The bull market nobody’s talking about

There's no cure for low prices like low prices, and if you're looking for low prices, uranium has suffered some of the lowest of any commodity in recent years. Uranium reached a low of US$18/lb at the end of 2016, a far cry from the US$130/lb it fetched in 2007. Given nearly all the world's mine-supply of Uranium is produced at cash costs of US$25/lb+, this was clearly not sustainable.

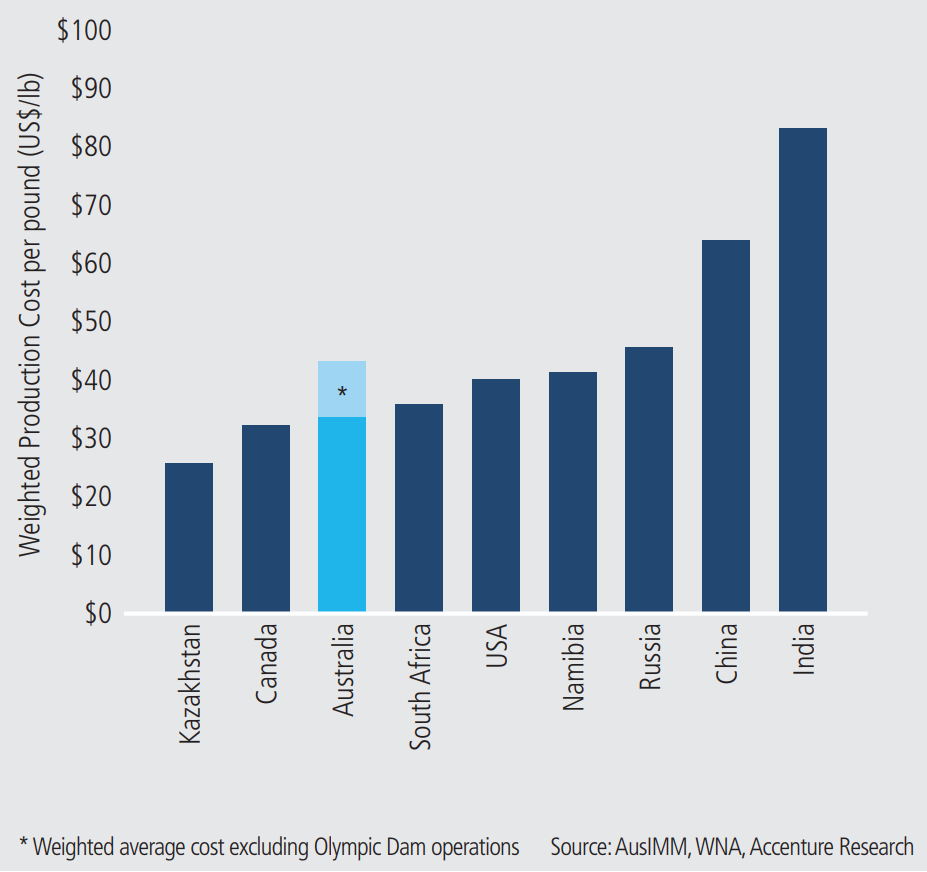

Source: National Energy Resources Australia – Uranium Industry Competitiveness Assessment

The shutdown of Japan’s entire fleet of nuclear reactors had left the market with an excess supply. Meanwhile, low prices encouraged ‘secondary supply’, where enrichment plants would reprocess ores to extract additional nuclear fuel. This excess supply has kept prices low for longer than many expected, but the balance in the market has begun to change more recently.

There has been increasing chatter among investors, including on Livewire, about the possibility of another bull market in uranium. In the past few months, we've heard from Michael Goldberg at Collins Street Value Fund, Nigel Littlewood at Harness Asset Management, and even resources legend Rick Rule from Sprott US Holdings about the opportunity. But what seems to be overlooked in more recent articles is the fact that, by traditional definitions, uranium is already in a bull market.

“The International Energy Agency suggests that the global cost to produce yellow cake – not the AISC, but the real cost; adding back prior-year write-downs, and accounting for cost of capital – is about US$60/lb. So, we make the stuff for 60, and we sell it for 25.” – Rick Rule, President and CEO, Sprott US Holdings.

A bull market? Isn’t that hyperbole?

The generally accepted definition for a bull market is that prices have risen by more than 20%. Uranium bottomed at around US$18/lb roughly 18-months ago, and while there have been a handful of commentators suggesting a bull market is coming, few seem to have identified that (by this definition) it’s already begun.

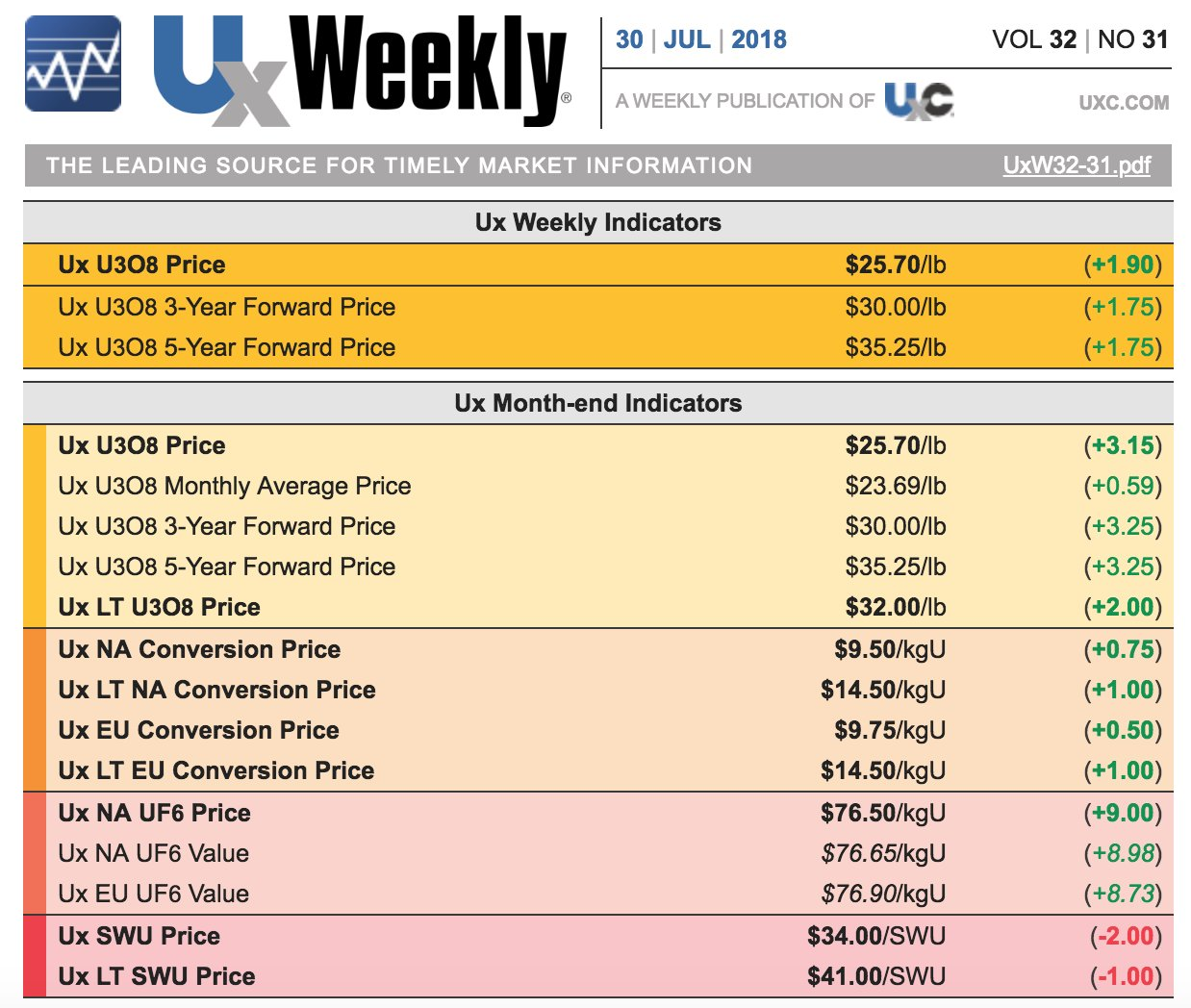

At the end of July 2018, the spot price of uranium was US$25.85/lb. This is more than 40% up from its lows, well and truly meeting our definition of a bull market.

“Significant supply and demand imbalances exist for uranium which, we expect, will push the price back up to at least $50-60/lb by 2020-2022.” – Nigel Littlewood, Harness Asset Management

“Not only does the fundamental mismatch in cost and price suggest a change is imminent, but the underlying buyers of yellowcake are insensitive to price… There is every reason to believe that investors in the right uranium businesses will benefit greatly in the coming twelve months or so… In short, I’ve never seen a commodity with so many fundamental factors working in its favour.” – Michael Goldberg, Collins St Value Fund

What’s changed?

Late last year, the two largest (and lowest cost) producers globally, Kazatomprom and Cameco, announced huge production cuts. In November, Canadian major Cameco announced the temporary suspension of the world’s largest uranium mine at McArthur River, removing 10% of global supply (18m lbs). Less than a month later, Kazakhstan’s state-owned miner, Kazatomprom announced that it would slash production by 11,000 tonnes, or 7.5% of global supply. At the end of July 2018, Cameco announced that the shutdown of McArthur River would be indefinite and placed the project into care and maintenance.

Despite the production cuts, Cameco is contractually bound to deliver 39-40m lbs of uranium to its clients in 2018, and 25-27m lbs in 2019. Following the cuts, Cameco now produces a mere 9m lbs p.a., so where’s the balance to come from? While 2018 saw them drawdown a significant amount of their inventory, Cameco is now purchasing uranium on the spot market to meet demand. In 2018 they’re planning to purchase 2-4m lbs, but from 2019 that number jumps to 9-11m lbs.

Other production cuts include:

- Cameco’s Rabbit Lake (4m lbs p.a.)

- Cameco’s US operations (2.5m lbs p.a.)

- Areva’s Somair and Cominak mines in Niger (1m lbs p.a.)

- Paladin’s Langer Heinrich mine (4m lbs p.a.)

Source: Shard Capital research note on Boss Resources

Source: Shard Capital research note on Boss Resources

In addition, a number of new funds have been launched recently with the intent of buying physical uranium on the spot market. The largest of these is Yellow Cake (LSE:YCA), which recently raised 150m Pounds Sterling with the intention of buying 8.1m lbs of uranium.

Nigel Littlewood told Livewire that the situation for uranium is similar to thermal coal before the price spike. "There's no new investments in nuclear in the West. Countries like the US and France will allow their old reactors to run down and won't rebuild, but this is already priced in. On the other hand, nuclear power is still ascending in the East."

He expects stable to increasing demand over the next 2-5 years, but for supply to remain tight. "It's a compelling risk/reward situation," says Littlewood.

“If we look out five or six years, because despite the fact that people around the world hate it, people like when they flick the switch and the lights go on. Even rich markets like the US, which alleges that it can do without power it doesn’t like, uranium still provides 15% of base-load power. If the price of the commodity doesn’t go up enough to cover its cost of production, five or six years from now the lights go out.” – Rick Rule, President and CEO, Sprott US Holdings.

Japan

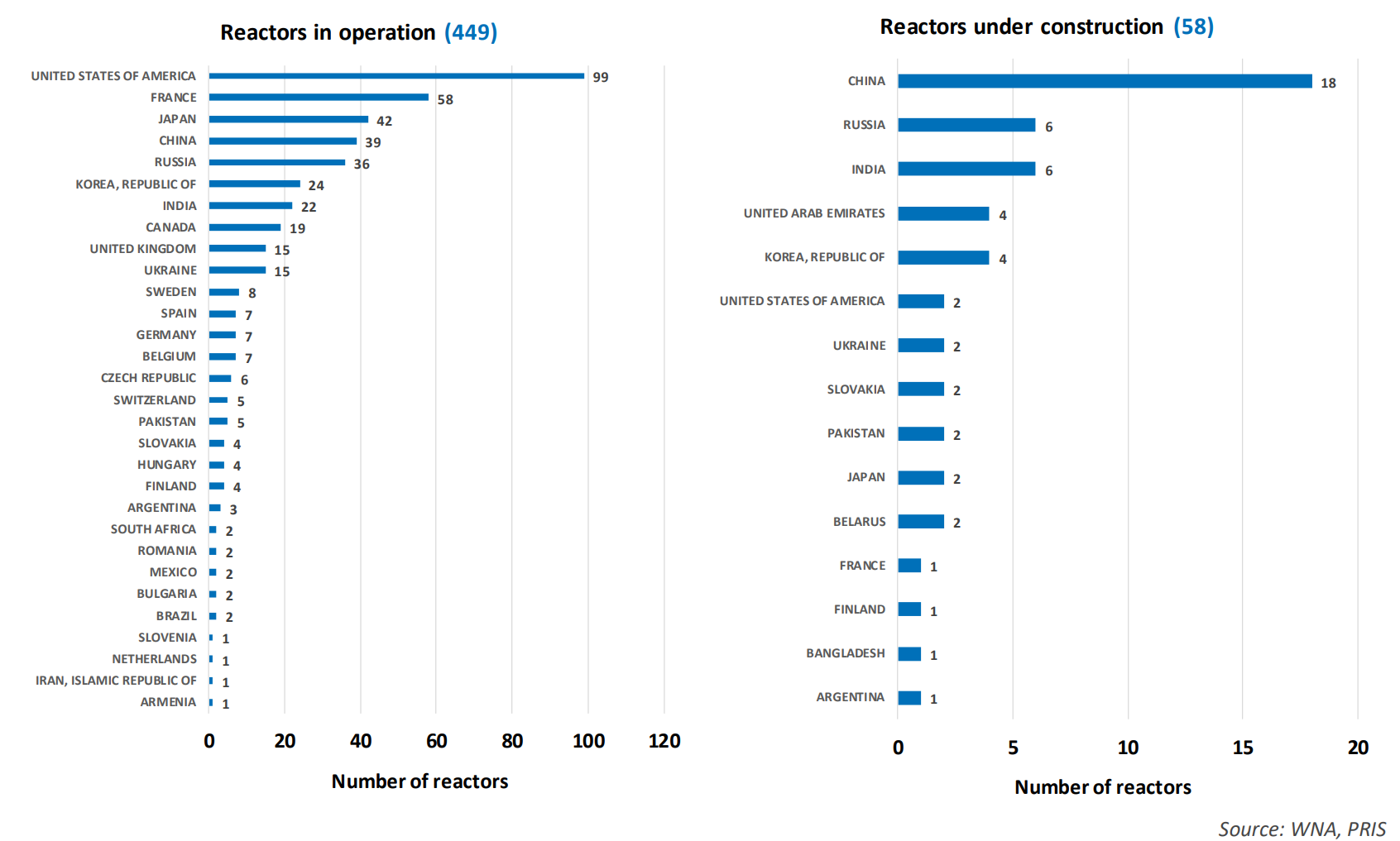

One of the biggest factors in the bear market has been the glacial pace of Japan’s reactor restarts. It’s been nearly five years since investors first started making noise about reactor restarts, but August 2015, the first reactor was officially restarted. Since then another eight reactors have been restarted. While this is a far cry from the 54 reactors operating in 2011, momentum appears to be slowly building.

The Japanese government approved its new Basic Energy Plan on 3 July 2018, which confirms that nuclear will remain a key part of their energy mix for decades to come. According to the plan, nuclear energy will make up 20-22% of the country’s power generation until 2030. Achieving this level of nuclear output would require the restart of around 30 reactors.

Littlewood believes that Japan could be the "big question mark in the thesis", as there is still significant internal resistance to reactor restarts. However, a recent byelection showed support for the Abe Government, which is pro-nuclear. This suggests that Japanese voters are happy to vote for a pro-nuclear party.

“Japan is determined to make a positive contribution to enhancing the safety of nuclear energy and the peaceful use of nuclear energy” – Japan’s Basic Energy Plan

The contracting cycle

Uranium is primarily sold via long-term contracts between miners and utilities. The contract prices are generally set at a premium to the spot price. The long-term nature of the contracts, and the fact that many of these contracts were signed during the last bull market (’07-’10) means that many of these utilities are expected to re-enter the contract market in the coming years, creating a significant amount of uncovered demand.

Littlewood said that understanding the contracting cycle is one of the more difficult parts of researching the investment case. There are no central data sources to gain an understanding of the timing of contract negotiations. Based on his research however, most long-term contracts should be up for renewal at some point in the next three years.

July 2018 saw the largest one month increase in long-term uranium prices since November 2014.

Source: Purepoint Uranium Twitter account

“While the demand for uranium is fairly steady and predictable, the procurement decisions of utility companies can vary based on the level of current contract coverage, existing inventories, forecasts of future prices and risk tolerance. The previous contracting cycle, brought on by uranium price spikes in 2007 and 2010, resulted in utilities rushing to contract at higher prices and for very long terms. While these old contracts are expiring, the utilities have not been moving to replace these contracts and the forward coverage of utilities have therefore fallen appreciably, resulting in uncommitted needs continuously building. UxC reports that these unfilled needs may total just under one billion pounds of U3O8 over the coming ten years and over 81% of expected reactor requirements are uncovered by 2027.” - Uranium Participation Corporation

“The recent relationship post the 2007 uranium bubble, between the spot price and long-term contract price has shown an average premium for long-term prices of around 25%; this differential indicates that a spot price of around US$48/lb would be consistent with the long-term contract price of US$60/lb.” – Vimy Resources

Incentive price

For new mines to be built to meet future demand, they must make economic sense. This means that the price of uranium must not just be higher than production cost, but needs to compensate investors for risk, and the time-value of money. Even after the recent improvements in price, the current spot price and contract prices remain far below the incentive price.

“The incentive price for meaningful new uranium production (new developments or mine expansions) to come to the market is estimated by BMO, in their March 2017 uranium market outlook, to be higher than US$60 per pound U3O8.” – Uranium Participation Corporation

“Should demand ultimately prove to be closer to Vimy’s Upper Case, then a long-term price of US$60/lb is unlikely to incentivise sufficient new production to replenish depletion of existing production and to meet increasing new demand. Accordingly, at a US$60/lb long-term contract price, it is foreseeable that further deficits will occur, leading to a further escalation in prices beyond Vimy’s price assumption.” – Vimy Resources

Which companies offer exposure?

Among the major Australian miners, both BHP and Rio Tinto own uranium assets. However, they form a relatively small part of the big miners’ portfolios, being dwarfed by iron ore, coal, and copper.

Cameco is the largest listed, pure-play uranium mining company in the world. Cameco is traded on both the Toronto Stock Exchange, and the New York Stock Exchange.

ASX listed, uranium-focused companies:

- Paladin Energy (ASX:PDN) - Placed in Care & Maintenance in May.

- Energy Resources Australia (ASX:ERA) - Permanently closed, processing stockpiles.

- A-Cap Resources (ASX:ACB) - Exploration, Preliminary Feasability Study expected in 2018/2019.

- Berkeley Resources (ASX:BKY) - Construction recently begun.

- Bannerman Resources (ASX:BMN) - Definitive Feasability Study complete, pilot plant complete.

- Boss Resources (ASX:BOE) - Care & Maintenance, restart recently announced.

- Deep Yellow (ASX:DYL) - Exploration, measured resource, scoping study not yet completed.

- Peninsula Energy (ASX:PEN) - In production.

- Toro Energy (ASX:TOE) - Preliminary Feasability Study completed.

- Vimy Resources (ASX:VMY) - Definitive Feasability Study completed, trial mining completed.

Sources and further reading

- Livewire interview with Rick Rule

- Nigel Littlewood - Betting on the perfect storm

- Michael Goldberg - Like buying oil at $20 a barrel

- Nuclear Power In Japan - World Nuclear Association

- Cameco Investor Presentation

- Vimy Resources Uranium Market Summary

- Nuclear reactor restarts likely as Cabinet OKs new energy plan - The Asahi Shimbun

- Boss Resources research note by Shard Capital

- Uranium Industry Competitiveness Assessment - National Energy Resources Australia

- Uranium Market - Uranium Participation Corp

- This Year, Everyone Will Love Uranium - Oilprice.com

- Twitter post by Purepoint Uranium

- Uranium Week: Price Jump - FNArena

- Bannerman Resources presentation

Disclosure: The author owns shares in some of the companies mentioned.

Disclaimer: This article is not financial advice and should not be viewed as an endorsement to trade in any of the stocks mentioned, any derivatives, nor any physical commodities. Investors should seek financial advice from a licensed advisor before making investment decisions.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life.

Patrick was a Market Analyst, Editor, Senior Editor, and Managing Editor at Livewire Markets between 2015 and 2022. He was the Content Director and a member of the Investment Strategy & Research Group at Betashares between 2022 and 2024. He is an expert on listed products, commodities, and investment strategy, with a particular interest in gold and uranium,.

2 topics

12 stocks mentioned

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life. Patrick was a Market Analyst, Editor, Senior...

Expertise

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life. Patrick was a Market Analyst, Editor, Senior...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

This recently triggered market signal has never failed to predict gains

Ophir Asset Management

Equities

Meet the perfect investor (and how you can beat them)

Livewire Markets