Revolutions and volatility

Brett Gillespie

Global Macro

Who said “Let them eat cake”? Most will answer Marie Antoinette. The Storming of the Bastille on the 14th July, 1789 marked the beginning of a French Revolution that was to last 10 years, overthrow the monarchy and replace it with a Republic, only to then see a military coup by a new Emperor and dictator - Napoleon. Indeed, many historians regard the revolution as one of the most important events in human history.

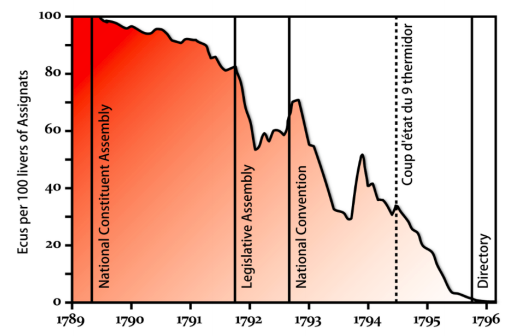

However, few historians realise it also included arguably the first aggressive experiment and most spectacular failure of quantitative easing. The Chinese invented paper money of course (commonly called fiat money) around 1000AD. They too debased it from time to time. But nothing like this period in French history. Imagine you are a peasant in 18th century France. 50% of your income is spent on bread. Between 1790 and 1795, the price of flour rose ten thousand per cent… Perhaps then not so hard to understand the execution of King Louis XVI in 1793.

But how did it happen? I love the explanation given by Professor Andrew White of Cornell University in 1912. From 1860 he collected all the information he could on the period, in particular from newspapers and pamphlets of the day. And then documented how smart people could oversee such a disaster. Well worth a read (and only 90 pages). But for the 99% who won’t read it; the government seized all the church land in France – 1/3 of all French land no less – and then used that land as the asset to back the paper currency.

They argued that as the paper money was convertible for land, the supply was limited, and as such, not inflationary. The only problem was when they started printing, they couldn’t stop.

Within 7 years, the currency was literally worthless.

Naturally, inflation soared. Some made fortunes as they borrowed heavily and moved into real assets – land and stocks, and sold the currency. But anyone who relied on a wage was destitute. France turned into a nation of “stock jobbers and gamblers”.

A modern-day revolution

Why am I talking about this? After all, there is no rampant inflation anywhere in the developed world. Yet we are seeing a modern day revolution. Brexit, Trump, and the rise of right-wing parties in Germany, France and Italy. Why is that?

One word: Inequality.

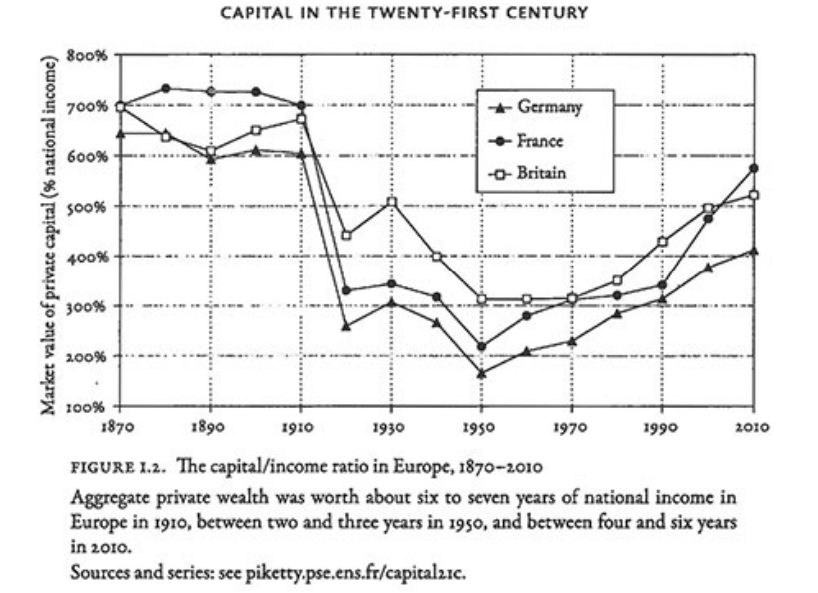

Inequality drives revolutions. Put simply, a lot of people are finding life very hard. Piketty’s “Capital” explains that wealth will accumulate to the wealthy simply because investment returns generally exceed wage rises. Except in war. Most of Europe’s wealth was wiped out in WW1 and WW2, before re-starting the trend rebuild in 1950.

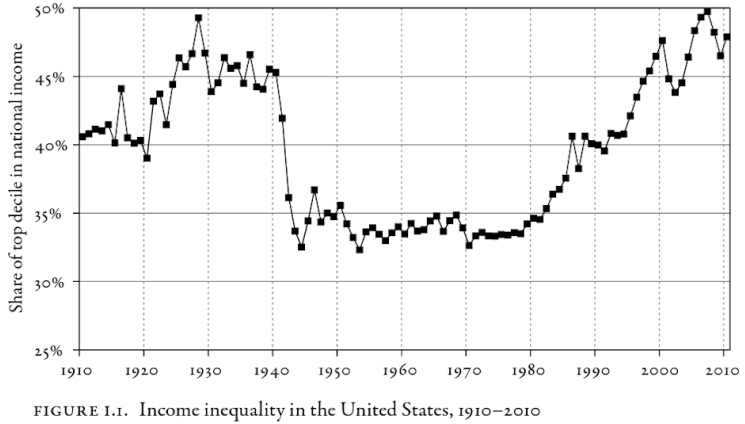

The long term inequality in income is also very interesting. Pikkety shows what % of national income goes to the top 10% of earners in the US. It plummeted during WW2. But it accelerated sharply from 1980.

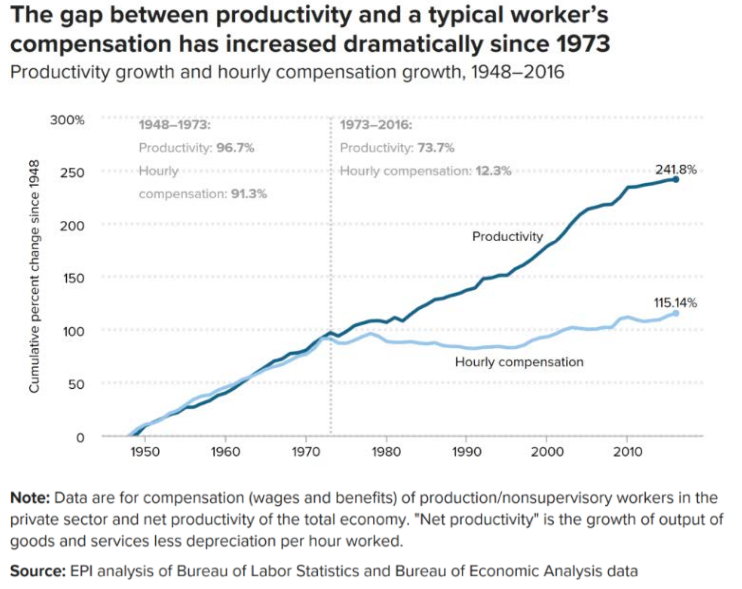

Why? Globalisation and deregulation (some call it financialisation), initated by Thatcher and Reagan and the mantra of every Western Government ever since. And more recently, quantitative easing (QE) and zero interest rates. It can certainly be shown that economies benefit in aggregate from globalisation, deregulation and QE. The problem is the benefits have not been evenly distributed. For example, there has been virtually no rise in real wages in the US since 1973.

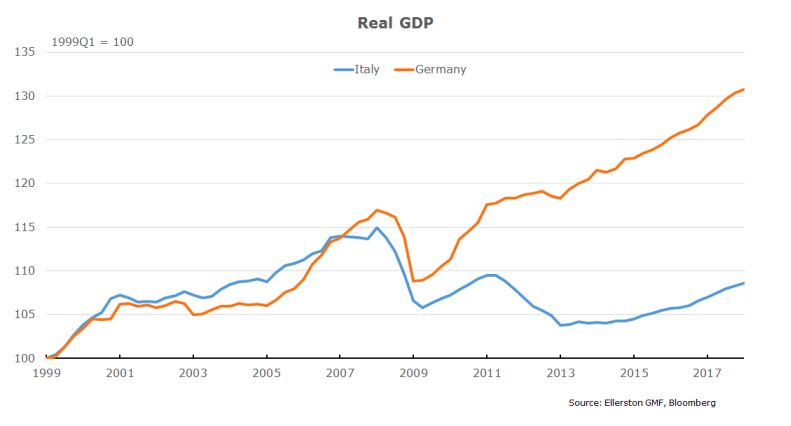

This is a massive topic, and I am not even scratching the surface. But what is clear is the global financial crisis has seen the proverbial dummy spit by many voters. For decades they have been promised the benefits of globalisation and deregulation. After the financial crisis, the rebellion has started. Many voters, in many countries, are saying enough, it hasn’t worked for us! Which of course brings me to Italy. And the Eurozone. This week saw the formation of a coalition between the extreme left and the extreme right of Italian politics – the most unlikley of bedfellows one would assume! And well it may prove to be…But they have one thing in common. They are both populist parties supported by people who have had enough of the current arrangement. And like the US worker, it is not hard to understand the Italian citizen when we look at the relative performance of the Italian economy.

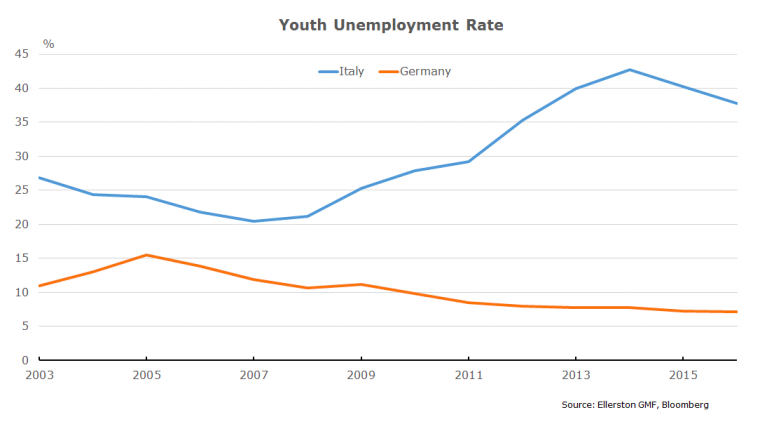

Or perhaps if we look at the average young Italian. Youth unemployment in Germany is 7%. In Italy? Call it 40%!

Hence the revolution, with both the extreme left and extreme right parties winning the most votes, and strangely forming a coalition at the end of May. The 5 Star party is anti-establishment. The Nothern league is anti-immigration. 5 Star has pledged guaranteed income for the poor and a lower pension age. The Nothern League has promised hefty tax cuts and tougher immigration policies. Initially they wanted as finance minister 81 year old Paola Savona, a fierce critic of the Maastricht Treaty and the Euro. Markets panicked. It was one thing to have a fiscally irresponsible government in Italy. It was entirely a different matter if Italy by any stretch of the imagination would seek to leave the Euro. The interest rate the Italian government has to pay to borrow for 2 years jumped from -0.3% (yes they have negative rates in Europe) to 2.75%. Levels not seen since Greece threatened to leave the Eurozone.

Savona’s main complaint is that the construct of the Eurozone, and the power of Germany, are crippling Italy. Savona makes two good points:

1. There needs to be fiscal transfer in Europe, particularly with regard to unemployment benefits.7

2. The cost of illegal immigrants to Europe is being disproportionately worn by Italy, estimated at some 4 billion Euro a year by the Italian government.8 (and Germany, which of course he doesn’t mention)

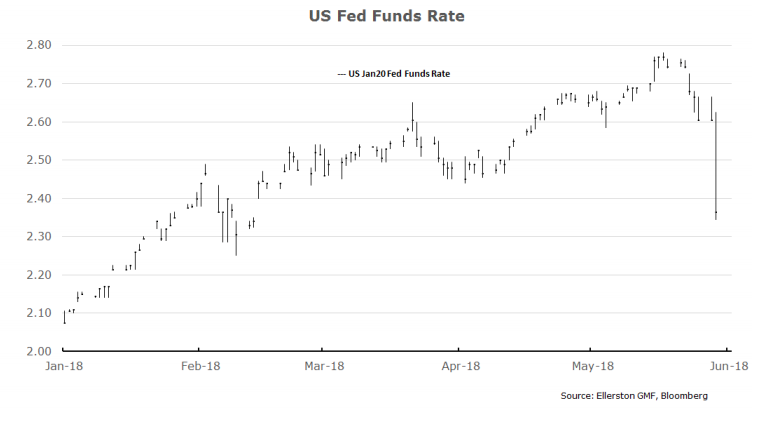

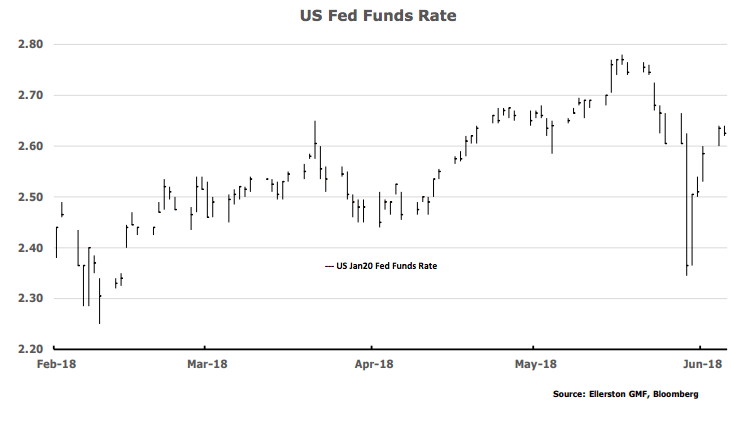

Markets calmed as Savona was moved from the finance ministry to Minister of EU Affairs, and 5 Star and Northern League re-iterated they have no intention of leaving the Euro. If so, it could be what saves the Euro, rather than destroys it, as reform is sorely needed. But it will be a bumpy ride. It is hard to get Germany motivated about reform – without a crisis… With the conniption in Italian bonds, the world went “risk-off”. US treasuries had the biggest one week rally (fall in yields) in 2 years, some 30 basis points. We were heavily positioned for Fed rate hikes to continue through this year and next. On the 22nd of May the market expected the US cash rate to be 2.75% at the end of 2019 (currently 1.9%). By the 29th of May that expectation had dropped to 2.35% - where it was at the end of January.

We expect it to get to 3.15-3.4%. What did we do? What would you do? If, for example, you bought Facebook at $190, expecting it to rise to $220, and it drops to $150, what would you have done? For us, when an outsized move like this happens that is contrary to our view, we defend. Our first and foremost goal is don’t lose (too much) money. Hence when Italian yields started to rise, we increased our holdings on bunds in case the situation escalated. This helped mitigate losses.

Most importantly, we have “stop loss” trades in the broker market to close our exposure when the market is moving against us. Think an order with your broker to sell your Facebook shares at $175. That way you limit your loss and the investment has a good risk reward. Every “stop loss” we had in US rates was executed on May 29th by 4am Sydney time. Portfolio risk was automatically reduced from 55% of maximum risk to 15%. (Some option trades remained). We were automatically de-risked and capital was preserved.

Secondly, we then look to take advantage of the situation. Is the move correct? Will it go further? Or is it an opportunity.

By 7am, after assessing the reason for the move and the relative market performances, we concluded the following;

1. The markets that had moved the most were the markets that had the largest “positions” in them and were most prone to reversal, namely Italian bonds and German and US bonds. Other “risk” markets, such as equities, had much more muted responses.

2. Often when markets have these “positioning wipe outs” they reverse very quickly

3. The Italian political situation was still unclear, but the market had quickly jumped to the worst case. 4. We had important US data at the end of the week, namely employment and manufacturing data, which we believed would show a reaccelerating economy and support ever higher interest rate expectations in the US.

So what does one do? Well once the portfolio is under control, my goal is if the market reverses we at a minimum make back what we have lost, preferably more given the opportunity. We decided to go for more, but safely. So like February, we bought 1 week put options on US 10 year bonds. Very short dated, to capture a quick reversal plus strong data at the end of the week

Unfortunately our May performance does not include the day the data was released, the 1st of June. Whilst making no guarantee about performance in June, I can say we got the economic data and reversal right, and have recaptured all of the under-performance in May in first 2 days of June. If yields fully reverse the rally we are on track to comfortably make more than we lost.

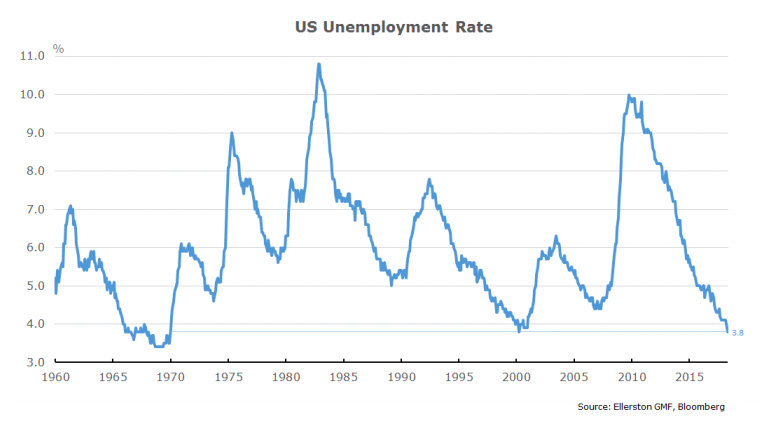

So what was the data? Well the unemployment rate has not been lower in the US since 1969.

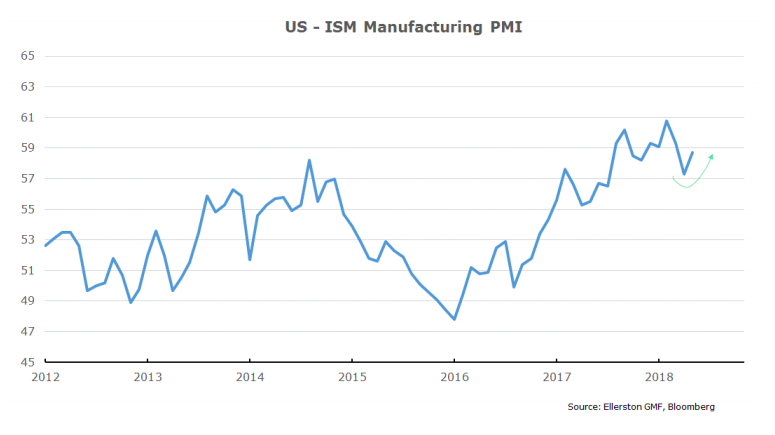

And where the consensus believed the US manufacturing sector was slowing, it has suddenly reaccelerated.

So after the dislocation in May, we find ourselves in a situation where the data in the US suggest the case for higher US rates is only getting stronger. Indeed, the risk that the Fed is “behind the curve” is nudging higher. If you recall, we have two drivers for higher US yields.

a) Normalisation of global real rates in bond markets, which have been suppressed by bond purchases by global central banks. This should comfortably see US 10 year yields rise to 3.5- 3.75%, probably by year end depending on the ECB (though less so as the Fed continues to hike)

b) A restoration of inflation risk premium. Policy is incredibly accommodative across the developed world for this stage of the business cycle. The US is most progressed in the business cycle, and accelerating. Business surveys and company anecdotes indicate significant inflation pressure is building. An acceleration in inflation now would be very alarming given the policy stance, and likely see a break of 4% bond yields in the US.

At the same time, we are in a new political world, indeed what could be a multi decade political readjustment away from the economics of globalisation and deregulation, and back to nationalism and protectionism. This both taxes growth and boosts inflation – (mild) stagflation if you like. That will mean different things for different economies, but for the US it will require tighter policy.

On the geopolitical front, North Korean/US tensions appear set to ease, but tariff tensions continue to ebb and flow, as will Italian concerns. For mine, Italy can cut both ways. It might accelerate reform and save the Eurozone, or end it. Either way the Italians have decided to move the patient into the operating theatre. It is going to be a long operation…

So we will still need insurance in the portfolio. European interest rates are no longer attractive given how far they have moved in the last week of May. We remain short the Euro currency, which works as a hedge when/if Italy escalates, but is also supported by our work on currency drivers

And we have rebuilt short bond positions in the US.

But between a recalcitrant Italy and a vacillating Trump, the market will remain on tenterhooks. Either have the potential to illicit panic as markets extrapolate suggestions. As such, we will be careful to keep hedges in the portfolio in the most cost effective fashion, typically utilising currency options, equity put options, and bonds in countries outside the US as opportunities arise. At month end we held options for a weaker Euro currency.

Meanwhile it is vital not to miss the forest for the trees. The US economy is not only fully employed, but accelerating. As one might expect if policy is still accommodative. The real risk over the next two to three years is not Italy. It is not tariffs. It is restrictive monetary policy and a “normal” US recession.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Brett has worked in the financial services industry for over 28 years. Most recently he was Head of Global Macro at Ellerston Capital. Prior to that he spent over 10 years as Senior Portfolio Manager at Tudor Investment Corporation.

3 topics

Brett Gillespie

Investor

Global Macro

Brett has worked in the financial services industry for over 28 years. Most recently he was Head of Global Macro at Ellerston Capital. Prior to that he spent over 10 years as Senior Portfolio Manager at Tudor Investment Corporation.

Expertise

Brett Gillespie

Investor

Global Macro

Brett has worked in the financial services industry for over 28 years. Most recently he was Head of Global Macro at Ellerston Capital. Prior to that he spent over 10 years as Senior Portfolio Manager at Tudor Investment Corporation.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets