The next bluechips to cut their dividends

“You can hold a rock concert, and that’s okay. And you can hold a ballet, and that’s okay. Just don’t hold a rock concert and advertise it as ballet.” ~ Warren Buffet.

Yield traps are akin to a retiree couple thinking they’re attending ‘Swan Lake’ only to see Venom perform ‘Welcome to Hell’ after the curtain is drawn. High yield stocks are like ballet performances where investors expect steady and consistent dividends transitioning from one year to the next. However, the ballet can turn into a nightmare performance if the expectations of high dividends turn out to be yield traps.

Each year there are notable yield traps.

- In 2012, it was QBE.

- During 2012 to 2014, some consumer stocks turn out to be yield traps including David Jones and Myer.

- The year 2015 saw mining services stocks take an axe to their dividends, including Monadelphous and WorleyParsons.

- In 2016, BHP’s progressive dividend policy was scuttled and Woolworths and Origin Energy also cut dividends.

- In 2017, Telstra, the king of all income stocks slashed its dividend.

- The year 2018 saw Myer suspend its dividend.

As we look forward to FY19, are there any more yield traps on the horizon?

To answer this question, we must consider the three drivers for a dividend cut:

1: Cyclical and/or peak earnings

Dividends are paid out as a proportion of earnings and when earnings are under pressure dividends usually follow. Hence, investors must be wary of cyclical earnings. Commodity stocks are the epitome of cyclicality, with the ‘Big Australian’, BHP Billiton, cutting its dividend in 2016 when commodity prices collapsed. Furthermore, investors must be cautious of companies facing structural issues. For example, Telstra has the double whammy of losing its fixed line earnings to the National Broadband Network (NBN) and suffering declining mobile margins.

2: Weak balance sheet

Business Finance 101 teaches us that debt holders get priority to cashflows before equity holders. Hence, when it comes to corporate survival it’s an easy choice for management to pay debt holders first before equity holders. Shareholders of debt-fuelled growth companies unfortunately know this too well. History is littered with many corporate zombies loaded with rising debt levels such as QBE Insurance and, in recent times, Vocus Group.

3: High dividend payout ratio

The higher the payout ratio (dividends as a proportion of earnings) the greater the likelihood of a dividend cut if earnings decline. In 2015, both BHP and Telstra had about a 100% payout ratio, which were then rebased to more sustainable levels in subsequent years. In 2018, Myer suspended its dividend when the company realised that future earnings were going to be substantially lower than the 2017 dividend.

While weakness in any one of these metrics may not lead to a dividend cut, the more a company exhibits these characteristics the greater the likelihood of a cut. Based on the above considerations our two picks for FY19 yield traps are:

National Australia Bank

From an earnings perspective, the outlook for National Australia Bank (NAB) is relatively benign (barring a recession). Hence, superficially it seems that their dividend is sustainable.

However, NAB is walking on a tightrope in managing high dividend expectations. With the weakest balance sheet and highest payout ratio compared to the other major banks, there is little room for error for NAB.

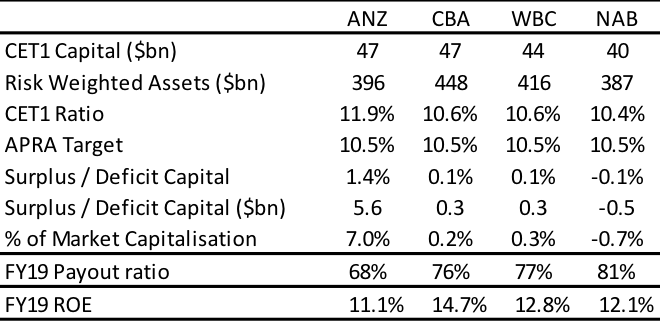

Chart2. Major Bank Proforma Capital Metrics

Source: Vertium, Factset, ANZ, CBA, WBC and NAB

Based on Australian Prudential Regulatory Authority’s 2020 target capital (CET1) ratio, NAB is the only bank that currently has a capital shortfall. Given that NAB’s ROE is relatively low and its payout ratio is high the company is simply not retaining enough earnings to replenish its balance sheet.

A tight balance sheet makes it difficult to tolerate even small shocks to the business. In a volatile world, management may be forced to protect the balance sheet rather than maintain the dividend.

We estimate that NAB may cut its dividend by 10% from $1.98 to about $1.80 if its payout ratio changes from 81% to 75%. Hence, the current 7.3% dividend yield may prove to be an illusion. A dividend cut looms large for NAB.

Telstra

Telstra has taken the headline as one of the biggest yield traps in recent years and unfortunately will continue to do so in FY19.

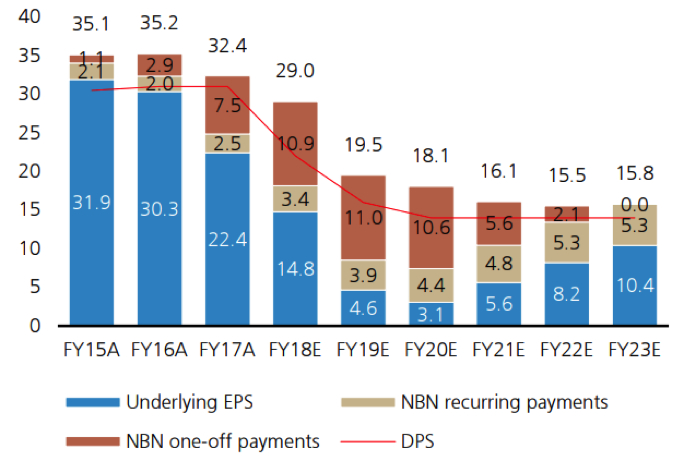

Despite Telstra having a strong balance sheet, in 2017 the company revealed that the NBN would gouge giant earnings hole in the future. This was the key reason why Telstra rebased its dividend from 31 cps to 22 cps.

In 2018, it became clear that Telstra cannot sustain its world beating mobile margins. At Telstra’s recent strategy day, its FY19 profit guidance highlighted that its FY18 dividend of 22 cps is unsustainable. Using UBS’ earnings forecasts and Telstra’s payout ratio guidance (75% for NBN one-off payments and 80% of core earnings), it is likely that the FY19 dividend will be around 15 cps. Moreover, future dividends are also likely to be lower.

Chart1. Telstra EPS Breakdown

Source: UBS

Due to the structural earnings decline, Telstra will be a shadow if its former self in terms of valuation and dividends.

Conclusion

Dividends are an essential component of investment returns, but chasing yield can be a very dangerous investment strategy. Investors need to avoid yield stocks with high payout ratios, weakening balance sheets, and/or peak cycle earnings otherwise they are picking up pennies in front of a steamroller.

If the dividend is under threat one will need the nimbleness of a ballet performer to exit just in time and avoid being steamrolled. Not everyone is that light-footed and for many it can be an unwelcome investment hell.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

1 topic

2 stocks mentioned

Vertium Asset Management

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Expertise

Vertium Asset Management

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

This recently triggered market signal has never failed to predict gains

Ophir Asset Management