2018: A taste of what's to come

Livewire recently got in touch with us to tell the story of 2018 in one chart, and how it is instructive going into 2019. Our choice, the 3 Month US Treasury Bill Yield.

Why is it important?

Even if you have no exposure to fixed income, interest rates still matter … a lot.

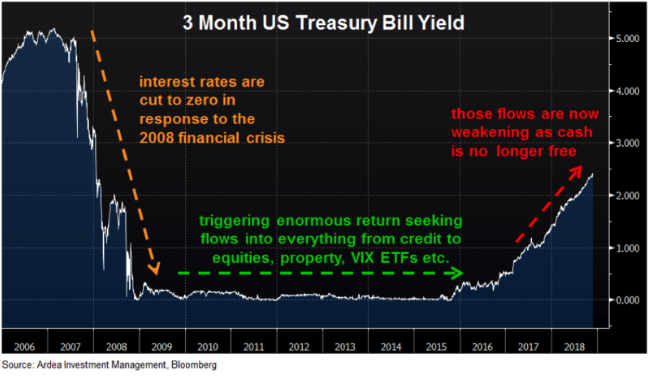

Having minimal credit or interest rate risk (politics aside), the interest rate on very short dated US government bonds, referred to as Treasury Bills (or T Bills), can be used as a proxy for a risk free rate of return. In response to the 2008 financial crisis, central banks around the world cut interest rates and embarked on an unprecedented program of monetary stimulus. As a result, risk free rates around the world fell to zero. This had two related effects:

1. Asset prices pushed higher

Risk free rates form the foundation from which all discount rates are calculated. These discount rates are then used to value cash flows generated by assets ranging from bonds to stocks to real estate. As discount rates fell, the valuation of cash flows rose and therefore asset prices were pushed higher.

2. The reach for yield

Secondly, as the rate of return investors could get from lower risk assets fell in line with risk free rates, a great rotation of capital began that has lasted for the past ten years. A wall of money progressively moved up the risk spectrum, into riskier and riskier assets, in order to generate higher returns … the so called ‘reach for yield’.

In fixed income this manifested as capital rotating out of cash deposits and government bonds into progressively riskier credit securities. More broadly, capital poured into everything from equities to emerging markets, property, VIX ETFs etc. … basically anything that offered a return above zero. This was a paradigm in which the desperate search for returns trumped considerations of how much risk was being taken to earn those returns. As risk free rates are now rising, the paradigm has changed. Cash is no longer free and those return seeking flows have correspondingly weakened. In July this year, the yield on 3 month US T Bills broke above 2%, and have since gone even higher. As the chart shows, this is a big change from the free money world investors had become accustomed to in the post financial crisis era, with more than half of that move higher happening in just the past 10 months. It’s not a coincidence that equities and pretty much all other asset classes have struggled over this period.

What does it tell us?

Firstly, the discount rate applied to all financial asset valuations is now rising and therefore, all else equal, asset prices should become more vulnerable.

Secondly, you can now earn 2.4% from risk free 3 month T Bills at a time when riskier assets are offering much smaller return pick-ups than they used to. This naturally means the compulsion to keep stretching risk budgets in the search for higher returns is no longer as strong and the risk vs. reward proposition of continuing to reach for yield is now much less appealing.

This doesn’t mean all capital flows suddenly reverse into lower risk assets. Rather, it’s subtle at first, like water leaving a bath tub when the plug is removed. Initially you hardly notice but then it becomes increasingly obvious the water is running out. We’re already seeing some evidence of this, for example in accelerating outflows from even ‘safe’ investment grade credit assets. This dynamic has negative implications for asset price valuations and volatility across all financial markets. So far 2018 has only given us a small taste of this … we expect much more going forward.

"This doesn’t mean all capital flows suddenly reverse into lower risk assets. Rather, it’s subtle at first, like water leaving a bath tub when the plug is removed. Initially you hardly notice but then it becomes increasingly obvious the water is running out"

About Ardea

Ardea Investment Management is a specialist fixed income investment boutique with a focus on delivering consistent alpha to clients through an investment process supported by a highly intuitive risk system. For further information please click here

-----------------------

The information in this article has been prepared on the basis that the Client is a wholesale client within the meaning of the Corporations Act 2001 (Cth), is general in nature and is not intended to constitute advice or a securities recommendation. It should be regarded as general information only rather than advice. Because of that, the Client should, before acting on any such information, consider its appropriateness, having regard to the Client’s objectives, financial situation and needs. Any information provided or conclusions made in this article, whether express or implied, including the case studies, do not take into account the investment objectives, financial situation and particular needs of the Client. Past performance is not a guide to future performance. Neither Ardea Investment Management (“Ardea”) (ABN 50 132 902 722, AFSL 329 828), Fidante Partners Limited (“FPL”)(ABN 94 002 835 592, AFSL 234668) nor any other person guarantees the repayment of capital or any particular rate of return of the Client portfolio. Except to the extent prohibited by statute, neither Ardea nor FPL nor any of their directors, officers, employees or agents accepts any liability (whether in negligence or otherwise) for any errors or omissions contained in this article.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Gopi Karunakaran is Ardea’s Co-Chief Investment Officer (Co-CIO), together with Ben Alexander. In this capacity they both share responsibility for overseeing the investment process and investment team, with ultimate accountability for ensuring the performance of all portfolios is consistent with client objectives.

Gopi has +20 years’ experience across global fixed income markets, including the full spectrum of global interest rate and credit markets, as well as broader macro relative value investing across equities, FX and structured products.

3 topics

1 contributor mentioned

Gopi Karunakaran is Ardea’s Co-Chief Investment Officer (Co-CIO), together with Ben Alexander. In this capacity they both share responsibility for overseeing the investment process and investment team, with ultimate accountability for ensuring the...

Expertise

Gopi Karunakaran is Ardea’s Co-Chief Investment Officer (Co-CIO), together with Ben Alexander. In this capacity they both share responsibility for overseeing the investment process and investment team, with ultimate accountability for ensuring the...

Expertise

Comments

Comments

Sign In or Join Free to comment