2 technology stocks with structural tailwinds

Global equity markets had their highest quarterly returns in decades as markets rebounded from the March COVID-19 induced lows. The dramatic recovery was led by essentially a ‘less bad’ outlook on COVID infections and an unprecedented wave of stimulus by central banks and governments across the globe.

The key stimulus package came from US President Donald Trump who signed the Coronavirus Aid, Relief, and Economic Security Act, also known as the CARES Act. This $2 trillion US stimulus package was the largest emergency relief bill in American history. Similar packages were passed in other developed countries, combined with co-ordinated central bank efforts to lower interest rates for sovereigns and corporates alike.

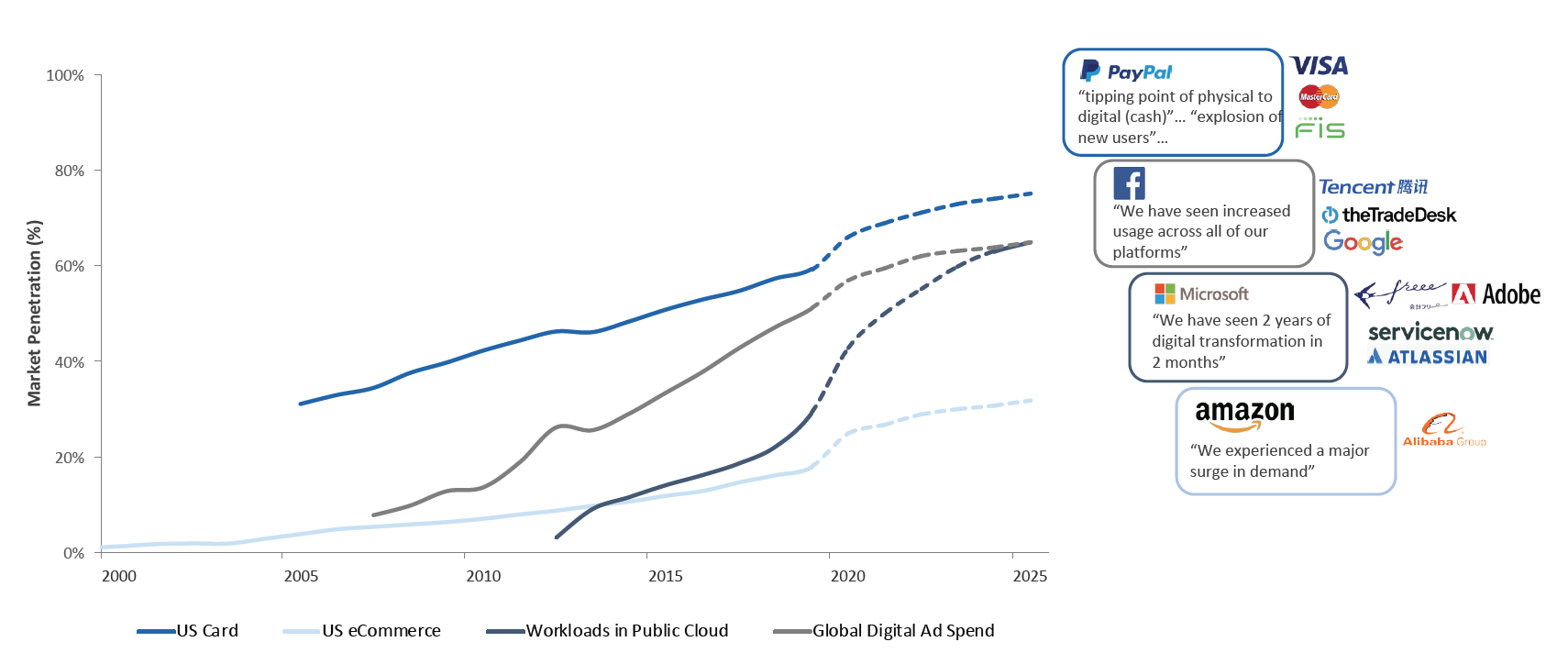

Asset prices responded in kind with all asset classes rising. However, equity markets did bifurcate from the lows with strong differentiation between the so-called digital and technology ‘winners’ in a post COVID world and the so-called bricks & mortar retail, financials and autos ‘losers’. This is most evident when looking at the calendar year performance of indices in the US, where the Nasdaq is up 13.7% and the smaller cap Russell 2000 index is down 14.2%.

Market Outlook

The COVID-19 pandemic is essentially a health crisis and by extension a solvency crisis for many small businesses across the globe. Consequently, governments and central banks alike have seen little need to worry about moral hazard or sovereign debt levels, instead moving quicker than usual to provide unprecedented levels of stimulus and far reaching interventions into credit markets which together have provided a strong firewall against any near-term solvency concerns.

Seeing these unprecedented actions and having also learnt the lesson of the ‘Powell Pivot’ in December 2018, we acted quickly to close our remaining hedges and short positions, increasing net exposure significantly over the first two weeks of April. Furthermore, we also chose to deploy our remaining cash into identified Areas of Interest (AoI) that would be better off in a post COVID world. Specifically, we have pushed portfolio exposure higher in key winning AoIs like Digital Enterprise, Digital Payments, eCommerce and Innovative Health. Many of our key portfolio holdings are now uniquely positioned to accelerate their market share dramatically as disruption speed, social distancing and the need to test the population becomes more prevalent.

We would reiterate that over the medium to long term it is far more important to correctly identify an area of structural growth and the companies set to benefit from that growth, than to try to predict the direction of the economy or market.

With so many areas of disruption occurring at once post COVID-19, we feel confident about the opportunities ahead over the medium to long term.

That said, it would be naïve to think that there are not more twists and turns in the road ahead given the global pandemic. While we are comfortable in our core holdings, we remain watchful for large market drawdowns and are prepared to use our capital preservation tools again should they be required in the months ahead.

Source: Company Filings, Magna, Morgan Stanley, Munro estimates 30 June 2020

PayPal

The 2020 COVID pandemic has proved an accelerant for digital payments. As consumers have been required to stay at home, e-commerce has become an essential service for many, particularly to buy groceries and pharmaceutical products, and it has also benefited from the shift in spending away from travel and entertainment. Elsewhere, cash has been deemed a virus transmitter, with many businesses and individuals choosing to no longer accept it as a form of payment.

PayPal is the dominant online payment platform, sitting at the forefront of the Digital Payments structural growth trend and has been a core holding in the Fund since early 2018. PayPal operates as a three-sided platform: it connects the bank, consumer and merchant selling online goods to securely process online transactions.

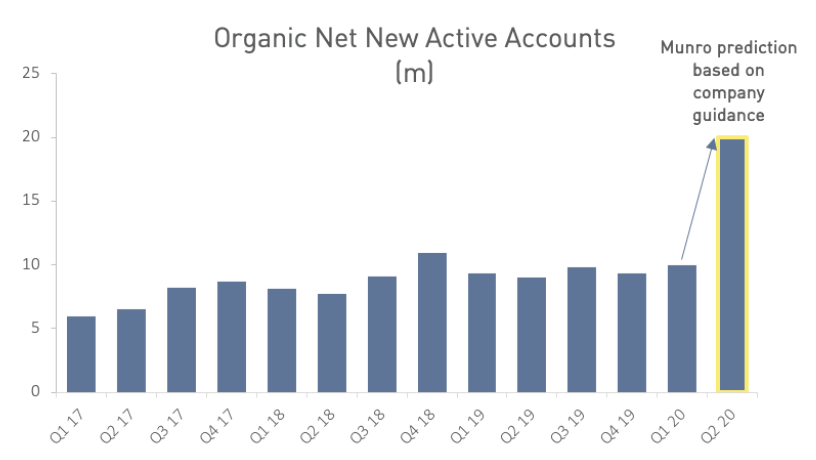

While PayPal’s Q1 results were in line with expectations, comments on its accelerating outlook by CEO Dan Schulman were what drove the recent strong performance. As evidence of this positive inflection, on the 1st of May, PayPal had its largest single day of transactions in history, larger than either of Black Friday and Cyber Monday last year.

The company also reports how many ‘net new actives’ have joined the platform, i.e. net new users adopting PayPal. Typically, PayPal reports 3-4 million net new active users per quarter. During April alone, the company recorded 7.4 million net new active users for a single month and looks on track to deliver nearly 20 million net new active users for the 2nd quarter, (see below). Despite the strong recent performance, we see PayPal as only beginning to monetise these new consumers and expect wider adoption and further performance in the years ahead.

ServiceNow

As the market leader in IT Service Management software, ServiceNow is automating IT departments and help desks, as well as enabling them to function virtually, all over the world. While ServiceNow’s Q1 results were good, the outlook was also upbeat with the business quickly pivoting to remote working and virtual implementations. CEO Bill McDermott said on the call that

“Post COVID, digital transformation will accelerate, and ServiceNow is the workflow standard for digital transformation. And most important, the Now Platform, the platform of platforms, has become the standard for workflow design experiences”.

Like many of our software investments, ServiceNow is dominating its core vertical, which in this case is IT support. This domination allows increased R&D investments to create increased functionality and network effects which in turn creates further domination.

ServiceNow’s latest software update includes chatbots that automate low level IT helpdesk queries such as resetting passwords; allowing human IT power to focus on more complex requests. Also included were machine learning features – by observing thousands of past queries the machine ascertains what the best outcome is, having learned from history. These features could add significant value in a COVID world where IT help desks have been overwhelmed by the volume of requests.

Other key products in HR and Customer Service Management are early in their life cycle, with management estimating they are 1% penetrated in their addressable markets. Here ServiceNow is the workflow management software that sits on top of the underlying system of record software products. For example, an employee onboarding process touches many different departments from HR, payroll, security, etc. ServiceNow’s product allows for automated workflow of this process.

ServiceNow has been a core holding in the fund since early 2018 and the investment case looks as attractive as ever; with the acceleration of digital transformation and vast growth opportunities ahead for a company that is already growing revenues at >30% per annum at close to a 30% FCF margin.

Want to learn more?

Munro focuses on identifying and investing in companies that have the potential to grow at a faster rate and on a more sustainable basis than the peer group. To find out more, hit contact below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nick is a founding Partner and the Chief Investment Officer of Munro Partners. He is responsible for the investment management of Munro’s key investment funds and the formulation and implementation of the proprietary investment process. Nick has over 20 years of financial services experience and over 14 years managing absolute return mandates focused on global growth equities.

........

The material contained in this publication is being furnished for general information purposes only as is not investment advice of any nature. The information contained in this document reflects, as of the date of publication, the views of Munro Partners and sources believed by Munro Partners to be reliable. There can be no guarantee that any projection, forecast or opinion in these materials will be realised. The views expressed in this document may change at any time subsequent to the date of issue.

This information has been prepared without taking account of the objectives, financial situation or needs of individuals. Before making an investment decision, investors should consider the appropriateness of this information, having regard to their own objectives, financial situation and needs.

Past performance information given in this document is given for illustrative purposes only and should not be relied upon as (and is not) an indication of future performance. No representation or warranty is made concerning the accuracy of any data contained in this document.

3 topics

Nick is a founding Partner and the Chief Investment Officer of Munro Partners. He is responsible for the investment management of Munro’s key investment funds and the formulation and implementation of the proprietary investment process. Nick has...

Expertise

Nick is a founding Partner and the Chief Investment Officer of Munro Partners. He is responsible for the investment management of Munro’s key investment funds and the formulation and implementation of the proprietary investment process. Nick has...

Expertise

Comments

Comments

Sign In or Join Free to comment