Why are you accepting more risk for less return?

This is a question that’s currently very relevant for corporate bond investors, particularly in the ‘safe’ investment grade (IG) sector. Since the 2008 financial crisis, corporate bond markets have been in a real sweet spot. On one side they’ve seen huge capital inflows from yield chasing investors and on the other side, corporates were happy to take full advantage by issuing lots and lots of bonds.

In fact, over the past 10 years corporates have raised more debt at cheaper levels in bond markets than at any other time in modern history.

Heading into the 2008 financial crisis, a lot of the debt build-up was in the household sector (think subprime mortgages) and it was banks who took the hit on their balance sheets. This time around the debt build-up is in the corporate sector.

Corporate debt levels have never been higher (c. 38% of global GDP) and most of this growth has been in corporate bonds (c. 57% of global corporate debt), many of which sit in funds and ETF’s sold to retail investors.

It was a perfect match. Yield chasing investors met debt hungry corporates and both sides were happy. That was then. The current state of affairs is very different. Corporate bond markets are now at that point where investors face a lot more risk, for a lot less return.

The expression “picking up pennies in front of a steam roller” conveys the idea of chasing small gains in spite of disproportionately large risks. This perfectly characterizes the current situation in corporate bond markets, particularly the IG sector where yields are vanishingly low.

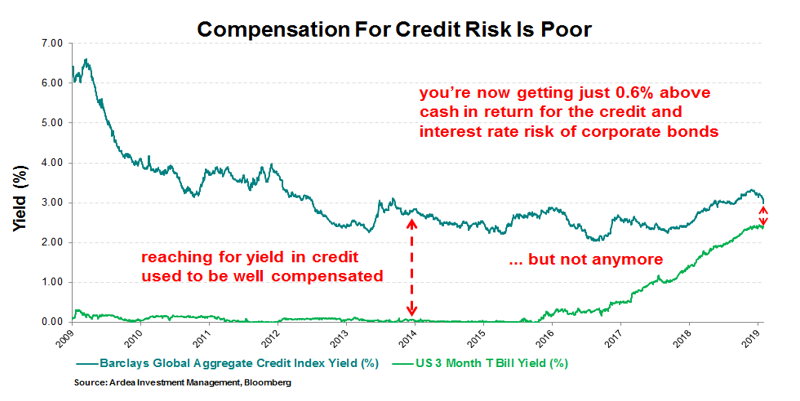

Corporate bonds, or any investment for that matter, are not inherently good or bad. Rather it’s about the balance between risk and return. We’re now at a point in the cycle where the risk vs. return trade-off in IG corporate bonds is asymmetrically poor. The chart below captures this.

The chart compares the yield on a broad USD corporate bond index (Barclays Global Aggregate Credit Index) to what you get from risk-free cash (USD 3 Month Treasury Bill yield). This chart covers the USD markets specifically but the same dynamics have played out globally.

The yield pick-up (i.e. extra yield) has declined to just 0.6% – that’s all you get in return for taking materially more credit risk, in addition to significant interest rate risk (remember, corporate bonds carry both risks). Reaching for yield in corporate bonds used to be well compensated. Those easy money days are now gone.

While the yield pick-up has dropped to historically low levels, late cycle risks in corporate bonds are also rising. Credit quality has worsened, credit spread and interest rate volatility is rising and liquidity has become structurally compromised.

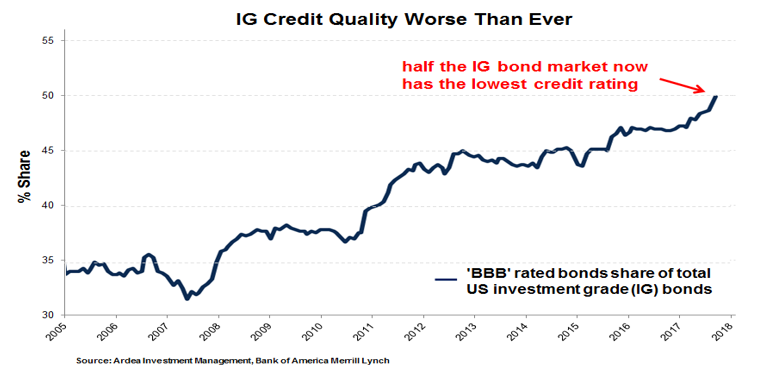

The IG segment of the corporate bond market is perceived as being ‘safe’, in the sense that credit quality is high. However, even in this space credit quality has been worsening.

The chart below shows the worsening credit quality of IG corporate bonds. The proportion of bonds rated ‘BBB’ – the lowest investment grade rating – has never been higher.

A particular concern is ‘fallen angel’ risk.

In the context of credit markets, a fallen angel refers to a company whose bonds start with a high quality investment grade credit rating but then transitions to a sub-investment grade rating (known as high yield or ‘junk’ rated bonds).

Often this happens because the company has taken on too much debt but can also occur due to worsening economic conditions or changes in certain industries. With half the market now sitting at the cusp of a junk rating, fallen angel risk is rising.

This can become very disruptive because many of the largest credit funds and ETF’s can only hold IG bonds. So, as bonds drop to a junk rating they become forced sellers. If enough angels fall, a disorderly market sell-off results.

Years of zero interest rates created an immense yield chasing party across global credit markets following the 2008 financial crisis.

The signs of excess and under-pricing of credit risk have now become extreme.

For example, a BBB rated French company (Veolia Environment) was able to issue a 3 year bond at a negative yield. So, a company rated just above junk was being paid by investors to borrow money from them!

Stretching the party analogy, this is the kind of behaviour you might see towards the end of a big night out. Seems like a good idea at the time but the next morning … not so much. (refer – A big night out for credit markets)

Maybe this growing list of risks doesn’t turn out as bad as feared … that’s possible … but going back to the core principle of risk vs. return, at this point in the cycle and with yield pick-ups so, you’re just not getting paid enough to stick around and find out whether the downside scenario plays out. (refer – Early movers are leaving the credit party)

We got a small taste of that downside scenario in the fourth quarter of last year when credit markets got hit hard as equities fell.

Corporate bonds, particularly the IG segment, are widely perceived as being defensive investments … but the reality has changed.

In 2018, as equities experienced large drawdowns, segments of the IG market had their worst year since the 2008 GFC. That’s not how a defensive investment should behave. 2018 was just a small taste. With the yield cushion in bonds now so low, expect corporate bond returns to become more correlated to equities going forward.

In the context of the role IG corporate bonds play in a broader investment they currently offer the worst of both worlds. On one hand they don’t provide decent returns in the positive market scenarios and on the other, they fail to act as a defensive buffer against equity losses in the negative ones.

This is not a blunt proposition of whether corporate bonds are good or bad but rather the more subtle question of compensation for risk and whether other fixed income return sources offer a better risk vs. return trade-off (refer Market inefficiency is a growing opportunity in fixed income, There’s more to fixed income than just buying bonds)

Reaching for yield in corporate bond markets worked well in the past. It has a time and place … but now is not that time and the defensive part of your portfolio is not the place to be doing it.

Never miss an update

Stay up to date with the latest news from Ardea Investment Management by hitting the 'follow' button below and you'll be notified every time I post a wire.

Want to learn more about Ardea's expertise? Hit the 'contact' button to get in touch with us or visit our website for further infomation.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Gopi Karunakaran is Ardea’s Co-Chief Investment Officer (Co-CIO), together with Ben Alexander. In this capacity they both share responsibility for overseeing the investment process and investment team, with ultimate accountability for ensuring the performance of all portfolios is consistent with client objectives.

Gopi has +20 years’ experience across global fixed income markets, including the full spectrum of global interest rate and credit markets, as well as broader macro relative value investing across equities, FX and structured products.

1 topic

1 contributor mentioned

Gopi Karunakaran is Ardea’s Co-Chief Investment Officer (Co-CIO), together with Ben Alexander. In this capacity they both share responsibility for overseeing the investment process and investment team, with ultimate accountability for ensuring the...

Expertise

Gopi Karunakaran is Ardea’s Co-Chief Investment Officer (Co-CIO), together with Ben Alexander. In this capacity they both share responsibility for overseeing the investment process and investment team, with ultimate accountability for ensuring the...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets