Three reasons why low inflation is good for shares and property

Share markets are at or around record levels despite lots of worries, particularly around the coronavirus (Covid-19) outbreak. A common concern is that this is because central banks (like the Fed and the RBA) are distorting market forces and just want higher asset prices. And flowing from this its argued that prices for assets like shares and property are overvalued, record highs are artificial, and a crash is inevitable. Markets are at risk of a short-term correction given the large gains since the last greater than 5% correction into August and given the risks around Covid-19. But beyond this it’s a lot more complicated than the bears would have it.

Central banks really just responding to market forces...

There is some truth to the claim that central banks want higher asset prices. Higher asset prices are part of the transmission mechanism for monetary easing to the economy because they boost wealth and this helps boost spending. As former Fed Chair Alan Greenspan said in 2010 “a stock market rally may be the best economic stimulus”. But it’s not quite that simple:

- First, central banks also fret about that financial instability that flows from higher asset prices as they may lead to overvalued markets that could crash or encourage people to take on too much risk say via excessive debt. Recall Alan Greenspan’s concerns about “irrational exuberance” and don’t forget the credit tightening that occurred from 2017 in Australia that was designed to slow “risky” housing lending.

- Second, more fundamentally central banks are really just responding to market forces. In the post GFC world we have seen lower inflation in response to ongoing spare capacity and competition from online disruptors, offshoring and automation. More fundamentally, reflecting greater caution we have seen desired saving exceed desired investment globally. All of which has driven lower interest rates which central banks have just responded too. To have not cut official interest rates would have defied market forces and caused even weaker growth, higher unemployment and even lower inflation.

- Finally, it's rational for asset prices to move up in response to lower inflation and lower interest rates.

…lower inflation equals higher PEs (and lower yields)

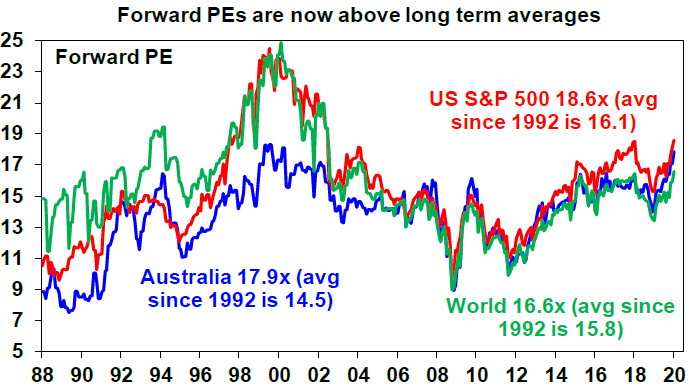

The next chart shows the ratio of share prices to consensus expectations for earnings over the next 12 months, which is often referred to as forward PEs. As can be seen, these are now above their long-term averages in the US and Australia, although US and global PEs are still well below tech boom extremes.

Source: Thomson Reuters, AMP Capital

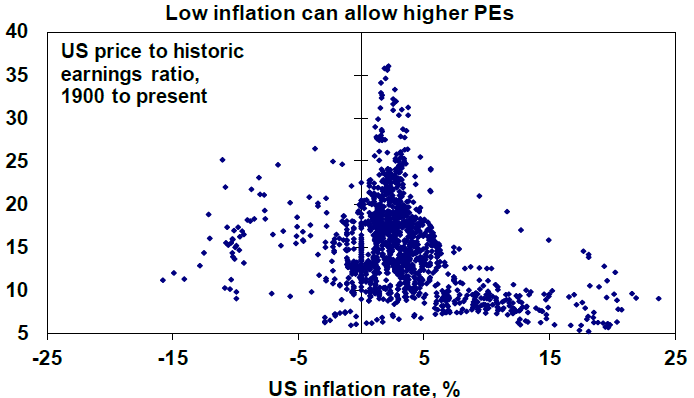

However, the next chart shows the long-term relationship between inflation on the horizontal axis and the price to earnings ratio on the vertical axis. The PE tends to move higher as inflation falls, although its less clear once inflation falls into deflation. And right now we have very low inflation of just below 2% globally.

Source: Bloomberg, AMP Capital

A rise in PEs in response to low inflation, providing it’s not deflation, makes sense for three reasons:

- First, low inflation means lower interest rates which boosts the value of future profits and dividends making shares more attractive. Or put simply lower inflation and interest rates boosts the attractiveness of higher yielding assets so investors switch into those higher yielding assets which pushes up their price relative to their earnings, dividends or rents.

- Second, low inflation means reduced economic volatility and uncertainty and hence investors are prepared to price shares on higher price to earnings multiples. The next chart shows rolling 10-year volatility in annual GDP growth for the US and Australia. It’s been in a downtrend since the first half of last century with the drivers being the growing importance of the more stable services sector, declining inventory levels which reduced the manufacturing inventory cycle and macro policies aimed at stabilising economic growth. But the shift to lower inflation from the 1980s and 1990s has likely also contributed.

Source: Bloomberg, AMP Capital

- Finally, low inflation means improved quality of earnings as firms tend to understate depreciation when inflation is high and so overstate actual earnings. So again, investors are prepared to pay more for shares when inflation is low.

The equity risk premium remains okay

So, while share markets may be around record levels and price to earnings multiples are relatively high there is some rationale for this given that it’s a low inflation and low interest rate world. And the longer inflation remains down its conceivable that the higher PEs may go. How high is impossible to know for sure. But as a result, it makes sense to look at share market valuations that allow this.

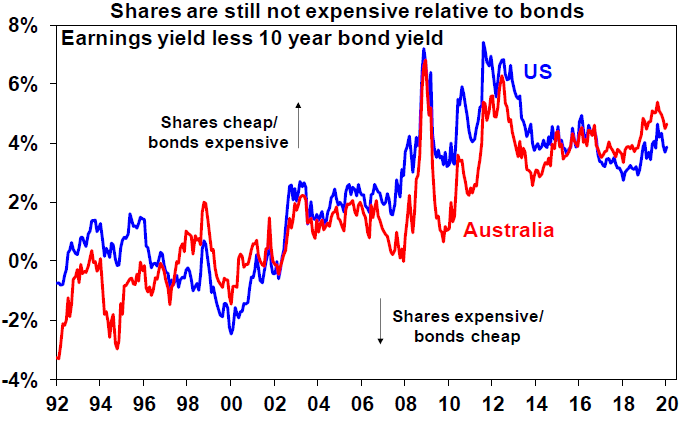

The next chart subtracts the 10-year bond yield for the US and Australia from their earnings yields (using forward earnings). This basically gives a sort of proxy for the equity risk premium – the higher the better. While this gap is well down from its post GFC highs, it’s still reasonable, suggesting shares are still more attractive than bonds. Of course, this will change if bond yields rise, but as we have seen in recent years this is taking a long while to eventuate with various events including trade wars and the coronavirus outbreak conspiring to keep yields low.

Source: Thomson Reuters, AMP Capital

What about property?

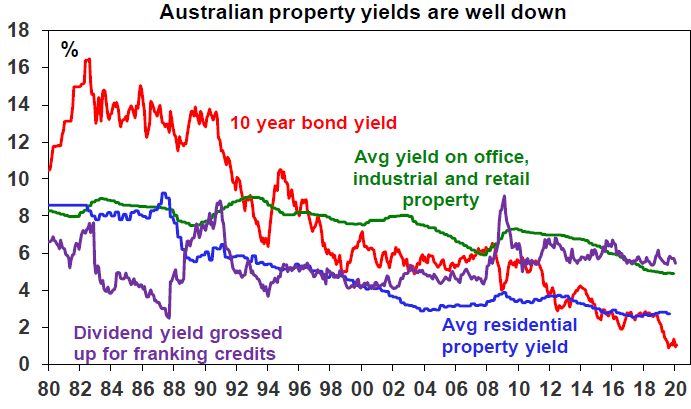

Basically, the same applies in relation to property and other assets in that lower inflation drives higher valuations for them too. This is evident in lower rental yields (or capitalisation rates) as lower inflation and interest rates pushes up the price relative to rents that investors are prepared to buy property at. This has certainly happened in Australian property markets with rental yields falling sharply since the 1980s and 1990s. This is particularly the case for residential property to the point that it is overvalued on some measures, with a shortage of dwellings relative to underlying demand enabling this to be perpetuated (but that’s a whole other issue beyond the scope of this note!). If the rental yield is inverted and expressed as a PE it would have risen to around 20 times for high quality commercial property but to a whopping 50 times for residential property, compared to around 12 times for both in the early 1980s and compared to around 18 times for shares. This would suggest residential property remains relatively expensive!

Source: REIA, JLL, Bloomberg, AMP Capital

So, what’s the catch?

There are two catches.

First, valuations are no guide to timing markets and none of this precludes a correction in shares, particularly given the risks around coronavirus as noted earlier.

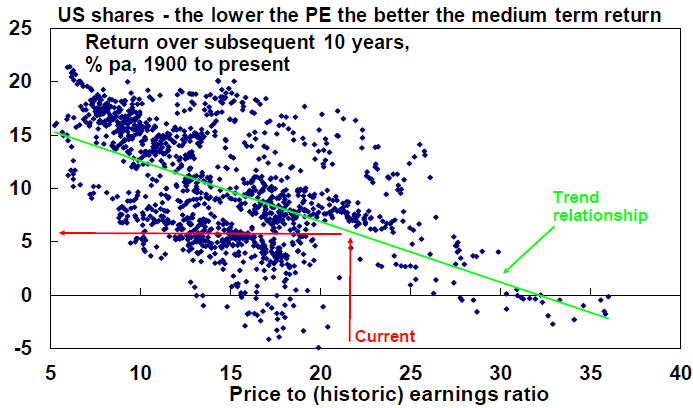

Second, just as low interest rates and low bond yields mean low prospective returns from cash and bonds, high PEs - or their inverse of lower earnings yields - and lower rental yields for property point to more constrained returns from shares and property on a medium-term basis. The following chart shows a scatter plot of the PE ratio for US shares since 1900 (horizontal axis) against subsequent 10-year total returns (ie dividends and capital growth) from shares. It indicates a negative relationship, ie when share prices are relatively high compared to earnings subsequent returns tend to be relatively low.

Source: Bloomberg, AMP Capital

The same inverse relationship exists for Australian shares.

Concluding comment

The bottom line is that while shares may be vulnerable to a correction, the rally in markets does not seem excessive given the low inflation and low interest rate environment. Key to watch for would be a recession, which would depress earnings and risk tolerance, or a sharp acceleration in inflation, which would drive sharply higher interest rates and a revaluation downwards in prices for shares and other assets. But beyond the risks to economic activity posed by the coronavirus outbreak both seem unlikely at present.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

4 topics

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Expertise

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets