13 tips for managing your finances

Getting your personal finances right can be a challenge. Here are 13 tips that may be of use: shop around when it comes to financial services; don’t take on too much debt; allow that interest rates can go up as well as down; allow for rainy days; credit cards are great but they deserve respect; use your mortgage (if you can) for all longer term debt; start saving and investing early; allow that asset prices go up and down; try and see financial events in their longer-term context; know your risk tolerance; make the most of the Mum and Dad bank; be wary of the crowd; and there is no free lunch.

Introduction

A few months ago Reserve Bank Governor Phillip Lowe provided four common sense points we should all keep in mind regarding borrowing to finance a home. (The Governor’s speech can be found here). I thought they made sense and so summarised them in a tweet to which someone replied that every checkout operator knows them.

Which got me thinking that maybe many do know them, but a lot don’t, otherwise Australians would never have trouble with their finances. So I thought it would be useful to expand Governor Lowe’s list to cover broader financing and investment decisions we make. I have deliberately kept it simple and in many cases this draws on personal experience. I won’t tell you to have a budget though because that’s like telling you to suck eggs.

1. Shop around

We often shop around to get the best deal when it comes to consumer items but the same should apply to financial services. As Governor Lowe points out “don’t be shy to ask for a better deal whether for your mortgage, your electricity contract or your phone plan”. The same applies to your insurance, banking, superannuation, etc. It’s a highly competitive world out there and financial companies want to get and keep your business. So when getting a new financial service it makes sense to look around. And when it comes time to renew a service – say your home and contents insurance - and you find that the annual charge has gone up way in excess of inflation (which is currently around 2%) it makes sense to call your provider to ask what gives. I have often done this to then be offered a better deal on the grounds that I am a long-term loyal customer.

2. Don’t take on too much debt

Debt is great, up to a point. It helps you have today what you would otherwise have to wait till tomorrow for. It enables you to spread the costs associated with long-term “assets” like a home over the years you get the benefit of it and it enables you to enhance your underlying investment returns. But as with everything you can have too much of it. Someone wise once said, “it’s not what you own that will send you bust but what you owe.” So always make sure that you don’t take on so much debt that it may force you to sell all your investments just at the time you should be adding to them or worse still potentially send you bust. Or to sell your house when it has fallen in value. A rough guide may be that when debt servicing costs exceed 30% of your income then maybe you have too much debt – but it depends on your income and expenses. A higher income person could manage a higher debt servicing to income ratio simply because living expenses take up less of their income.

3. Allow that interest rates can go up as well as down

Yeah, I know that it’s a long time since official interest rates were last raised in Australia – in fact it was way back in 2010. So as Governor Lowe observes “many borrowers have never experienced a rise in official interest rates”. But don’t be fooled by the recent history of falling or low rates. My view is that an increase in rates is still a long way off (and they may even fall further first) - but that’s just a view and views can be wrong. History tells us that eventually the interest rate cycle will turn up. Just look at the US where after six years of near zero interest rates, official US interest rates have risen 2% over the last three years. So, the key is to make sure you can afford higher interest payments at some point. And when official rates move up the moves tend to be a lot larger than the small out of cycle moves from banks that have caused much angst lately.

4. Allow for rainy days

This is another one raised by Governor Lowe who said: “things don’t always turn out as we expect. So for most of us having a buffer against the unexpected makes a lot of sense.” The rainy day could come as a result of higher interest rates, job loss or an unexpected expense. This basically means not taking all the debt offered to you, trying to stay ahead of your payments and making sure that when you draw down your loan you can withstand at least a 2% rise in interest rates.

5. Credit cards are great, but they deserve respect

I love my credit cards. They provide me with free credit for up to around 6-7 weeks and they attract points that can really mount up (just convert the points into gift cards and they make optimal Christmas presents!). So, it makes sense to put as much of my expenses as I can on them. But they charge usurious interest rates of around 20-21% if I get a cash advance or don’t pay the full balance by the due date. So never get a cash advance unless it’s an absolute emergency and always pay by the due date. Sure the 20-21% rate sounds a rip-off but don’t forget that credit card debt is not secured by your house and at least the high rate provides that extra incentive to pay by the due date.

6. Use your mortgage for longer-term debt

Credit cards are not for long-term debt, but your mortgage is. And partly because it’s secured by your house, mortgage rates are low compared to other borrowing rates – at around 4-5% for most. So if you have any debt that may take longer than the due date on your credit card to pay off then it should be on your mortgage if you have one.

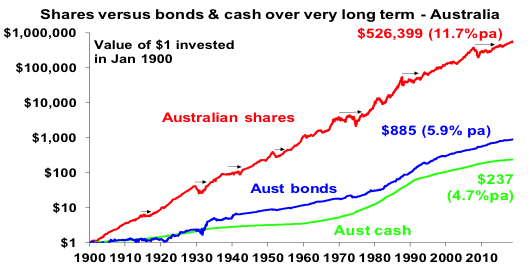

7. Start saving and investing early

If you want to build your wealth to get a deposit for a house or save for retirement the best way to do that is to take advantage of compound interest – where returns build on returns. Obviously, this works best with assets that provide high returns on average over long periods. But to make the most of it you have to start as early as possible. Which is why those piggy banks that banks periodically hand out to children have such merit in getting us into the habit of saving early.

Of course, this gives me an opportunity to again show my favourite chart on investing which tracks the value of $1 invested in Australian shares, bonds and cash since 1900 with dividends and interest reinvested along the way. Cash is safe but has low returns and that $1 will have only grown to $237 today. Shares are volatile (& so have rough periods highlighted by arrows) but if you can look through that they will grow your wealth and that $1 will have grown to $526,399 by today.

Source: Global Financial Data, AMP Capital

8. Allow that asset prices go up and down

It’s well known that the share market goes through rough patches. The volatility seen in the share market is the price we pay for higher returns than most other asset classes over the long term. But when it comes to property there seems to be an urban myth that it never goes down in value. Of course, property prices will always be smoother than share prices because it’s not traded daily and so is not subject to daily swings in sentiment. But history tells home prices do go down as well as up. Japanese property prices fell for almost two decades after the 1980s bubble years, US and some European countries’ property values fell sharply in the GFC and the Australian residential property market has seen several episodes of falls over the years and of course we are going through one right now. So the key is to allow that asset prices don’t always go up – even when the population and the economy are growing.

9. Try and see big financial events in their long-term context

Hearing that $50bn was wiped off the share market in one day sounds scary – but it tells you little about how much the market actually fell and you have only lost something if you actually sell out after the fall. Scarier was the roughly 20% fall in share markets through 2015-16 and worse still the GFC that saw roughly 50% falls. But such events happen every so often in share markets – the 1987 crash saw a 50% in a few months & Australian shares fell 59% over 1973-74. And after each, the market has gone back up. So, we have seen it all before even though the details may differ. The trick is to allow for periodic sharp falls in your investment strategy and when they do happen to remind yourself that we have seen it all before and the market will find a base and resume its long-term rising trend.

10. Know your risk tolerance

When embarking on investing it’s worth thinking about how you might respond if you found out that market movements had just wiped 20% off the value of your investments. If your response is likely to be: “I don’t like it, but this sometimes happens in markets and history tells me that if I stick to my strategy I will see a recovery in time” then no problem. But if your response might be: “I can’t sleep at night because of this, get me out of here” then maybe you should rethink your strategy as you will just end up selling at market bottoms and buying tops. So try and match your investment strategy to your risk tolerance.

11. Make the most of the Mum and Dad bank

The housing boom in Australia that got underway in the mid-1990s and reached fever pitch in Sydney & Melbourne last year has left housing very unaffordable for many. This contributed to a huge wealth transfer from Millennials to Baby Boomers and some Gen Xers. Hopefully the current home price correction underway will help in starting to correct that. But for Millennials in the meantime, if you can it makes sense to make the most of the “Mum and Dad bank”. There are two ways to do this. First stay at home with Mum and Dad as long as you can and use the cheap rent to get a foothold in the property market via a property investment and then using the benefits of being able to deduct interest costs from your income to reduce your tax bill to pay down your debt as quickly as you can so that you may be able to ultimately buy something you really want. (Of course, changes to negative gearing if there is a change to a Labor Government could affect this.) Second, consider leaning on your parents for help with a deposit. Just don’t tell my kids this!

12. Be wary of what you hear at parties

A year ago Bitcoin was all the rage. Even my dog was asking about it – but piling in at around $US19,000 a coin just when everyone was talking about it back then would not have been wise (it's now below $US6500) even though many saw it as the best thing since sliced bread. Often when the crowd is dead set on some investment it’s best to do the opposite.

13. There is no free lunch

When it comes to borrowing & investing there is no free lunch – if something looks too good to be true (whether it’s ultra-low fees or interest rates or investment products claiming ultra-high returns & low risk) then it probably is and it’s best to stay away.

Concluding comment

I have focussed here mainly on personal finance and investing at a very high level, as opposed to drilling into things like diversification and taking a long-term view to your investments. An earlier note entitled “Nine keys to successful investing” focussed in more detail on investing and can be found here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Expertise

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Why "buy and manage" is the better way to invest in stocks

Livewire Markets