This crisis has only just begun...

We believe markets are still overly optimistic and are failing to properly consider the ongoing challenges. As such, the current bounce may prove to simply be a bear market rally off the recent panic lows.

In February, we warned that the coronavirus could be a significant issue, writing that investors were too complacent and that the coronavirus could prick the 'bubble in everything'.

That bubble is now deflating, and the world has changed as the delusions of the past struggle to remain relevant. The crash was incredibly rapid and alarming, highlighting both the nature of the shock and the fragility of markets.

As we lay out in this wire, while markets are enjoying a relief rally, we believe that this crisis has only just begun and investors should prepare for a long, challenging period ahead.

Government responses leave much to be desired

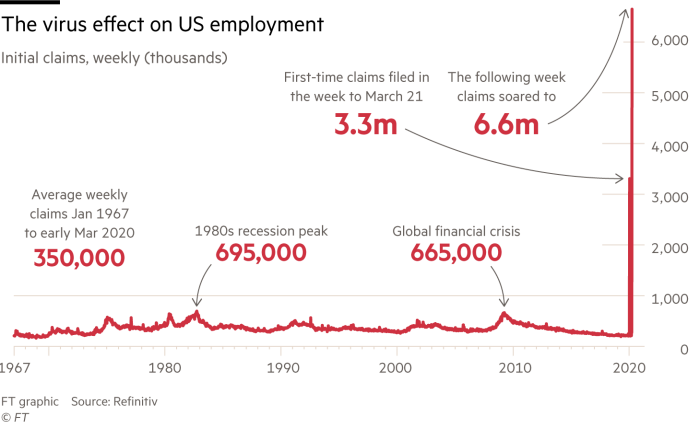

Based on the US unemployment claims seen in recent weeks, the unemployment data will likely be equally concerning. The ability to get our economies back to previously accepted norms will be as well.

The coronavirus crisis and its various feedback loops have been a very challenging situation to analyse for investors.

This is because the response by the government was integral to the response by markets and because data and information were ever-changing, unreliable and somewhat difficult to analyse.

The situation should have been a relatively easier assessment for effective leaders to grasp. Having been constantly assessing the situation in real-time, we were surprised at the initial tardiness of the public health responses of many governments worldwide, which have left much to be desired in our opinion.

This will hurt future trust in government and certain political leaderships – as will their dramatic financial and economic actions. One example was the risks posed to the population by continuing to allow inbound travel from affected regions while the magnitude of the threat was unknown and while knowing how seriously China had eventually reacted to the threat in late January.

This would have been calamitous if the pandemic had been even nastier and deadlier. A pandemic is not a “black swan” but a known risk of potentially catastrophic proportions.

Indeed, Bill Gates warned everyone in a TED talk back in 2015 that we were underprepared for such an eventuality and that it was a much greater threat than many others we waste our precious resources on. Furthermore, many governments have established pandemic plans to protect their population, which they presumably didn’t follow very closely.

Farewell, free markets

Having been slow to respond effectively initially, the risk now posed by government interference and massive over-reach in markets and our lives is real and going to be with us for some time.

Governments cannot bail out everyone for long, and most, if not all, are not in a good position to do so. Unfortunately, one clear learning from history is that central planning is never likely to be successful long term – a truly market-based economy creates greater prosperity for society in the long term than a centrally planned distribution and commandeering of resources ever will.

Without genuine productivity growth, which we, unfortunately, haven’t had much of for a long time, an economy will not create real wealth in the long term. The distortions created over recent years by manipulating interest rates and inflating bubbles in markets, and now by massive monetisation efforts, will not be resolved by the coronavirus crisis.

Nor will ever-increasing misallocation of resources and zombification of economies. Instead, we have governments focussed on broadening their interference, and doing so to a much greater degree.

This probably simply guarantees even slower real growth on the other side of this crisis, which bodes poorly for equities and property generally over the long term as well as the prospects of widespread wealth creation.

Private markets and cycles including recessions and economic cleansings serve a necessary purpose if allowed to do so, however politically unpopular and inconvenient they may be.

Many more risks lie in wait

There will likely be many worrying changes and outcomes which result from this crisis, some of which I laid out in this wire, 8 more icebergs right up ahead.

Pandemics of the past have shown that real growth is slower after a pandemic, again meaning economic damage and recessionary like conditions could be with us for a lot longer than many care to accept or imagine.

- Consumers will be much less confident and precautionary saving will become more popular, if not mainstream.

- More socialist and/or nationalist and populist leaders may eventuate.

- As discussed, and importantly, geopolitical conflict will continue and military conflict will become a greater possibility.

- De-globalisation is likely at least in part (possibly removing much of the economic benefits from globalisation and growing trade).

- Governments will fail, social unrest may rise and nations will need to become more self-sufficient as they learn the hard way that their cheap but necessary supplies from elsewhere are not as reliable as needed.

- Taxes may rise. Wages and subsidies may increase at the expense of capital.

- While we are experiencing strongly deflationary forces for now, stagflation (low growth and higher inflation) may become a more likely outcome over time.

- Fiat currency debasement is likely to be accentuated, and may prove potentially catastrophic to many countries.

Of course, most of this bodes very poorly for traditional portfolios which are dominated by long-only equity and property risks (such as your average super fund). We expect these to continue to perform very poorly over time and in the ways that count.

Which asset classes work in this environment?

Investors will learn that there is no easy way to wealth creation and that not everyone gets a prize.

Unlike the consensus based on extrapolating a bubble economy and fake growth forever, we view traditional equity, property and related assets as more suitable for opportunistic and/or speculative investments at the current time, rather than long-term strategic buy and hold investments.

Meanwhile, cash and bond yields are now almost nothing and negative in real terms, meaning long term allocations to traditionally defensive assets probably simply now guarantee slow wealth destruction.

Precious metals are likely to become more widely accepted as necessary parts of a portfolio. The need for active value-added investment and skilled, differentiated and diversified portfolio management capable of preserving and growing capital in an adverse economic environment will only grow with time.

Don't expect a quick fix

Somewhat amazingly, even the global pandemic is still being underestimated by investors, despite it dominating the news and our lives. The consensus appears to be expecting this to be a short-term issue that will quickly be resolved once the “curve is flattened”.

Many expect that we can all get back to work soon and carry on with our lives once we’ve done our “deep freeze” or hibernating “interval time-out”. In contrast, our analysis suggests that there may not be any easy or quick fix to the coronavirus crisis, although we hope there is.

A game-changing treatment from an existing drug is unlikely, although a drug or two is probably helpful and an improvement on the current standard treatment. Furthermore, an effective vaccine and the time required to scale up its manufacturing is likely to be at least 15-18 months or more away, which is an eternity in today’s world.

This article, When, and How, Does the Coronavirus Pandemic End? provides some more context on what the 'exit strategy' from this could look like.

In the interim, given the economic challenges from social distancing, the risks to investors are very great. Importantly, the investment risks are much more substantive than simply being about the coronavirus (although that would be challenging enough), as we have highlighted above.

Buckle in for the long-haul

The lack of a definitive medical solution means that governments may be relying upon draconian solutions – or modifications thereof - for much longer than we would like and can tolerate for keeping the killer virus at bay.

Better testing and social adaptations will likely be introduced, but public and social adaptations of some sort may be required for over a year if we aren’t going to allow the virus to wash through communities and wipe out more of our vulnerable and elderly rapidly, and a few of our healthy people also.

While the deaths from letting the virus run rampant might seem unacceptable for now, without much hope of a quick and effective preventative or cure, within weeks and months many governments – and particularly but not exclusively those in the developing world - will struggle to maintain cooperation with social distancing policies.

This is because the costs of a prolonged economic shutdown - including massive unemployment and underemployment - will only grow with time and eventually become unbearable.

Trust will be lost, people will struggle and it will become less clear whether the virus is the greater threat - or the societal and government reactions to it with their resulting destruction of wealth and opportunity.

The audible hiss of a deflating bubble

Hence, there is every reason to be concerned about the outlook for our economies, societies and investment markets. Even though many humans are ingenious and adaptable, we did not generally come into this situation as a society from a position of strength.

We have been living in a bubble economy for a long time, with inflated asset prices driven by unsustainable growth in credit and debt. The markets naturally want to deflate, while our governments are doing everything they can to keep the bubbles from doing so and prevent any cleansing process from occurring, given how painful it would be - for them in particular.

Of course, this is an unhealthy situation. Will central banks and treasuries be able to create one more bubble cycle driven by massive expansions in deficits and government and other debts? I suspect this will be very difficult this time given the ongoing challenges we are likely to face, but if so, it will only come at a further very real cost to our ongoing prosperity and that of future generations and will hence likely be short-lived.

Many investment markets have been or are in the process of being socialised at taxpayer expense given the extent of government involvement. Many others have become highly speculative. This is truly a time when investors need to be very adaptive to the risks, possibilities and opportunities. There are no guarantees of success.

Furthermore, there is no point simply watching the destruction of our societal wealth and a better future forgone. We all need to influence and be involved in the coming changes and outcomes so that they provide a much more constructive, productive, inclusive and sustainable outcome for all of us than would be the case otherwise.

Taking an interest in our local community and in political decisions, taking less for granted, and using our voice to educate and advocate for positive changes to the status quo is one way to do this.

Dynamic markets need dynamic strategies

Meanwhile, investors needs have not changed much but are poorly served by most investment choices. Investors hence need to navigate and avoid being dependent on the binary and likely poor outcomes of the economy and many investment markets at the current time.

Despite the massive and unprecedented speed of falls and wealth destruction in nearly all asset markets during the quarter, the Lucerne Alternative Investments Fund (LAIF) ended the dramatic and destructive quarter flat, and without any meaningful drawdowns at any stage.

We recently shared our thoughts on how investors can position for this kind of market environment, among other things, in a special Q&A we did with Livewire, which you can read here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Dr Jerome Lander is a highly experienced, proven Portfolio Manager and a specialist in outcome-based and absolute return investing, which is a client centric approach aligned with many peoples' preferences - and one which is well suited to today's more challenging investment environment. Jerome has achieved net returns for clients of around 20% in both the challenging 2020 year and in 2021, with much lower drawdowns and volatility than Australian equities and hence much superior risk adjusted returns. His Wealthlander Diversified Alternative fund targets double digit returns annually for wholesale clients, with lower volatility and greater consistency than Australian equities, using a diversified multi-asset portfolio approach.

........

Important Notice

Jerome Lander is Managing Director of boutique investment firm Procapital. He is the portfolio manager of the Lucerne Alternative Investments Fund with Lucerne Partners and outcome based managed account portfolios with Dynamic Asset, and a well-known thought leader and client advocate within the investment industry. He helps ensure researched, differentiated and tailored outcome based investment portfolios are available to financial advisers and their clients which have demonstrated outstanding risk adjusted returns. This communication is for informational purposes only, and is a thought piece which represents the views of the author alone. It is not intended as an offer for the purchase or sale of any financial instrument. It does not constitute personal or financial advice of any kind and should not be relied upon as such - investors should consult their financial advisers before making any investment decision. This article's accuracy cannot be assured. All opinions and views expressed constitute judgment as of the date of writing and may change at any time without notice and without obligation.

2 topics

Dr Jerome Lander is a highly experienced, proven Portfolio Manager and a specialist in outcome-based and absolute return investing, which is a client centric approach aligned with many peoples' preferences - and one which is well suited to today's...

Expertise

Dr Jerome Lander is a highly experienced, proven Portfolio Manager and a specialist in outcome-based and absolute return investing, which is a client centric approach aligned with many peoples' preferences - and one which is well suited to today's...

Expertise

Comments

Comments

Sign In or Join Free to comment