallied back up by at least as much from the correction low, and then plunged into a broader bear market. These whipsaw actions occurred before or at the start of more than half of the bear markets in the sample.

This suggests that corrections are not to be trifled with. They are often a harbinger of something more sinister potentially bubbling up under the surface of the macroeconomic backdrop. It also potentially suggests that many investors discounted the prevailing issues at first, because perhaps they were too focused on all the money they were making in the prior bull market – but then those issues suddenly became too dangerous to ignore (Cue the ba-ba-baaammm again 🚨!).

If this correction turns out to be the start of the next bear market, then there’s still a long way to go (10%-ish so far vs 30%-ish on average, and 7 weeks so far vs 38 weeks on average). So, as far as the question of “Is it time to buy the current dip?” is concerned, there may be no harm in waiting for more clarity on how President Trump’s trade war is going to impact the global economy – and therefore by extension – local stock prices.

Are ASX stocks cheap yet?

Perhaps the most commonly used yardstick of stock market valuation is the market P/E Ratio. “PE” stands for price to earnings. It’s a simple formula that divides the earnings expected from an asset over the next 12 months into its current price: P/E.

In short, the P/E implies that a higher E vs P results in a lower P/E Ratio. This is a good thing, because it means it costs less to buy one dollar’s worth of the asset’s earnings. Less to buy anything implies cheaper. Conversely, a lower E vs P results in a higher P/E Ratio, and we typically say this means the asset is more expensive.

So, are Aussie stocks cheap or expensive? That all depends on what you call cheap or expensive. The old rule of thumb as far as P/E Ratios go is:

- >20 = Expensive (many major market tops occurred when the market P/E Ratio rose above 20)

- ~15 = Fair value

- <10 = Cheap (many major market lows occurred when the market P/E Ratio fell below 10)

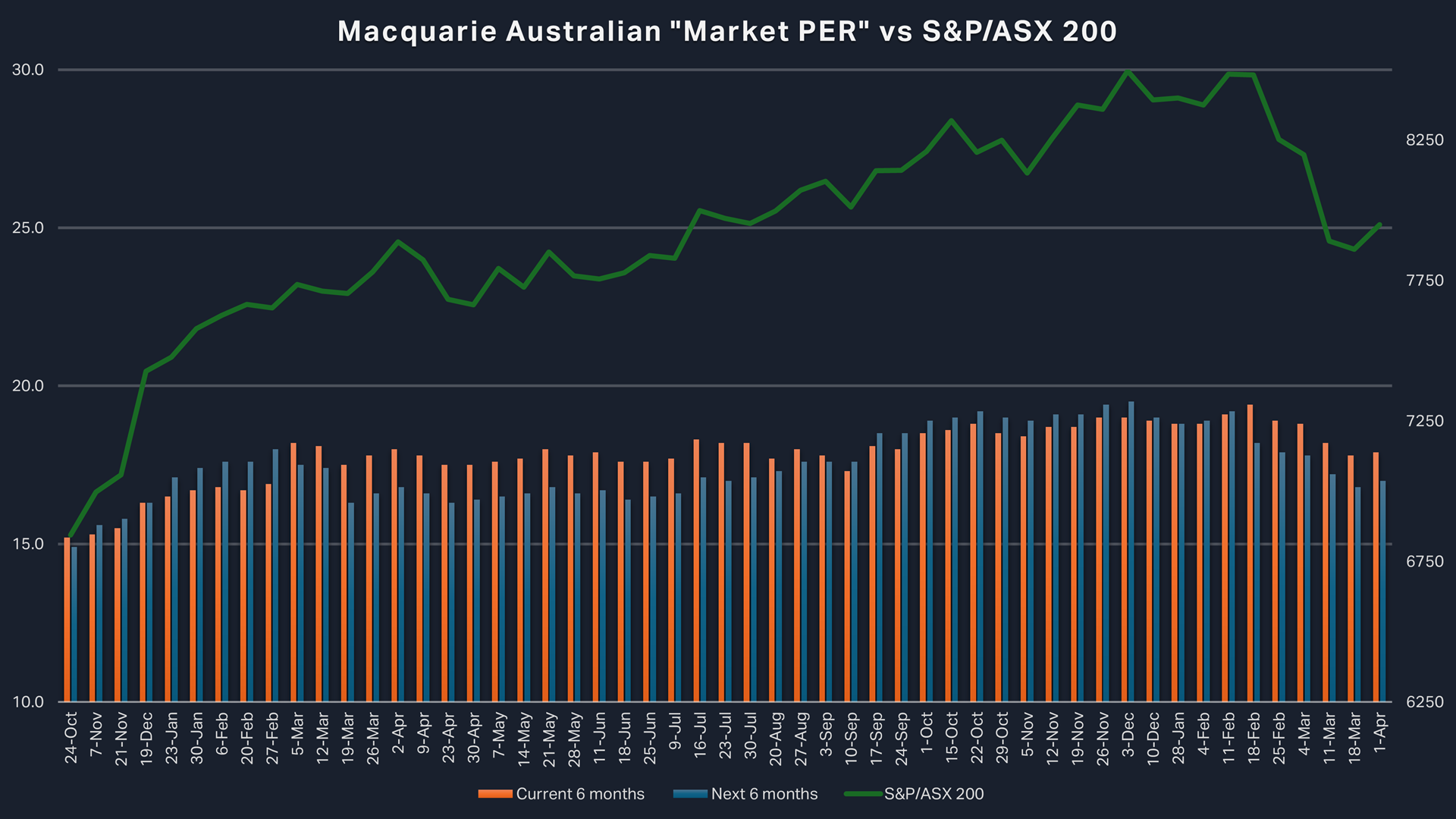

My favourite way to get an idea of whether the Australian stock market is currently cheap or expensive is to look at major broker Macquarie’s “Market PER”. It’s a forward-looking P/E Ratio for a basket of Australian stocks representing the largest ASX-listed companies accounting for the bulk of the ASX’s market capitalisation.

Earlier this week, Macquarie noted its Market PER for the current financial half-year ending June 30 was 17.9x, and for the next financial half-year ending December 31 it was 17.0x. So, just using the old rule of thumb, even after their recent correction, Aussie stocks still appear to be on the wrong side of fair value – albeit modestly when considering next half-year’s Market PER of 17.0x.

{kind=link}

According to Macquarie’s Market PER, valuations on a next-6-month basis have improved by around 12.8% compared to the metric’s peak of 19.5x set in early December. So that, at least, is some good news for those looking for a value-based entry here – but arguably there is still a long way to go until Aussie stocks could be considered “cheap”.

Do the charts say it’s time to buy ASX stocks?

If you wait for a bargain – it may never come! So let’s turn our attention to the technicals – the charts.

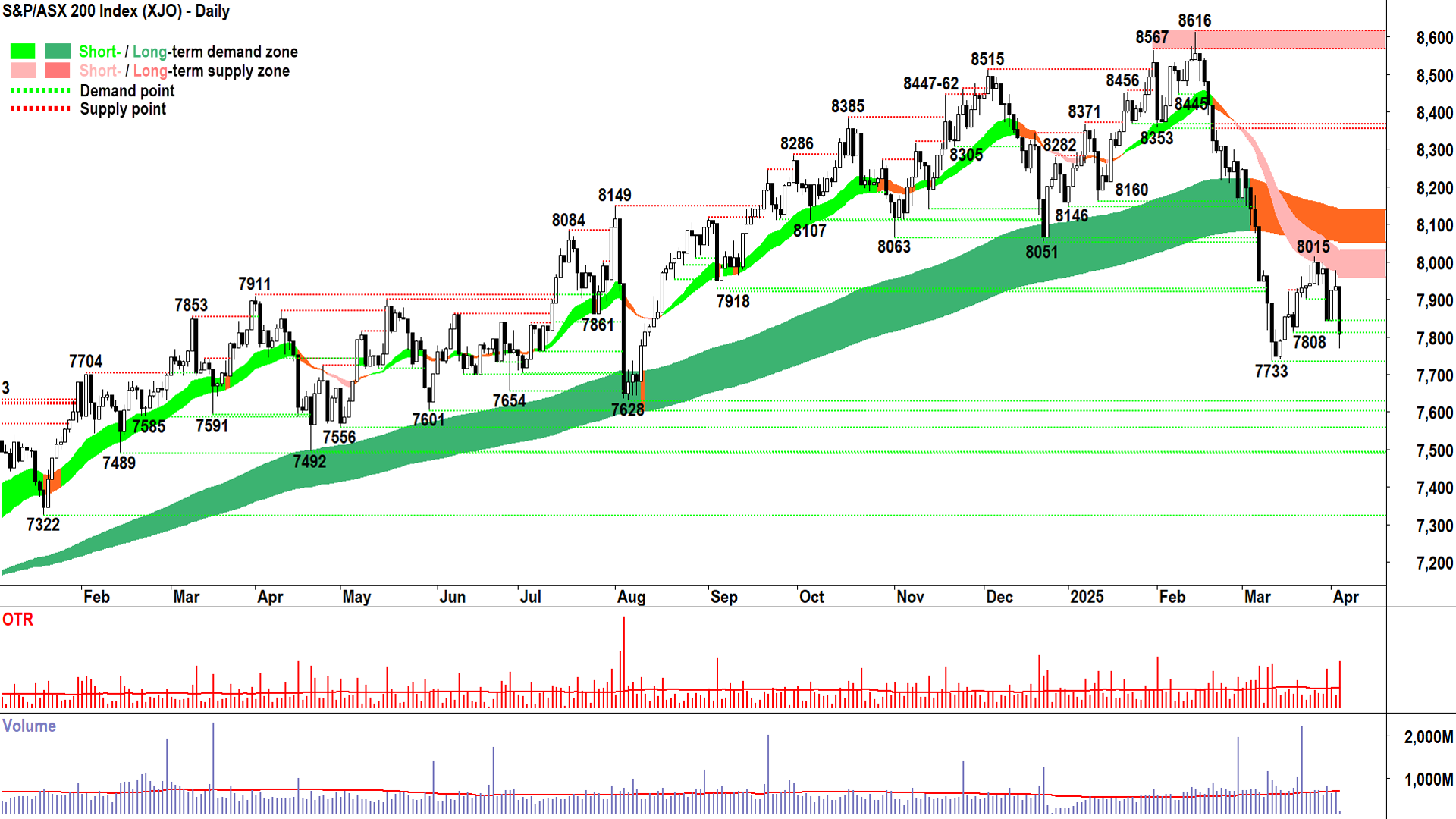

If you follow along with my ChartWatch write ups in each edition of our Evening Wraps, then the current state of the ASX 200 would be no surprise to you at all. More than likely, you would have observed, as I did in ChartWatch, the key technical signals that indicated many weeks ago the short term uptrend in Australian stocks, and then the long term uptrend, was changing.

I will be brief here, but you may wish to check out my ChartWatch Primer for more details on how my technical model works. The first indication that something was “off” with the ASX 200 came on 20 February when a series of supply-side candles (i.e., black-bodied and or upward pointing shadows) caused the its price to close below the short term trend ribbon (light green).

%20chart%203%20April%202024%20Source%20Market%20Index.png)

%20chart%203%20April%202024%20Source%20Market%20Index.png){kind=link}

That short term trend ribbon subsequently neutralised (amber), and then turned down (light pink), and soon, the ASX 200 repeated the same process at the long term trend ribbon (dark green to amber). This is a strong indication the supply-side of the market was growing in prominence and control.

At the same time, the price action switched from rising peaks and rising troughs (i.e., supply removal and demand reinforcement) to falling peaks and falling troughs (i.e., supply reinforcement and demand removal). The candles have remained predominantly supply-side in nature since.

At various points along this transitional journey – from demand side control prior to the 8616 peak on Valentine’s Day, to the current failure to reclaim the long term trend ribbon – I have noted my preference to move step-by-step to what I call my most conservative risk level – a maximum of two-thirds cash.

As for what happens next in the chart – I haven’t the foggiest! This is because I am a trend follower, not a trend prognosticator. Nobody can tell the future – not even the great Warren Buffett! So I don’t make predictions.

Simply, I just follow the trends I can see. More specifically, I look to manage my risk in accordance with how the smart money is controlling prices. If my analysis suggests they are creating an environment of excess supply – as is the case right now – I prefer to operate at maximum conservatism levels, but to also actively seek out a few strategic short selling opportunities.

I will not increase my risk settings until I see the smart money is again creating an environment of excess demand. Signs of this would be a return to:

- Prices above the trend ribbons and the trend ribbons rising, the trend ribbons are supporting the price on pullbacks

- Rising peaks and rising troughs

- A predominance of demand-side candles (i.e., white-bodied and or downward pointing shadows)

Short selling in a correction or bear market can be extremely lucrative, but it is not for the ill-prepared. I wrote a dedicated article on the practice back in December which you may wish to read. (Pretty good timing – but I suggest given current circumstances it’s still as much!)

As for what to short, well I’ve got you covered there as well. Many of my followers like to use my ChartWatch ASX Scans lists to identify potential short selling opportunities. I publish both Uptrends and Downtrends – the latter is the one you might want to keep an eye on for shorts!

Conclusion

When you think about it, together, corrections and bear markets are a rather common occurrence – hitting markets by orders of magnitude every 18 months. So, if you don’t yet have a strategy for dealing with these disruptions, then you probably should.

Sure, the market is substantially higher today than it was 45 years ago, and one could argue one could just ride it out…don’t worry…it will go back up again…

But getting corrections and bear markets wrong or right can make a big difference. Let’s assume you were able to reduce the impact of corrections and bear markets by just half since just the year 2000 – you would have ended up over 300% ahead.

.png)

.png){kind=link}

There’s clearly plenty at stake when it comes to navigating major market downturns, particularly should this correction turn into another bear market. One could argue that there are just as many contributing uncertainties this time compared to previous market calamities.

As the saying goes, to be forewarned is to be forearmed. You just got warned. What are you going to do about it? Hopefully this article serves as a great starting point!

This article first appeared on Market Index on Thursday 3 April 2025.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

Never miss an update

Get the latest insights from me in your inbox when they’re published.

5 topics

8 stocks mentioned

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets