We have not made any tactical changes to portfolios this month after last month’s decision to trim equities. We remain modestly overweight risk, led by our positioning in domestic equities and international corporate credit. While data indicates record collapses in Q2 growth lie ahead, more up-to-date data paints a picture of recovery. How sustainable that is remains uncertain, given recent virus outbreaks and renewed geo-political risks.

In this wire, we look at the outlook for real assets and how they can help build less expensive resilience into portfolios (relative to more traditional bonds). With portfolios being buffeted over the past few years by heightened market volatility, elevated geo-political risks, and a seemingly increased array of unforeseen events (such as pandemics), building quality and resilience into portfolios should be front of mind for investors.

First, an update on recent market

developments…

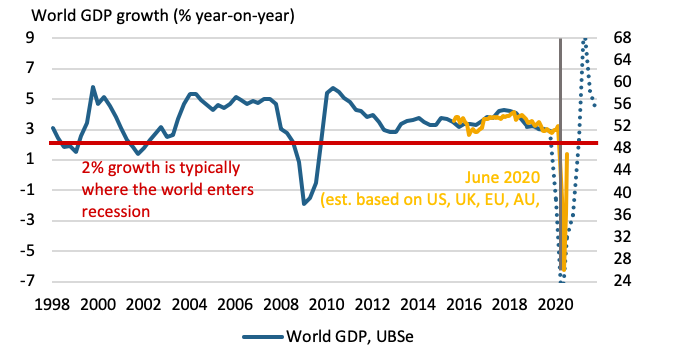

Q2 2020 now looks to be the focal point of a sharp and deep pandemic-led recession. Weakness in consumer spending and rising unemployment point to an almost universal (and in many cases record) collapse in Q2 growth of 6-10% for most developed economies. However, more up-to-date data and a pick-up in leading indicators as activity restrictions have been eased (see the following chart) suggest Q3 growth is likely to record a strong rebound. But uncertainty remains over how sustained this will be, reflecting tapering Q4 fiscal support and the cautious recovery of consumers. Also, other risks have re-emerged, including the acceleration of outbreaks of COVID-19 through key emerging economies (particularly Brazil and India) and a recent significant outbreak post the easing of lockdowns in the US (and Australia). Geo-political tensions between the US and both China and Europe have also risen.

While equities rallied and bond yields rose into mid-June, these risks led to a modest pull-back in risk appetite. We have not further reduced risk, as we did last month. We remain modestly overweight equities relative to fixed income, with an overweight in domestic equities and international corporate credit.

Given recent gains, the risk of a correction in equity markets in the short term remains. But on our tactical six to 12-month horizon, we believe risk appetite will be well supported. This reflects our anticipation that the world will avoid a second round of activity lockdowns, that global interest rates will stay low, and corporate earnings expectations will trough and slowly rise.

Rising leading indicators signal an eventual

global growth recovery

Source: Factset, UBS, Crestone.

The outlook for real assets

With portfolios being buffeted over recent years by heightened volatility, a plethora of geo-political risks and a seemingly increased array of unforeseen events (such as tariff wars and pandemics), building resilience into portfolios should be front of mind for investors. Alternatives, with an expected lower correlation to traditional asset classes, are a way to achieve this, increasing diversification as well as potential risk-adjusted returns.

We classify alternatives under three broad sub-sectors: hedge funds, private equity and real assets. Real assets typically refer to investments in unlisted real estate, infrastructure and sustainable resources, and exposure is accessed through both equity and debt opportunities. As Brookfield, one of the world’s largest real assets managers, notes, real assets form the backbone of the global economy, being tied to global growth and macro trends. Commodities (such as gold) are also considered real assets.

“Alternative investments can provide many benefits to investors, ranging from potentially higher returns to lower risk and better diversification than may be available from a traditional portfolio.” - Blackrock Inc.

Real assets possess a range of characteristics that can underpin the cashflow of these investments (and returns) during periods of economic expansion and contraction. Being ‘physical’ or ‘tangible’ assets, they can provide real inflation-protected returns when demand is rising. And given many of the assets represent essential goods and services driven by end-use demand, cashflows can be quite defensive through periods of economic downturns. Real assets demand attention in an investor’s portfolio for two key reasons.

As an alternative uncorrelated investment, real assets are an important part of a well-diversified portfolio. As JPMorgan notes, “stable and high-quality income streams from core real estate and infrastructure investments provide a strong offset against their lack of liquidity for investors who are able to hold these assets through the cycle”.

Real assets have the potential to lower the overall cost of providing a defensive ballast to portfolios through volatile markets. Real assets are typically at the more defensive end of the risk spectrum (like sovereign bonds). However, unlike many zero-yielding sovereign bonds, real assets continue to retain a relatively attractive expected total return of 5-6%.

On the latter point, with traditional asset classes more recently tending to gravitate toward expensive valuations, and sovereign bonds—typically leant on for their defensive characteristics—now coming at a real opportunity cost to portfolios (given minimal running yield), real assets are increasingly being considered as an additional means to build cost-effective resilience into portfolios (given they can still provide relatively attractive income).

It is also worth highlighting that, in a world where inflation has more recently been lower, the inverse correlation between sovereign bonds and equities has also been lower (i.e. bonds have potentially become less effective portfolio diversifiers in a low inflation environment).

“The (real assets) asset class has proven its value by providing reliable long-term total returns, inflation protection and the ability to offset the volatility of equity and fixed-income investments.” - Bruce Flatt - CEO, Brookfield

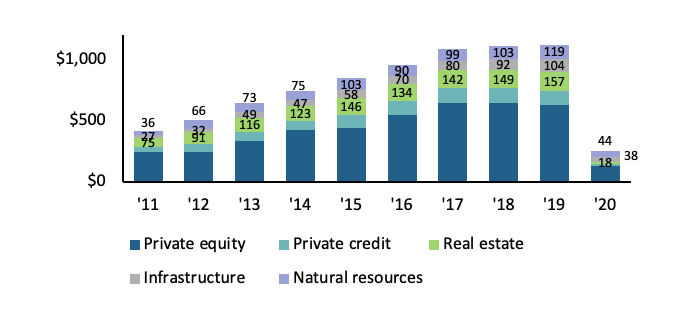

The chart below shows that, while the overall allocation of capital to private markets has levelled out over the past couple of years, capital directed to real estate, infrastructure and natural resources has continued to rise.

Global private capital fundraising (USD billions)

JPMorgan Asset Management. Fundraising categories provided by Preqin and represent its estimate of annual capital raised in closed-ended funds. Data may not sum to total due to rounding. Data based on availability as at 31 May 2020.

Real

assets through the COVID-19 correction

The impact of the pandemic on the world economy was somewhat unique— not only because of the unexpected and unprecedented nature of the human catastrophe, but also because of the way many cross-asset correlations became elevated, and some defensive assets proved less defensive ‘for a time’ at the height of the crisis. While real assets initially provided attractive relative downside capture, the extent of the dislocation in markets eventually saw selling pressure, erasing much of that initial outperformance.

But, according to Brookfield, while many sectors are seeing short-term cashflow disruption, no significant long-term value decline is anticipated. The long-run equity beta of real assets remains less than one, at 0.22 for unlisted real estate and 0.10 for infrastructure (from 2004-2016). Many alternative real asset sectors are now trading at a discount to long-term valuations and some are likely to inherit tailwinds as a consequence of the pandemic.

“Core real estate has high quality, relatively transparent income streams, which in the current environment are well above core government bond yields.” - JP Morgan, January 2020

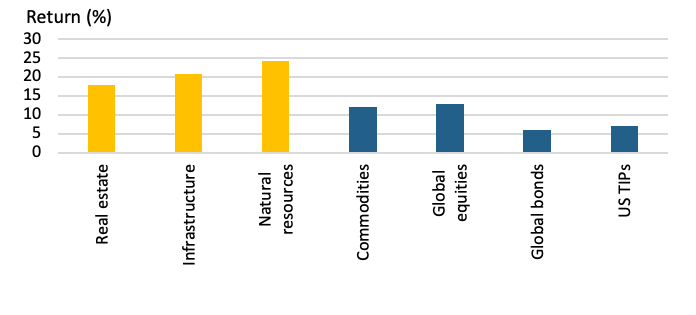

Real assets hedge against inflation surprise

While inflation is currently depressed, history reveals it can emerge without warning. As Brookfield notes, “for this reason, long-term investors can benefit from allocations that generate cashflows with a positive sensitivity to changes in inflation.” As real estate contracts usually have inflation-linked rent increases, revenues typically respond favourably to higher inflation.

Real assets perform well in periods of positive inflation surprise

Source: Morningstar, Bloomberg, Brookfield Investment Management, US BLS, Federal Reserve Bank of Philadelphia SPF. Data range represents 2004-2016.

Real estate assets help stabilise cashflows through the cycle

Alternative real estate involves exposure to unlisted property assets (typically split across commercial, retail and industrial segments). Investments can be direct or through a manager that facilitates a portfolio of investments, ranging from open-ended funds with periodic liquidity to closed-end structures.

While real estate investments can experience drawdowns during recessions and are not readily converted to cash, they can help stabilise a portfolio’s income and cashflow through the cycle (particularly compared with current low-yielding sovereign bonds). And while real estate can exhibit significant economic volatility, its accounting volatility can be lower, due

mostly to its more lagged quarterly reporting frequency.

Investors should ensure they have a significant allocation to core real estate to smooth economic volatility. Such investments embody high quality tenants and long-term rental agreements in gateway markets. Not only does this have a low correlation to traditional markets, it typically has a low correlation between different global regions (and lower dispersion among managers). Looking ahead, there is likely to be a range of long-term, as well as post-virus return drivers across the unlisted real estate sub-sector:

Office—commercial office returns

have always been strongly linked to economic growth and should benefit from a

synchronised global pick-up through late 2020 and 2021. Persistent low rates

globally should also support valuations. It remains too early to assess the

long-term impacts of an increased trend in working from home, and there are

offsetting drivers, such as more floor space to meet social distancing

requirements and trends toward more open-plan office areas.

Retail—the pandemic has likely

accelerated the shift away from bricks and mortar retailing, potentially

pressuring long-term valuations. Short-term headwinds from retail consolidation

and rent abatements are also likely to weigh on the sector for some time.

Industrial—including warehouse,

logistics and distribution centres, this sector is likely to benefit from the

shift to online purchasing, as well as the trend toward more localised

manufacturing.

“Investors looking for security of income from unlisted property should focus on high quality assets leased to defensive, essential services and resilient industries and tenant customers, on long-term leases.” - David Harrison, CEO Charter Hall

Demand for infrastructure is likely to underpin returns

While the allocation to real infrastructure assets has grown significantly, it has come from a relatively low base. While this has still led to some compression in returns, it is expected to remain relatively attractive compared to traditional asset classes. Infrastructure investment projects, while not liquid, could be suitable diversifying safe assets for specific long-term investors who can harvest their illiquidity premium. It is also worth noting that infrastructure investments often align closely with investors’ desires to invest with an ESG (environmental, social and corporate governance) or sustainability framework.

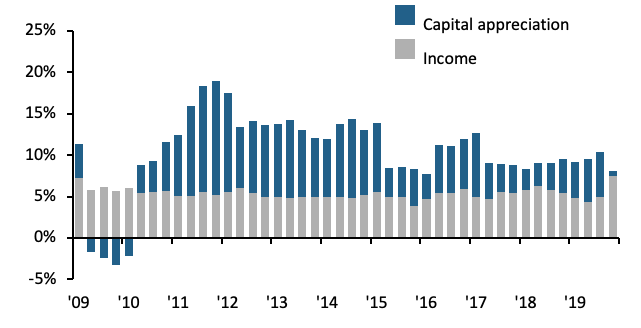

JPMorgan believes that, in a late-cycle environment, investors should concentrate on assets that fit the established definition of ‘core’, chiefly the ability to provide clear visibility into long-term yield (the chart below shows return split between capital and income). True core infrastructure assets can offer low volatility, low correlation to equities and fixed income, and reliable cash yield streams. There are five key areas of private infrastructure—utilities, renewables, transport, energy and telecoms, with the first three tending to attract most capital.

For the better part of a decade, and in particular over the last five years, institutional investors have increasingly embraced the potential of equity investment in core private infrastructure assets: diversification, inflation protection and yield. - JP Morgan, January 2020

Looking ahead, demand for infrastructure is likely to underpin returns, with McKinsey estimates suggesting global annual spending will need to rise (to keep pace with economic growth) from about USD 2.5 trillion to about USD 3.3 trillion by 2030, led by telecoms, transport, power and water:

Utilities—this

segment is supported by relatively inelastic demand for residential and

commercial energy, with long-term regulated contracts that underpin rates

charged to consumers and make consideration for ongoing maintenance and capex

costs.

Renewables—the

desire to reduce carbon footprints and transition from fossil fuels supported

by regulatory initiatives will continue to see renewables remain a growing part

of the infrastructure space. Strong ESG investor support is also expected to be

a positive.

Transport—this is

essential infrastructure (road, rail, ports etc), often privatised through

concessional government contracts with allowances for capex and pricing growth

no less than inflation. There are also high barriers to entry. This sector

should rebound with economic activity, though some assets (airports) are likely

to face short-term cashflow issues.

Energy—these are

oil and gas pipelines, processing and storage facilities. It is supported by

long contracts (30 years) with limited impact of commodity price fluctuations.

The sector may face more structural headwinds from renewables and low

oil prices.

Telecoms—these are

often regulated investments with long-term (10-year) leases and inflation

escalation. There is proliferation of data use in general and the post-COVID-19

world would appear supportive of this sector.

As shown in the earlier chart, some infrastructure asset classes also perform

strongly during inflationary periods, particularly when rising prices are

spurred by economic growth and improving levels of employment and consumption.

Global core infrastructure returns

Source: GTA. Rolling four quarter returns from income and capital appreciation.

Diversify your portfolio through Alternatives

Crestone Wealth Management offers access to a range of strategies in the alternatives space, including hedge funds, private equity and venture capital, as well as structured products, warrants and other derivatives. Click the 'CONTACT' button below to find out more.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.