Winning by not losing

Human emotions and biases affect all investors. Left unchecked, these emotions can sabotage financial decisions and generate suboptimal investment outcomes. But understanding how human emotions and behaviour influence decision-making can unlock investment opportunities. The key to unlocking these opportunities is:

- understanding how financial markets interact with human behaviour; and

- finding an investment style to exploit these biases.

Emotions are the enemy for investors

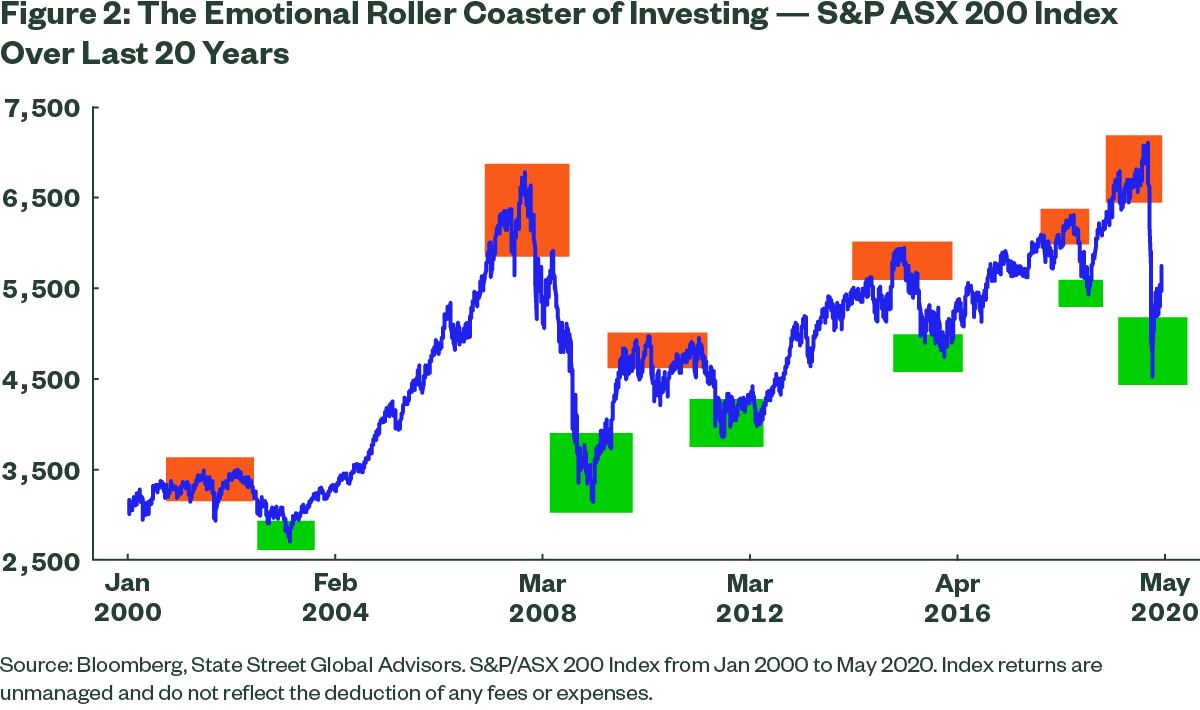

Financial markets have the ability to generate and destroy wealth. They are complex and volatile and evoke significant emotions. Figure 1 depicts an all too common emotional roller coaster for investors. The worst-case scenario is letting your emotions drive your investment decisions - buying a security near the high or capitulating and selling near the low. How can investors avoid the mistakes of mass psychology and turn emotional short comings into opportunity? Be risk averse when the market is overly optimistic (Euphoria) and seek risk when the market is overly pessimistic (Panic and Capitulation).

Over the last 20 years, there are many examples of Euphoria followed by Fear and Capitulation (see Figure 2).

2020 has seen it all yet again - Euphoria in January followed soon after by Fear, Panic and Capitulation in March; and followed by Hope and Relief and elements of Euphoria again in April, May and June. We can look at a number of market indicators to help us find opportunities within financial markets.

What occurs at the market index level also occurs with single securities. As active managers, we see securities being mispriced every single day. The margins are often small - but can at times be large. Mispricing is usually a result of human emotions and bias, including fear, greed, herd mentality, over-emphasising recent events and confirmation bias.

We regularly see investors being overly optimistic about the fortunes of a company and factor in too much good news. Equally, we observe investors become overly pessimistic on a company’s fortunes, giving up on the business model.

The ability to recognise these opportunities requires an unemotional, fact-based assessment of the company’s prospects. How can we build an unemotional assessment of a company’s prospects?

