Two big issues for markets

When COVID-19 (coronavirus) first made headlines, in China, then worldwide, global market reactions were complacent. It was perceived as a primarily Chinese issue, reminiscent of the SARS outbreak of the early 2000s. Expectations were for a brief selloff, which would last only until the number of new cases retreated.

However, the virus has spread far beyond Chinese borders and erupted into a global pandemic. Global economic expectations changed dramatically in early March, and have continued to evolve just about daily since. Global growth forecasts for this year are likely to reach 40-year lows.

It’s uncertain what lies ahead, but COVID-19 is sure to dominate headlines in the near term, and it presents two big issues for markets.

The first is on the demand side. As a result of the sudden decline in economic activity, many companies will experience unprecedented declines in revenue. It is unlikely that many companies will be able to adjust cost bases quickly enough to this decline, so we are likely to see increased pressure on balance sheets and cashflows. This is likely to be an acute problem for small- and medium-sized businesses. These enterprises tend to have less-diverse revenue streams, are more consumption driven, and have less access to financing.

The second issue markets are facing is liquidity. These concerns manifest in two ways: market liquidity and company liquidity. The former is an issue because as markets fall, financial conditions tighten. This, in turn, drives markets even lower. The latter is problematic because as companies’ cash flows fall, the probability of credit defaults increase, which could threaten the economy at large. If companies go bankrupt, there will be labor shedding and people leaving the workforce, which would be a greater structural threat to the economy than just the current demand for liquidity.

These issues play out in an environment where oil markets are reeling after having received a dual shock. There has been a decline in demand due to the rapid slowdown in economic activity. There has also been a supply-side shock, driven by a price war between Saudi Arabia and Russia. Lower oil prices help consumers, but disrupt the supply chain and investment, which will have economic consequences that could be compounded by the coronavirus situation.

Government action will serve as the nuts and bolts for building a barricade against these more serious structural issues.

Thus far, central banks have responded by lowering rates and pumping liquidity into markets. Whilst this is an important step, we are still awaiting more fiscal-policy action, which may inspire enough confidence to stabilize markets. However, a lasting recovery will also depend on confidence that the rate of spread of the virus has been contained.

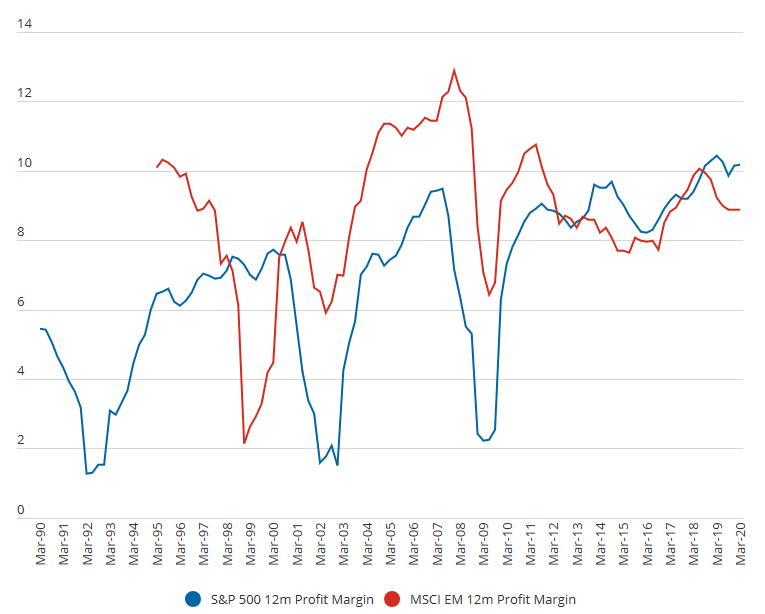

We may not be able to divine the full future economic effects of COVID-19, but we can look to history as a guide. In China, as a result of containment measures against the virus, industrial production experienced its steepest decline ever (even compared to the global financial crisis). This suggests that economic data around the world will continue to be grim – for now, at least. If we look further back, however, it’s clear that profit down cycles tend to be short and sharp vs. up cycles, in both EMs and the U.S (Chart 1).

Chart 1: Historic profit down cycles are shorter than upcycles

Source: Bloomberg March 2020. S&P 500 Unmanaged Index considered representative of the U.S. stock market. MSCI Emerging Markets Index is an unmanaged index considered representative of stocks of developing countries. The index is computed using the net return, which withholds applicable taxes for non‐resident investors.

The more governments are able to prevent demand-side problems and liquidity concerns from evolving into structural issues, the better the chance for a strong earnings recovery. All of this also hinges on how quickly coronavirus cases peak. Right now, it’s unclear as to whether the pandemic will continue in waves over a prolonged time, or be stemmed by summer 2020. In Hubei, the Chinese province where the virus originated, cases peaked in early March, about 6 weeks after the initial surge. While this may offer some guidance, the Chinese government has farther-reaching powers than many other states, which enabled them to quickly enact extremely strict containment measures. We expect that other nations will require longer lockdown periods because they cannot be as stringent. Because recovery depends on containment, we believe economies will experience a U-shaped recovery once measures are relaxed.

In emerging markets, the call for liquidity is being answered, which is promising. Additionally, emerging market balance sheets entered this crisis period in a healthy state, which may bode well for recovery. Reform agendas, especially in Brazil, also offer encouragement.

While this market rout appears, in many ways, similar to 2008, volatility may present an opportunity for long-term investors to initiate positions in high-quality companies with good valuations that can benefit from these market conditions.

Never miss an insight

Keep up to date with Aberdeen Standards latest thinking by hitting the follow button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

abrdn manages assets for a range of global and domestic clients. We invest worldwide and follow a predominantly long-only approach, based on fundamentally sound investments.

3 topics

abrdn

abrdn manages assets for a range of global and domestic clients. We invest worldwide and follow a predominantly long-only approach, based on fundamentally sound investments.

abrdn

abrdn manages assets for a range of global and domestic clients. We invest worldwide and follow a predominantly long-only approach, based on fundamentally sound investments.

Comments

Comments

Sign In or Join Free to comment