Why we own shares in Alliance Aviation

When it comes to investing, we’re not big fans of airlines. But in the case of Alliance Aviation Services (ASX: AQZ), we’re happy to make an exception. You see, Alliance operates fly-in fly-out charter services for Australian mining companies, and its flights are in demand. With high returning business and strong cash generation, we think there’s a lot to like.

The Montgomery Small Companies Fund looks to invest in stocks with competitive advantage, run by talented management with their hands deftly gripped to value creation levers in their control. The airline sector with its high capital intensity, inflexible and high fixed cost and exposure to major imponderable externalities such as fuel costs (oil prices) and unknown demand is not the normal place to go shopping for stocks that meet that criteria set! These are not the best of times for the aviation sector but that’s when Alliance’s value creation opportunity resonates.

Management are proven value creators

In our view Alliance is an example of the value that quality management can bring in small caps. They listed on 20 December 2011 with an IPO price of $1.60, delivering a total return including dividends of 149.1 per cent since then, that’s an annual compound rate of return of 11.2 per cent, smashing the rate of return for the Small Ords Accumulation Index at 5.4 per cent over the same period.

The management team has built a resilient winning business model, executing a nimble strategy to take advantage of opportunities that arrive from the cyclicality of the aviation sector. Let’s run through AQZ’s equity story and the opportunities ahead.

Key Competitive Advantage 1: Low unit capital cost assets are in AQZ’s DNA

In a capital-intensive sector, if you have spent a lot less acquiring your asset base than your competitors did, then you are off to a good start. Lower dollars invested allows you to make an acceptable return at profitability levels that your competitors cannot.

A quick history: October 2004 Alabama USA, Alliance’s management team visit the headquarters of the US State’s public pension fund – Retirement Systems of Alabama – which had recently become inadvertent owners of surplus aircraft in the then post 9/11 world.Alliance management were there to find good assets at distressed prices and they acquired six aircraft (Fokker F100’s) that day, the first of many low-cost asset purchases taking advantage of the opportunities that availed during aviation sector downturns.

In 2015, at the depths of the Australian resource sector cycle, Alliance’s management bought 21 Fokker aircraft (15 F100’s and 6 F70’s) for just USD$15 million (yep, fifteen) from Austrian Airlines. Alliance had to be creative to make that deal work – issuing AQZ shares directly to Austrian’s parent company (Lufthansa), as well as making cash payments on staged aircraft delivery. Management found a way to get the deal funded and the job done, knowing that the planes were too valuable in AQZ’s business model to pass up. Ditto Switzerland 2019, another five F100’s at good prices.

Key Competitive Advantage 2: Lower risk and flexible low-cost structure and high service level

AQZ aren’t like Qantas (QAN), they don’t take fuel price or load factor risk, and they don’t run a beefy cost structure of a national flag carrier. During its almost 9-year listed life Alliance has seen oil prices range between $25 and $125, and never once has it discussed fuel costs as a profit driver. Alliance’s clients are resource companies in Australia, that need solutions to move their largely production workforces large distances, by air, to and from mine sites. Alliance provides aircraft, crew and a service level guarantee for a fee. The clients enjoy the flexibility of controlling flight schedule timing and pay for the aircraft, irrespective of how full it is, and pay for the fuel cost on top.

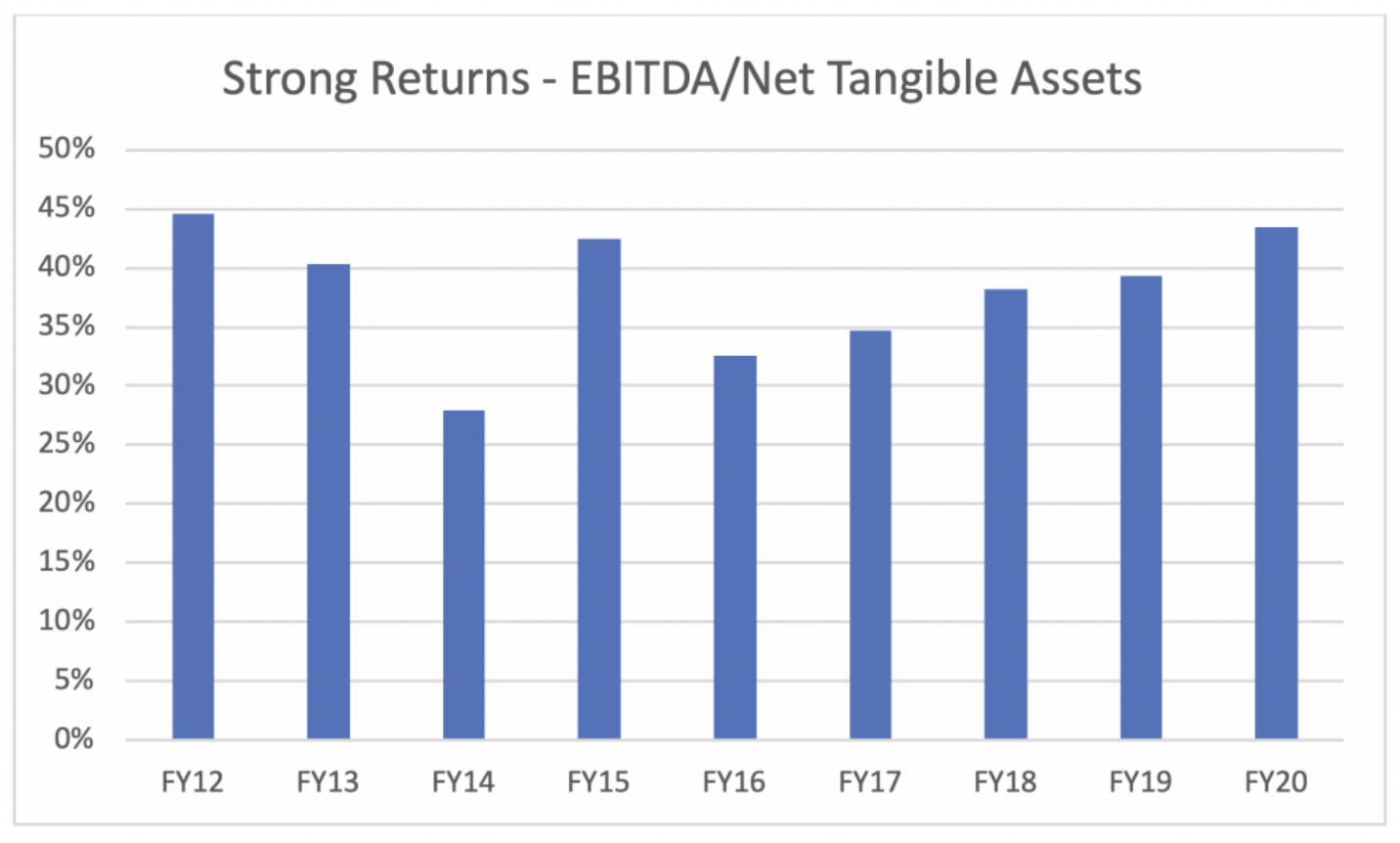

Alliance varies the quantity of fleet in service based on the demand profile it needs to service. Critically by owning its aircraft it doesn’t make lease payments for assets it needs to take out of service, by outsourcing its heavy maintenance requirements its fleet runs based on the needs of the business and not the need to keep a fixed cost labour base occupied. It’s set up to handle the variability of its FIFO resource sector client demand, and as can be seen in the chart belowAlliance makes good returns on its assets even at the bottom of the cycle – more on AQZ’s returns later.

Alliance focuses on service quality, reliability and low-cost operations. The track record is one of high asset availability, best in class on-time performance and industry leading cost structure. This is important to resource sector customers, who want a service that’s good enough but with a low cost and service reliability levels that translates to better staff productivity as they transit mine site to home location. Low and flexible costs with high service reliability is a competitive advantage.

AQZ is a high returning business with strong cash generation

Operating low unit capital cost aircraft, with high cost structure flexibility, means the company has consistently made good returns, as illustrated in the chart below, even in the depth of the Australian resource sector downturn of 2013 to 2015. Those rates of return are great, and the level and consistency that other airlines can only dream of. Which probably goes some way to explaining why QAN took an unsolicited 20 per cent stake in Alliance in February 2019. They are now invested alongside management and former founders who speak for greater than 10 per cent of the share register; this management has skin in the game.

Source: AQZ financials, Montgomery

And those returns have been backed up by cashflow, over the same period post tax operating cashflow conversion from EBITDA has been 75 per cent which is very strong, even adjusting for low tax payments since 2016 cash conversion has been pretty good. And we expect strong free cashflow to continue.

Just as Alliance used times of market distress to acquire low unit cost aircraft, they have done the same thing with aircraft parts. Those parts significantly lower the future cash maintenance capex cost of maintaining it’s aircraft fleet. To put this into some context. At FY11 AQZ had 25 aircraft and a parts inventory on the balance sheet of $6 million; at FY20 AQZ held $57 million of inventory for 43 aircraft – 9x the inventory levels for under double the fleet size. Out of a $34.5 million maintenance capex cost last year, $8.4 million, or a quarter of the cost, came from existing inventory. Put another way they have prepaid a significant cash cost of the business, and we will see that come through as stronger cashflow in the years ahead. Alliance has a balance sheet that has been invested in.

Never let a good crisis go to waste: fleet expansion

Today the aviation sector globally has been broken by COVID-19, domestically putting Virgin in administration and forcing QAN into an emergency capital raise. But it has created the conditions where AQZ’s competitive advantage thrives and Alliance is expanding into the COVID-19 opportunity void. Management raised A$96 million of capital for growth, and yep you guessed it, they invested that in buying 14 Embraer 190e aircraft at distressed prices, with parts and engines and an option to buy 5 more for A$112 million. Never let a good crisis go to waste. Rinse and repeat.

What is AQZ’s earnings capacity?

Alliance’s Fokker fleet has steadily expanded from 2 in 2002, to 21 in 2010 and 43 aircraft today, with the 14 Embraers to arrive in F21. Over AQZ’s listed life (10 years FY11 to FY20) our model calculates that Alliance earned around an average of $1.9 million of EBITDA per aircraft in service per annum. We expect the new Embraer aircraft to earn at least the same EBITDA as the Fokker planes, possibly more, as these newer generation assets are a little larger and more operating cost efficient. Doing the maths suggests on average the Fokker fleet of 43 plus the 14 new Embraers have $110 million or so EBITDA capacity per annum.

On top of that Alliance has a business that provides aviation services including trading aircraft and parts; it’s very lumpy, but hasn’t done less than $10 million of revenue a year, and we think is very profit dense, probably good for another $5 million of EBITDA per annum. Call it $115 million EBITDA capacity.

To put this into some content at $3.50 the company has an enterprise value of $645 million; that’s a multiple of 5.6x at average EBITDA capacity.

Opportunities – The COVID-19 void

Today AQZ’s Fokker fleet is working hard keeping up with resource sector demand in a COVID world and judging by second half’s record profits (2H20 $46.5 million clean EBITDA – annualised $93 million from 42 in service aircraft) is doing rather well. Management have called out that they expect demand from their resource client base to continue to be strong and are bringing the last of their Fokker asset base into service to meet demand. Alliance has taken share when competitors have been hurting.

Up until its administration event, Virgin was one of AQZ’s major customers, Alliance provided aircraft on a wet lease basis (aircraft and crew), Virgin were taking advantage of Alliance’s low cost structure to operate routes where it struggled with its cost structure and aircraft type to make money. It appears Alliance could make money where Virgin could not. Today that revenue has gone to zero. But what about Virgin 2.0. At some point we are all going to be flying around Australia domestically again.

Virgin 2.0 is mooted to be a leaner more focused operator, one with fewer staff, costs and aircraft and even less resources of the type that Alliance offers. In our view there is likely a larger role in Virgin 2.0 for Alliance ahead than before. Perhaps that’s where those newly acquired Embraers will operate. However, if Virgin 2.0 doesn’t make it, there will be a (very) large void in the Australian aviation landscape, particularly on regional routes where Alliance’s cost structure and asset base are well suited.

Either way we think Alliance’s competitive advantage means it will profitably grow and generate strong cashflows (and fully franked dividends) into the post-COVID-19 opportunity that exists in the Australian aviation market.

Get investment insights from industry leaders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Gary is the Portfolio Manager of the Montgomery Small Companies Fund – a small-cap Australian equity fund investing in 30 to 50 high quality, undervalued small and emerging companies with strong growth potential. The fund invests outside the ASX100.

1 topic

2 stocks mentioned

Gary is the Portfolio Manager of the Montgomery Small Companies Fund – a small-cap Australian equity fund investing in 30 to 50 high quality, undervalued small and emerging companies with strong growth potential. The fund invests outside the ASX100.

Expertise

Gary is the Portfolio Manager of the Montgomery Small Companies Fund – a small-cap Australian equity fund investing in 30 to 50 high quality, undervalued small and emerging companies with strong growth potential. The fund invests outside the ASX100.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX playmakers making things happen

Livewire Markets

Equities

Brokers' top picks for October

Livewire Markets