Facts are your friend

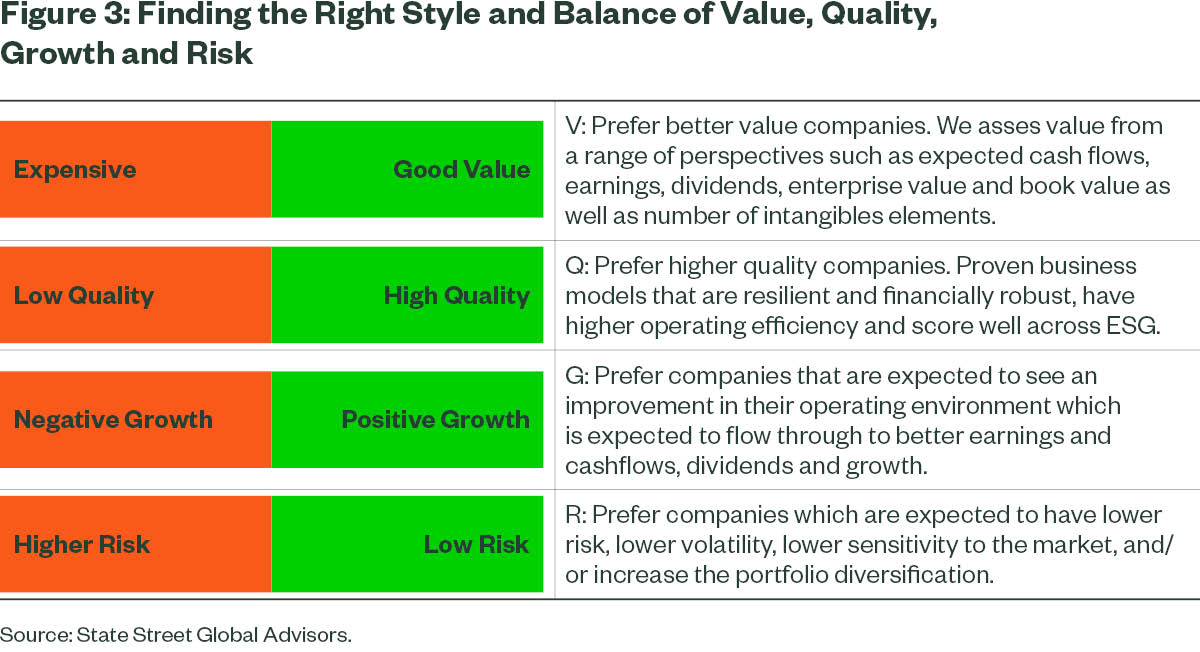

When it comes to making good investments, emotional decisions are your enemy - facts are your friend. The State Street Active Equities team has developed a process to unemotionally evaluate the prospects of securities in order to determine when human emotional biases have resulted in security mispricing. We clinically evaluate each company from a perspective of Quality, Relative Value, Growth Outlook and Risk to assess its opportunity set.

‘When it comes to making good investments, emotional decisions are your enemy - facts are your friend.’

Our predetermined analysis framework assesses the facts with little bias. It is not influenced by popular media, or the latest group think, and is designed to remain unemotional. We focus on buying quality businesses at reasonable value, with improving growth prospects and advantageous risk characteristics. When evaluating stocks, the key is being able to unemotionally assess all these elements. As you would expect, we have our largest positions in companies that rank the highest across all of these metrics. Our position size will vary based on how these attributes change over time.

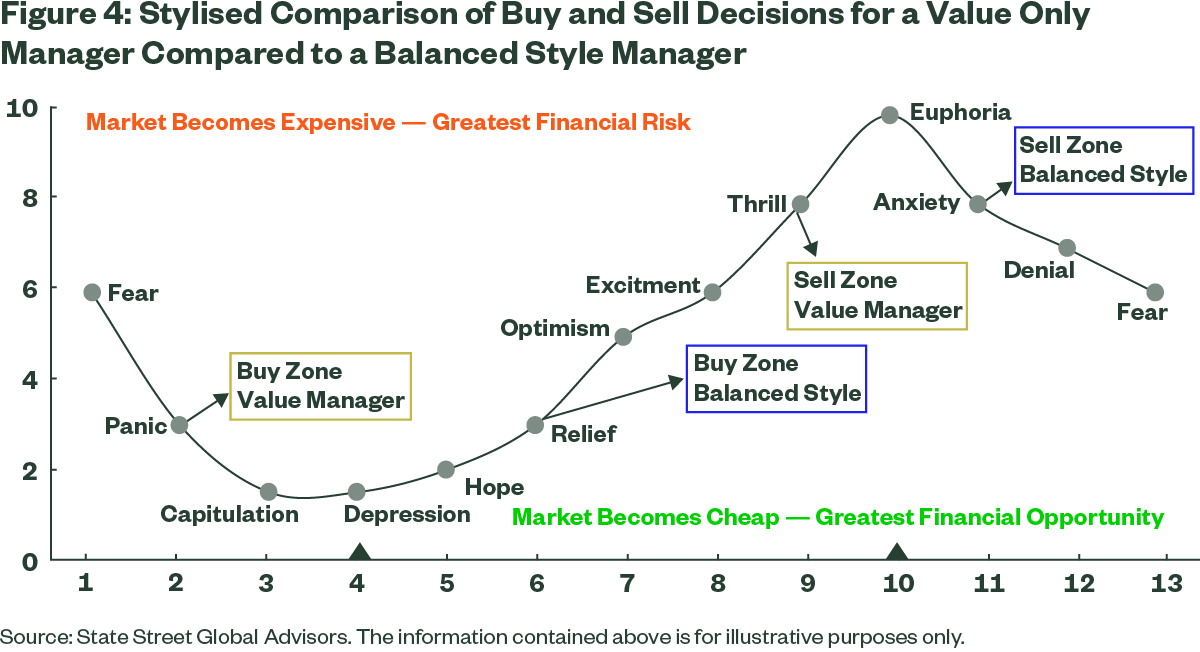

Figure 4 describes a stylised buy and sell zone (see blue box) for our balanced style investment process (incorporating a balance of value, quality, growth and risk considerations in the investment process). It then compares this to a value-only Manager (see orange/yellow box). Both styles can generate excess return, but tend to buy and sell at different points across a company’s rerating cycle. For companies that offer attractive quality and risk characteristics, we look for those offering a balanced combination of value and improving growth prospects. It is not enough for a stock to become cheap; we would also need to see the operating environment improving (or at the very least stop deteriorating).

Focusing on this value-growth combination, as well as the company’s quality and risk profile, helps to avoid value traps.

It is important to note that we can also hold companies that have become more expensive, if the operating environment is sufficiently positive and the quality and risk elements are also supportive enough to justify the higher valuations. But once a company has become expensive it is more likely we will exit the position as soon the positive outlook deteriorates.

The big four banks: quality and value but growth outlook challenged

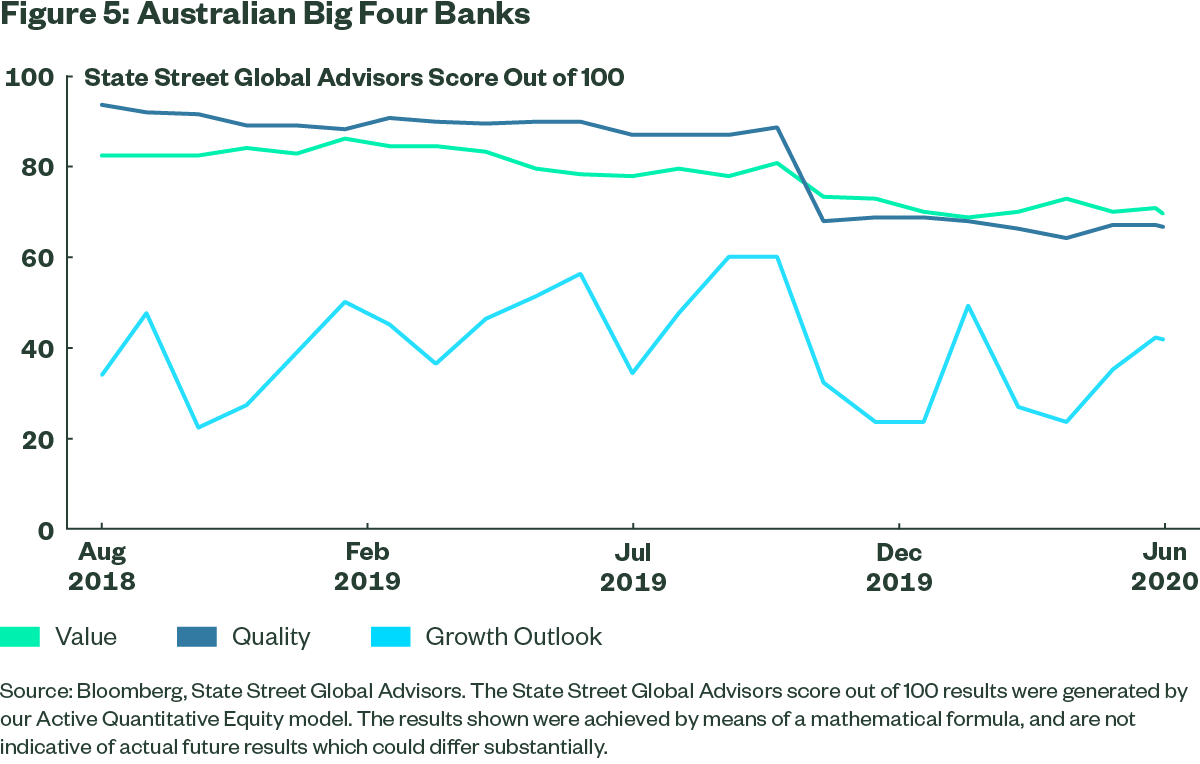

Our balanced style approach has not owned any banking companies in the last 12 months and has been structurally underweight compared to the index for many years. This position has been beneficial to investors as the big four banks have materially underperformed the broader market over the last 2 years.

Our view on the banks can be decomposed into our balanced investment style that assesses the opportunity set for the banks with respect to the quality of the business, the valuation opportunity as well as the growth potential. Figure 5 provides a time series view on the big four banks on average and is broken down by the key elements we use to assess all companies.

All scores are out of 100 and we prefer companies with higher scores across quality, value and growth outlook. Currently, the banks do not present a strong enough investment case and this has been the situation in the last 2 years. As shown in Figure 5, they have consistently scored well in terms of quality and value but this is not enough for our balanced investment approach. At this stage, we continue to see a difficult operating environment for the major big four banks driven by a slowing economy, lower loan growth, a deteriorating bad debt cycle, ultra-low interest rates, as well as further regulation and competition. Our assessment of the operating environment for the big four banks on average has been consistently below 50 and currently sits at 40 out of a possible 100. A value and quality manager might already own the banks but our balanced style needs to see a less negative outlook before we can establish a position.

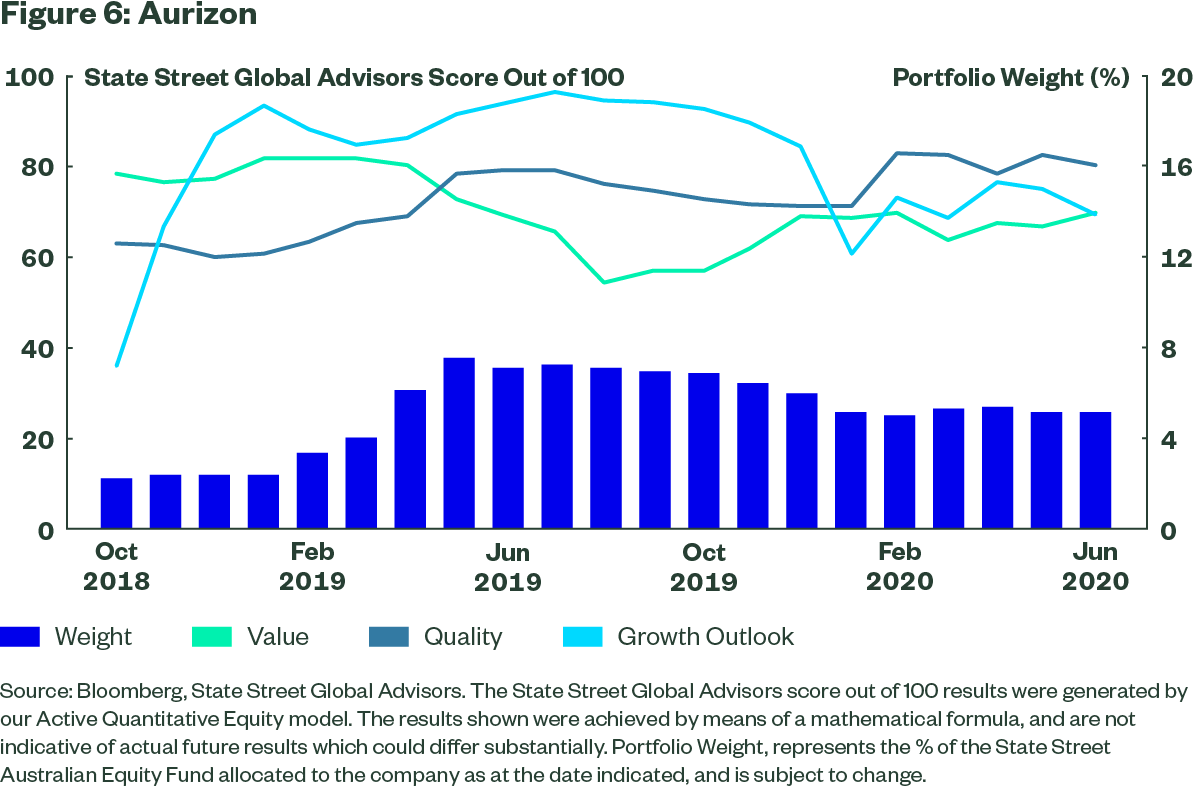

Why Aurizon scores well across quality, growth and value

On the other hand, we have held Australian rail freight operator Aurizon since October 2018. In Figure 6, we show the State Street Australian Equity Fund (“the Fund”) portfolio weight compared to our changing assessment of Aurizon over time.

The company is considered a quality business scoring between 64 to 84 since October 2018. Its share price represented good value back in October 2018 but it wasn’t until the company's growth outlook improved that we added to our position. As the stock has outperformed, its valuation score has come back from 85 to 70, but still offers some valuation support. Quality and growth remain supportive of our current position. Since 28 September 2018, Aurizon has generated a total return of 16.9% p.a. outperforming the S&P/ASX 300 Index*.

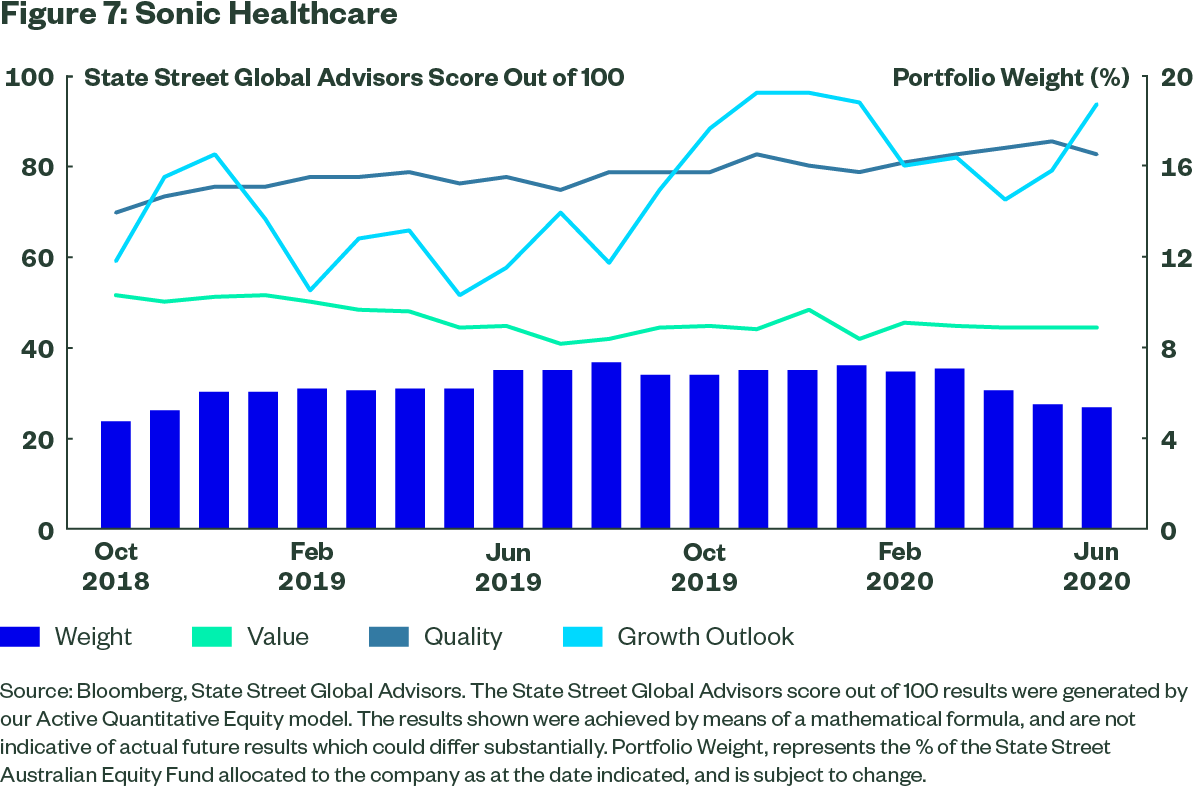

Sonic Healthcare: high quality and growth outlook now looking more expensive

We have been overweight Sonic Healthcare for more than 18 months and it has been a strong contributor to the Funds outperformance. In Figure 7, we decompose our assessment of Sonic Healthcare in terms of the key components of quality, value and growth.

The company scores very highly in terms of quality (from 70 to 87) and also from a volatility or risk perspective. Its growth outlook has also been high (76 to 98 out of a possible 100) since September 2019. Offsetting the strong quality and growth outlook is the valuation support, which has been consistently moving lower as the stock continues to outperform. Should the quality or growth profile deteriorate, we will likely reduce our position in the company.

Sonic Healthcare is a good example of our style which incorporates more than just value and we recognise that value is not the only driver of a stock’s performance. Since 30 September 2018, the company has returned 15.3% p.a. outperforming the S&P/ASX 300 Index*.

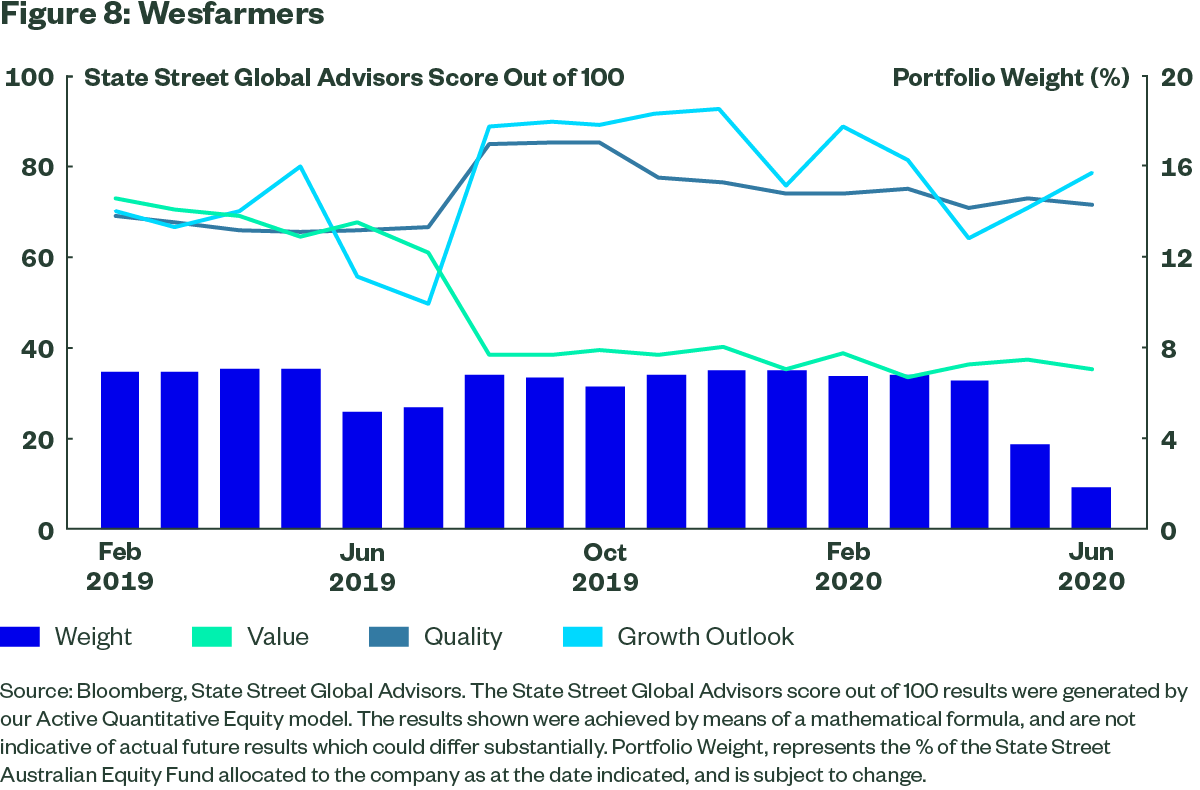

Wesfarmers: high quality and growth outlook now looking more expensive

Wesfarmers has been a core holding for more than 18 months and has contributed to the Funds outperformance. The figure below illustrates our changing assessment of Wesfarmers since February 2019, when all scores were above 70 out of 100. By August the stock had run hard reducing the valuation score to 40 from 74.

Had we been a value only manager we likely would have exited but because the quality and growth outlook components were improving to ~90, offsetting the lack of valuation support, we continued to hold a position.

However, as the valuation has remained ~40 out of a possible 100 and the other components have decreased, we have gradually reduced our fund weighting over time. Since 28 February 2019, Wesfarmers has generated a total return of 30.4% p.a. outperforming the S&P/ASX 300 Index*.

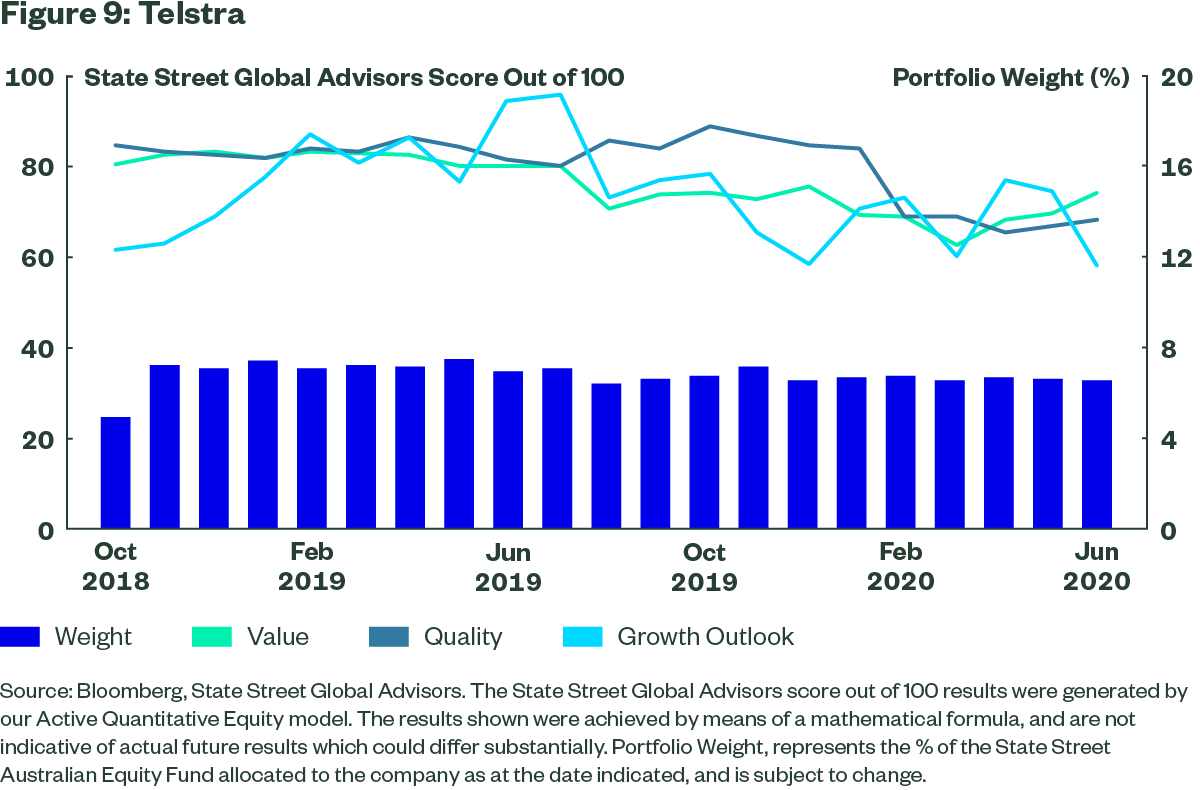

Telstra – value and quality with a more volatile growth outlook

Telstra is the leading provider of bandwidth and mobile data within Australia and ranks above average from a quality perspective. During 2017 and 2018 the operating environment deteriorated significantly for Telstra with competition eroding margins and sales growth. Over this period the stock underperformed significantly, and the growth outlook scores declined.

By the end of 2018, the underperformance and negative sentiment toward Telstra had opened up some medium term value. In September 2018, the company ranked above average in quality and value but below average in terms of growth prospects. At this point we had a ~4% weight in Telstra, and the company was detracting from performance. By January 2019 the growth outlook began to improve and we lifted our position to ~6.5%. Since January 2019 we have held Telstra at close to 6.5% and it has been a mixed contributor to performance. Since September 2018, Telstra has generated a total return of 6.3% p.a. underperforming the S&P/ASX 300 Index*.

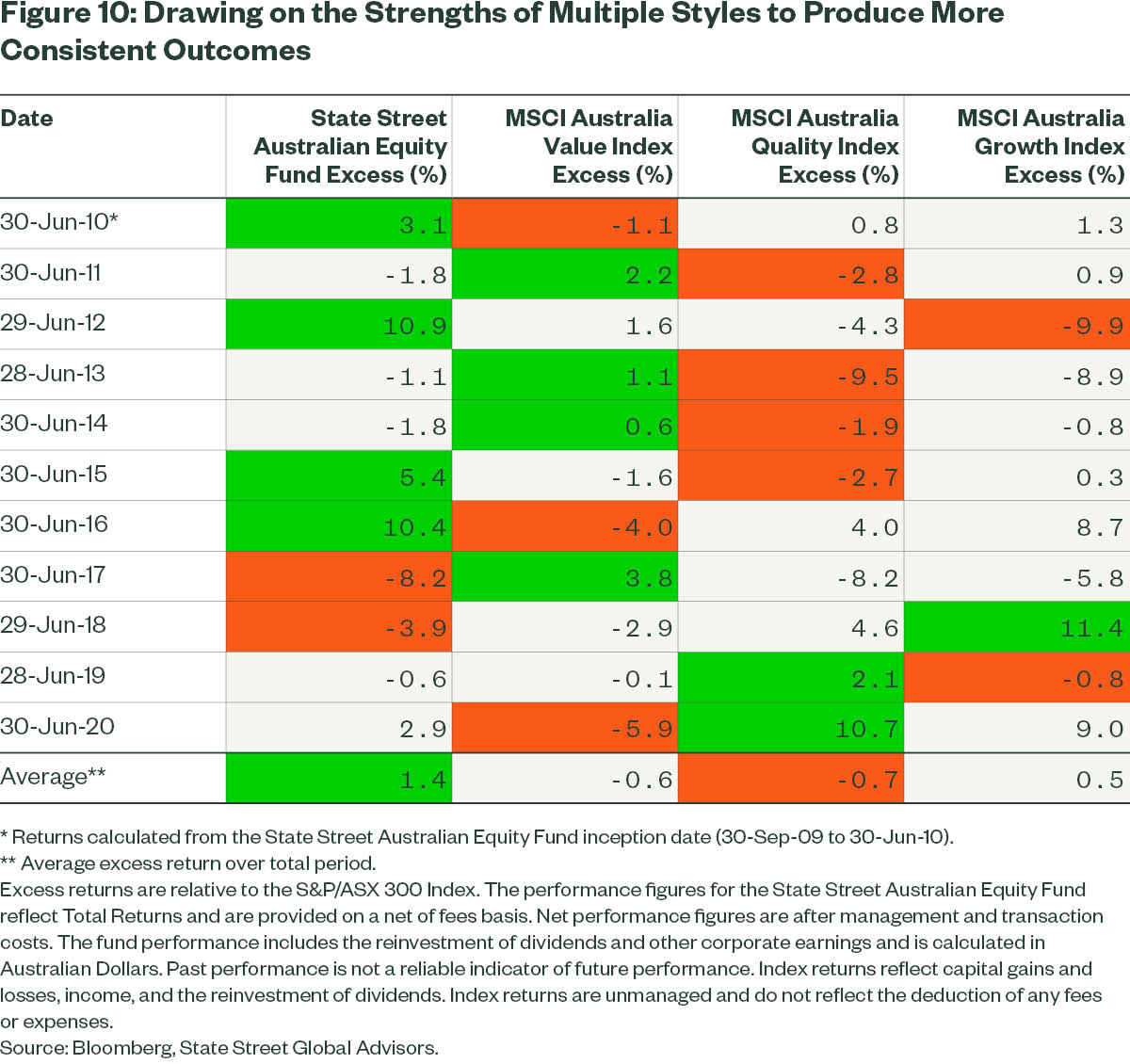

Having a diverse approach to stock selection is designed to be more balanced and produce more consistent outcomes. Figure 10 compares the excess returns (returns generated above or below the returns of the S&P/ASX 300 Index) for a balanced style manager with the MSCI styles of value, quality and growth. In any given year a single style may dominate, but over the time shown, the balanced style approach has demonstrated greater consistency and higher excess returns.

Boring is indeed beautiful

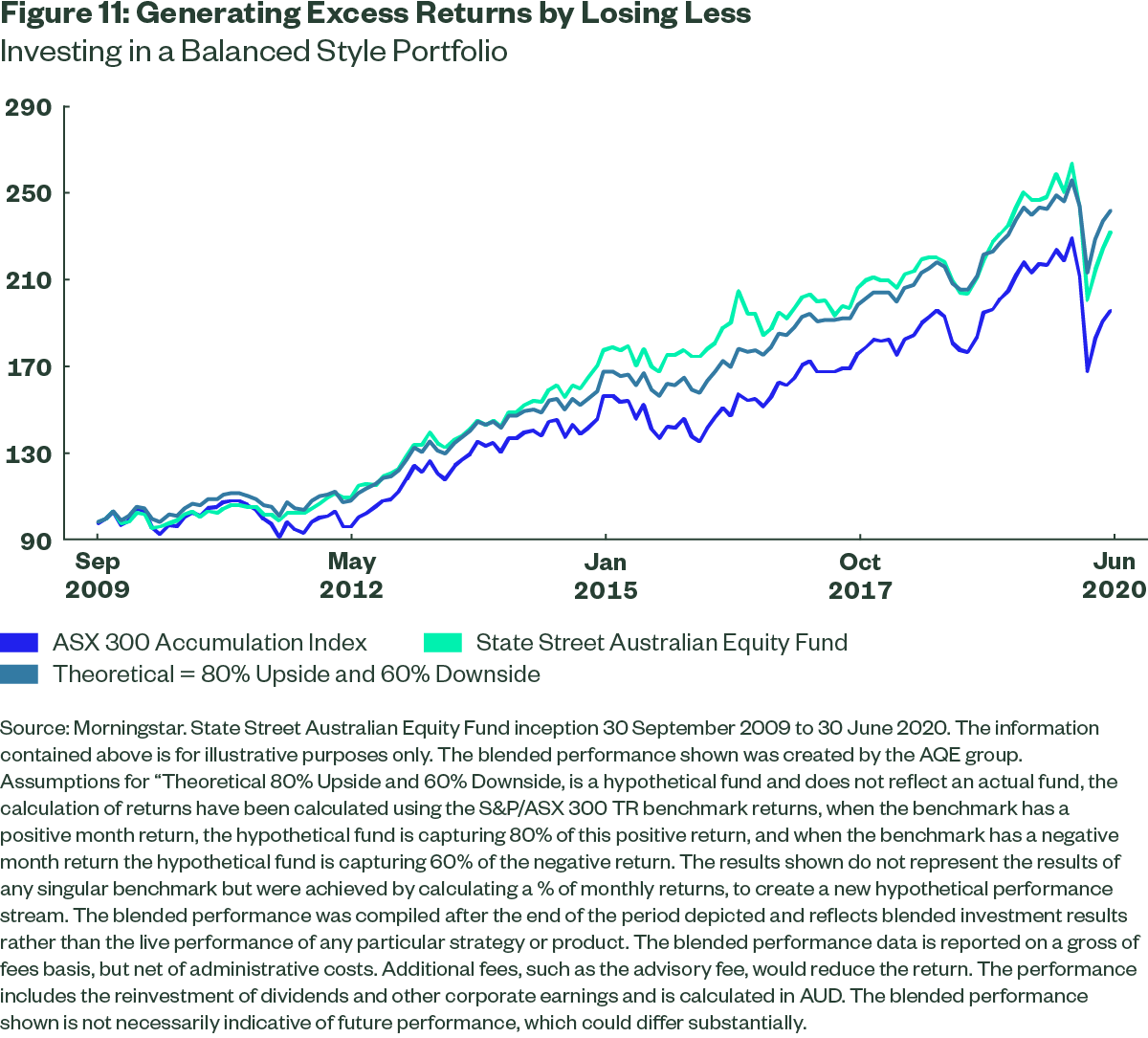

At State Street, our balanced unemotional assessment of companies from the perspectives of value, quality, growth and risk, pushes us towards more stable companies and away from the more glamorous companies. We are unapologetic for owning such boring businesses as we understand the power of more consistent returns over time. As most great sports teams understand, having a great defence is critical in winning. In funds management having a great defence is the ability to reduce capital losses. “Winning by not losing” may sound unglamorous but it is incredibly powerful for investors. In our experience, using a balanced style investment approach has resulted in the State Street Australian Equity Fund participating in about 60% of a given down month, generating most of its excess return from reducing losses. Historically, this approach has generated greater outperformance in more volatile periods.

‘Winning-by-not-losing may sound unglamorous but it is incredibly powerful for investors.’

We view human emotions and biases as an integral part of financial markets. These biases are both prevalent and persistent across the business cycle, providing fertile ground for savvy investors to extract excess returns. Compared to other investment styles, a balanced approach can provide greater downside protection and consistency of returns during periods of market volatility. Boring by nature. Far from boring investment outcomes.

*as at 30 June 2020

Learn more about risk aware investing

For more details on how State Street Australian Equity Fund can play a part in your asset allocation, watch the Fund in Focus here, click the contact button below, or visit our website for more information.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Bruce is Head of Active Quantitative Equity - Australia, for State Street Global Advisors. He has over 20 years' experience, covering Australian and global equites, long and short equities as well as global macro strategies.

........

Issued by State Street Global Advisors, Australia Services Limited (AFSL Number 274900, ABN 16 108 671 441) (“SSGA, ASL”). Registered office: Level 14, 420 George Street, Sydney, NSW 2000, Australia · Telephone: +612 9240-7600 · Web: ssga.com. State Street Global Advisors, Australia, Limited (AFSL Number 238276, ABN 42 003 914 225) (“SSGA Australia”) is the Investment Manager.

References to the State Street Australian Equity Fund ("the Fund") in this communication are references to the managed investment scheme domiciled in Australia, promoted by SSGA Australia, in respect of which SSGA, ASL is the Responsible Entity.

This communication is intended for professional investors, as defined under the Australian Corporations Act 2001 (Cth).

This general information has been prepared without taking into account your individual objectives, financial situation or needs and you should consider whether it is appropriate for you. You should seek professional advice and consider the product disclosure document, available at ssga.com, before deciding whether to acquire or continue to hold units in the Funds.

The views expressed in this material are the views of the SSGA Australian Active Quantitative Equity Team through the period ended 10 September 2020 and are subject to change based on market and other conditions. The information provided does not constitute investment advice and it should not be relied on as such. All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

Investing involves risk including the risk of loss of principal. Risk associated with equity investing includes stock values which may fluctuate in response to the activities of individual companies and general market and economic conditions. The strategy is actively managed and may underperform its benchmarks. An investment in the strategy is not appropriate for all investors and is not intended to be a complete investment program. Investing in the strategy involves risks, including the risk that investors may receive little or no return on the investment or that investors may lose part or even all of the investment. Past performance is not a reliable indicator of future performance.

This material should not be considered a solicitation to apply for interests in the Funds and investors should obtain independent financial and other professional advice before making investment decisions. There is no representation or warranty as to the currency or accuracy of, nor liability for, decisions based on such information.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA Australia’s express written consent.

© 2020 State Street Corporation - All Rights Reserved

3 topics

8 stocks mentioned

Head of Portfolio Management – Australia, Active Quantitative Equity

State Street Global Advisors

Bruce is Head of Active Quantitative Equity - Australia, for State Street Global Advisors. He has over 20 years' experience, covering Australian and global equites, long and short equities as well as global macro strategies.

Head of Portfolio Management – Australia, Active Quantitative Equity

State Street Global Advisors

Bruce is Head of Active Quantitative Equity - Australia, for State Street Global Advisors. He has over 20 years' experience, covering Australian and global equites, long and short equities as well as global macro strategies.

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets