TOL - 25th Mar, 2025

US equities sell-off will create opportunities

Tariffs, funding freezes, and government spending cuts have caused investors to reassess the outlook. The chances of stagflation have grown, but policy will stabilise, and opportunities will appear, both domestically and globally.

US equities slide

Since the S&P 500 posted an all-time high on the 19 February, it has declined by over 10 per cent, marking a technical correction. The widely watched 200-day moving average has also been breached. US equities that had climbed strongly following the presidential election of Donald Trump have swiftly reversed course as investors re-evaluate US policy.

Part of the reversal in US equities seems to be a case of complacency. The market initially focused on the positives of the Trump platform and preferred not to dwell on the potential downsides. Investors hoped that Trump would take a pragmatic approach and use the threat of tariffs as a negotiating tactic without following through.

By mid-February, it emerged that no immediate agreement with Mexico and Canada was likely, further steel and aluminium tariffs would be implemented, and trade partners India and Europe could be added to the list of tariff counterparties. In March, some of the tariffs on Mexico and Canada came into effect, with the majority postponed until April, while the blanket tariff on China was doubled to 20 per cent. All three countries have promised retaliatory measures. In addition, the Trump administration is considering protectionist policies on copper, lumber, and timber.

These developments indicate the US is taking a hawkish stance towards its trade deficit with other countries. The implications of these measures are higher input costs and lower margins for US businesses and higher prices for consumers. Trump and Treasury Secretary Bessent have also both indicated they are willing to accept temporary financial market pain to push through their agenda.

Challenges to growth

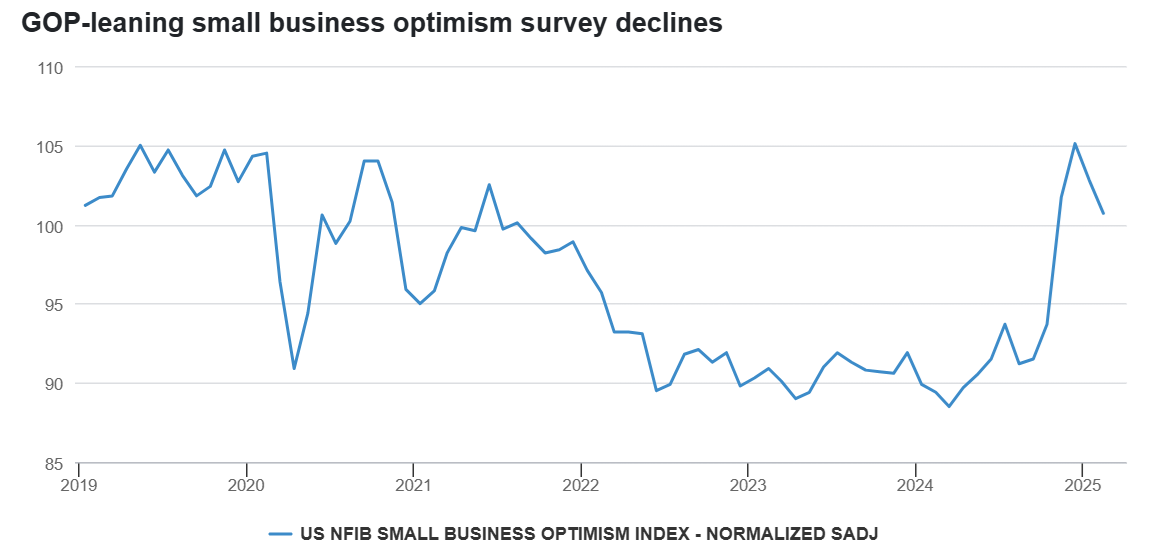

The uncertain policy environment has made it more difficult for businesses and consumers to plan investment and spending. While these challenges are not yet showing up clearly in hard economic data - US GDP growth is tracking above 2 per cent and unemployment remains at historically low levels - it is affecting soft data. Recent consumer confidence readings have dipped sharply and even the Republican-leaning NFIB small business survey, which tends to be more optimistic during Grand Old Party (GOP)-led governments, has weakened.

The market also continues to re-evaluate the potential implications of Trump’s other policies. Immigration controls have been interpreted as likely to lead to a lower influx of cheap labour and consequently higher wages. Department of Government Efficiency (DOGE)-related spending cuts have seen tens of thousands of government employees laid off and that number could ultimately stretch to hundreds of thousands, affecting the spending power of many households, at least in the short term. The combination of tariffs, immigration control, and government job cuts are leading to lower growth forecasts.

Despite that outlook, monetary policy levers may not be able to flex as much as usual. Inflation remains above target, and the US administration’s policies are expected to put upward pressure on prices. If this is the case, it means that despite weaker growth, the US Federal Reserve may be forced to keep monetary policy more restrictive than they would ordinarily like. Our macro team has placed a 50 per cent probability on a stagflation scenario (higher than target inflation with below trend growth) for the US this year.

Short-term pain, but potential long-term gain

The more pessimistic outlook is feeding through to financial markets. US Treasury yields are falling - not because inflation is coming under control, but because of growth fears. In equities, US stocks have sold off as investors incorporate the revised economic path and the AI theme loses some of its lustre. Previously, artificial intelligence (AI) was powering US equities higher, but this impetus has evaporated in recent weeks as the advent of Chinese rival DeepSeek’s R1 model causes a rethinking of the prospects for the Magnificent Seven stocks.

Although technical signals in US equities suggest stocks are oversold and that we could see some short term rebound given the magnitude and speed of the recent declines, the fundamental outlook is uncertain as the lack of policy clarity will affect the environment for corporate decision making.

However, we know the Trump administration has an end game - a better trade balance with its partners and onshoring manufacturing operations. In that light, once the policy backdrop becomes more stable, we could see a continuation or even acceleration of large scale and prolonged capital investment that reorients the economy towards a stronger domestic manufacturing base. As the environment settles, we could also see renewed focus on tax cuts and deregulation.

Outside of the US, we see opportunities in other markets. Europe, which is starting from a point of low expectations, has posted solid corporate results; the region’s earnings revisions have risen quickly, decoupling from the flatter US earnings trajectory. The valuation gap between the US and Europe has reduced as European markets benefit from a re-allocation from the US, although the gap remains wide historically. Europe is the strongest regional performer this year and this may continue.

Our latest Analyst Survey of our bottom-up equity analysts around the world shows corporate sentiment improving markedly in Europe while slowing in the US. Ukraine peace talks are already leading to a drop in European gas prices, reducing the price of a key input for businesses. In Germany, the recent election results could signify a watershed moment; a relaxation of the debt brake and potentially hundreds of billions of euros in infrastructure and defence spending over the coming years.

Similarly to Europe, our equity analysts highlight China for improving corporate sentiment. DeepSeek has accelerated the AI race in China and, combined with signs of a more supportive policy environment for technology and potential fiscal stimulus, could sow the seeds of an enduring bull market.

Investors should bear in mind that the S&P 500 is back to where it was six months ago, and valuations, which were stretched, are moderating. While we expect more volatility ahead, there are opportunities. A US economy transitioning to more domestically driven manufacturing and trading at more reasonable valuations could offer a rich pool of investment ideas for stock pickers. In the meantime, there are opportunities for investors at a global level. Europe and China both have the potential for ongoing market recoveries, while Japan remains an attractive investment destination as it continues to enjoy reflation and structural reform.

For further insights from the team at Fidelity International, please visit our website.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Niamh is Co-Chief Investment Officer (Co-CIO), Equities at Fidelity International. She was previously Managing Director of Equity Research and Co-Head of Equity Sustainable Investing at Fidelity Investments (FMR). Prior to joining FMR in 2011, she held various roles as an equity analyst and sector portfolio manager at Pioneer Investments, Merrion Stockbrokers and Tilman Asset Management.

........

All information is current as at its published date unless otherwise stated. Not for use by or distribution to retail investors. Only available to a person who is a "wholesale client" under section 761G of the Corporations Act 2001 (Commonwealth of Australia) ("Corporations Act“).

This document is issued by FIL Responsible Entity (Australia) Limited ABN 33 148 059 009, AFSL No. 409340 (‘Fidelity Australia’). Fidelity Australia is a member of the FIL Limited group of companies commonly known as Fidelity International. Prior to making any investment decision, investors should consider seeking independent legal, taxation, financial or other relevant professional advice. This document is intended as general information only and has been prepared without taking into account any person’s objectives, financial situation or needs. You should also consider the relevant Product Disclosure Statements (‘PDS’) for any Fidelity Australia product mentioned in this document before making any decision about whether to acquire the product. The PDS can be obtained by contacting Fidelity Australia on 1800 044 922 or by downloading it from our website at www.fidelity.com.au. The relevant Target Market Determination (TMD) is available via www.fidelity.com.au. This document may include general commentary on market activity, sector trends or other broad-based economic or political conditions that should not be taken as investment advice. Information stated about specific securities may change. Any reference to specific securities should not be taken as a recommendation to buy, sell or hold these securities. You should consider these matters and seeking professional advice before acting on any information. Any forward-looking statements, opinions, projections and estimates in this document may be based on market conditions, beliefs, expectations, assumptions, interpretations, circumstances and contingencies which can change without notice, and may not be correct. Any forward-looking statements are provided as a general guide only and there can be no assurance that actual results or outcomes will not be unfavourable, worse than or materially different to those indicated by these forward-looking statements. Any graphs, examples or case studies included are for illustrative purposes only and may be specific to the context and circumstances and based on specific factual and other assumptions. They are not and do not represent forecasts or guides regarding future returns or any other future matters and are not intended to be considered in a broader context. While the information contained in this document has been prepared with reasonable care, to the maximum extent permitted by law, no responsibility or liability is accepted for any errors or omissions or misstatements however caused. Past performance information provided in this document is not a reliable indicator of future performance. The document may not be reproduced, transmitted or otherwise made available without the prior written permission of Fidelity Australia. The issuer of Fidelity’s managed investment schemes is Fidelity Australia.

© 2025 FIL Responsible Entity (Australia) Limited. Fidelity, Fidelity International and the Fidelity International logo and F symbol are trademarks of FIL Limited.

Niamh is Co-Chief Investment Officer (Co-CIO), Equities at Fidelity International. She was previously Managing Director of Equity Research and Co-Head of Equity Sustainable Investing at Fidelity Investments (FMR). Prior to joining FMR in 2011, she...

Niamh is Co-Chief Investment Officer (Co-CIO), Equities at Fidelity International. She was previously Managing Director of Equity Research and Co-Head of Equity Sustainable Investing at Fidelity Investments (FMR). Prior to joining FMR in 2011, she...

Comments

Comments

Sign In or Join Free to comment