Value vs. growth

The debate over whether a value or a growth style produces better long term investment returns continues, with staunch advocates on both sides. Certain high profile investors such as Warren Buffett continue to champion the Benjamin Graham school of value investing while, in contrast, recent BAML fund managers’ surveys have shown the higher P/E ratio FANG stocks to be one of the most favoured trades.

Below we analyse what could be driving performance divergence. In particular, was Jeremy Grantham right when he said that the value style has a hard time ahead? Or is growth’s recent outperformance about to fade?

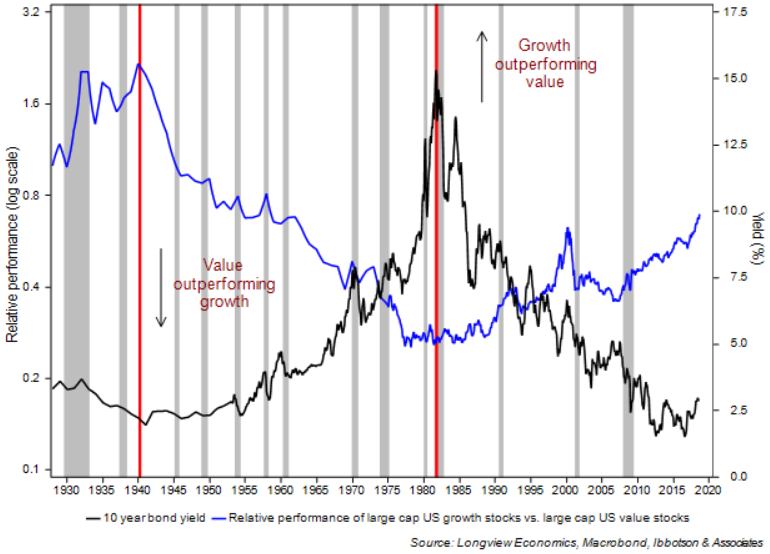

Throughout most of the 20th century, value stocks outperformed growth stocks. The total return on a buy-and-hold investment in 1927 in large cap value stocks would be superior to an investment in large cap growth. Taking the whole period together, though, is somewhat misleading, as value returns have not always dominated. Between 1927 and 1940, and from the early 1980s up to the present day (except for during the last economic cycle) growth shares tended to outperform value.

Fig 1: Relative performance of large cap US growth vs. value* stocks shown against US 10 year bond yields

*NB our data merges indices from Ibbotson & Associates and MSCI

Interestingly, during both periods of secular outperformance by growth stocks, the economic environment was one of falling long term interest rates (fig 1). That is, there were secular bull markets in bonds (and interest rates) up to the early 1940s and since the early 1980s. The Russian economist, Kondratieff, identified long cycles in interest rates, postulating that a full cycle – i.e. a rise and a fall in interest rates – typically lasts 56-60 years.

This rate cycle has been ongoing now for 69 years. Unless, as we outlined, it ended in July 2016.

Whilst clearly this number of data points/turning points is insufficient to draw any robust conclusions (statistically), theoretically it makes sense that growth outperforms in a period of falling interest rates. Growth stocks tend to be valued using long term discount factors. Falling bond yields should therefore support an upward re-rating of the valuations of growth stocks. Conversely rising bond yields should undermine those valuations. Equally rising bond yields are also often/typically accompanied by rising inflation. Value stocks are usually dividend plays with those value companies often themselves endogenous in the inflation process (e.g. utility companies, food producers, staples) and, as such, able to protect earnings growth and dividends in a rising bond yield environment (and therefore outperform).

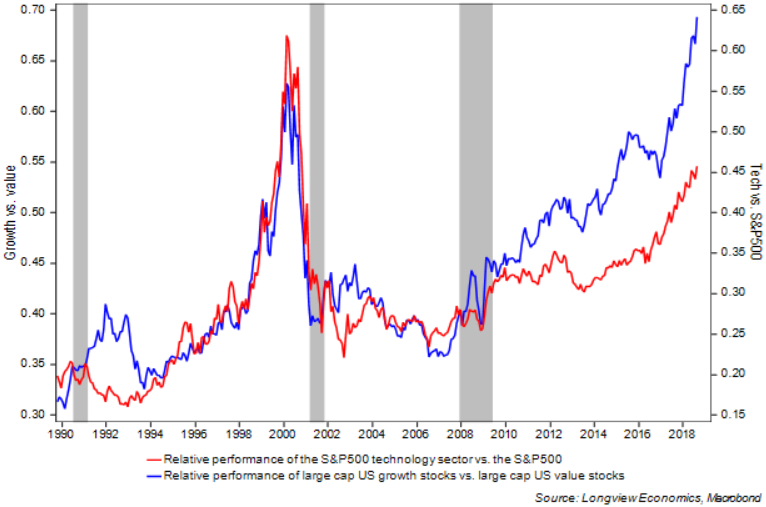

Fig 2: Relative performance of large cap US growth stocks vs. large cap US value stocks shown with the relative performance of S&P500 technology vs. the index.

Also of note in this debate is the dominance of the technology sector in recent years (i.e. in driving growth). Since the late 1980s, when our sector data began, the relative performance of growth vs. value has largely tracked the relative performance of the S&P500 technology sector vs. the broader S&P500 index (fig 2). In that period of time the weight of the technology sector within the broader market has grown from ~7% to ~25%.

As such, going forward the relative performance of value and growth is likely to continue to be dominated (in the near term) by the performance of US technology as well as by the medium term outlook for the US 10 year bond yield. As it stands, we view bonds as attractive at current levels (i.e. yields should fall in the near term). In the longer term (perhaps after the next cyclical bear market and at the start of the next bull), we would anticipate renewed weakening of bond prices (i.e. yields to move higher) and a continuation of the secular bond bear market which we anticipate likely began in the middle of 2016.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation advice; and Global thematic, macro and commodities research.

4 topics

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation...

Expertise

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

What a 40% year taught us: 4 lessons from the past 12 months (and 3 new stocks to buy)

Seneca Financial Solutions

Equities

2 stocks to drive future performance following a 35% return in six months

Katana Asset Management