2025 commodities outlook: iron ore, copper, uranium, lithium and more

The Australian Government's commodity forecaster is expecting further weakness in iron ore, strength in uranium and elevated gold prices.

The Australian Government's commodity forecaster, the Office of the Chief Economist – publishes a report every quarter, which forecasts the value, volume and price of major resources and commodity exports.

In this article, I've summarised some key takeaways for the most high-profile commodities including iron ore, copper and uranium. While these forecasts tend to be conservative, they've proven reliable in predicting market trends and flagging potential upside/downside risks to prices.

Iron Ore: More Weakness to Come

- Near-term demand and supply drivers: Global steel demand has been relatively weak in 2024, particularly in the second half. In October 2024, the World Steel Association downgraded its short-term steel demand outlook for most major economies, citing persistent weakness in global manufacturing.

- Global steel production is projected to gradually recover over the next two years, up 0.9% in 2025 and 1.3% in 2026. However, weakness in the all-important Chinese property sector is set to continue, offset by potential investments across infrastructure and manufacturing sectors.

- New capacity from Australia (Rio Tinto, BHP and Fortescue), Brazil (iron ore exports forecast to grow 6% pa through to 2026) and Africa could weigh on prices.

- Price forecast: Average price projected at US$80 a tonne in 2025, falling to US$76 over the outlook period (to 2026).

- Upside risks: Stronger-than-expected demand recovery in China or emerging Asia, faster-than-expected fall in interest rates.

- Downside risks: Higher-than-anticipated supply growth from Australian majors and Brazil, weaker-than-expected steel demand from China.

Oil: Geopolitical Upside

- Near-term demand and supply drivers: The US continues to ramp up shale oil production, driven by improved drilling efficiencies and cost reductions, which in turn helps offset cuts by OPEC. However, OPEC and its allies have implemented production cuts to stabilise prices in response to weaker demand. These cuts are expected to persist in 2025, but compliance among members varies, creating some uncertainty. Ongoing tensions in the region, particularly in Israel and Gaza, raise concerns about potential disruptions to oil supplies.

- Price forecast: Oil prices to stabilise around US$74 a barrel in 2025 and gradually ease to US$69 over the outlook period.

- Upside risks: A broader conflict could impact production and transportation, particularly through critical chokepoints like the Strait of Hormuz (which handles approximately 20% of global oil trade). Spare capacity among major producers remains tight, especially within OPEC. This limited buffer could exacerbate price volatility in the event of unexpected supply disruptions. In addition, if China's recent policy measures to boost growth succeed, oil demand could rebound significantly, increasing imports and tightening supply.

- Downside risks: Continued struggles in China’s property and industrial sectors could dampen global demand, outweighing growth in emerging markets. Faster-than-expected production increases in Brazil, Guyana, and the US could lead also push the market into surplus.

Gold: Trading at Record Levels

- Near-term demand and supply drivers: Gold hit a peak of US$2,778 an ounce in October 2024. While prices have moderated slightly, sustained demand ensures continued support at current levels. The ongoing conflicts in the Middle East and rising tensions between global powers (e.g., US-China relations) have increased investor appetite for gold as a safe-haven asset.

- Central banks in advanced economies, such as the Federal Reserve and European Central Bank, are moving toward more neutral or easing stances. Lower interest rates reduce the opportunity cost of holding gold (a non-yielding asset), boosting its attractiveness.

- Price forecast: Average gold price projected at US$2,552 an ounce for 2025, with risks skewed towards the upside. Prices are forecast to moderate slightly over the outlook period to US$2,391 an ounce as financial markets stabilise, reducing the urgency for safe-haven exposure.

- Upside risks: Escalating conflicts in the Middle East or other global hotspots could increase gold’s appeal as a safe-haven asset. Renewed uncertainty in global equity markets, driven by poor corporate earnings or unexpected economic shocks, could push investors toward gold.

- Downside risks: If the US dollar appreciates faster than anticipated (e.g., due to stronger-than-expected US economic growth), gold demand could weaken, especially among international buyers. If central banks delay rate cuts or tighten monetary policy further, it could increase the opportunity cost of holding gold, reducing demand. Weaker consumer spending in India and China, the largest markets for gold jewellery, could weigh on physical demand.

Uranium: Prices to Trend Higher

- Near-term demand and supply drivers: China, India, and several European nations are actively expanding or modernising their nuclear reactor fleets, a massive tailwind for uranium demand. Countries in the Middle East and Southeast Asia are also investing in nuclear energy as part of long-term energy strategies, increasing uranium demand.

- From a supply perspective, supply has been impacted by operational challenges at key mines, including those in Kazakhstan, the world's largest uranium producer. While utility companies are increasingly reliant on primary uranium supply as secondary stockpiles (recycled or military sources) are dwindling, tightening the market.

- Price forecast: Prices are forecast to tick higher in 2025, to US$83/lb and rise further to US$93 over the outlook period (to 2026).

- Upside risks: Accelerated reactor builds in China, India, and other emerging markets could outpace supply, worsening tensions involving Russia or Kazakhstan (both significant players in the nuclear fuel cycle) could disrupt supply chains and an increase in stockpiling could drive prices higher.

- Downside risks: Public opposition or policy reversals in key regions (e.g. Germany, Japan) could dampen demand, faster-than-expected production increases in Kazakhstan, Canada or Australia.

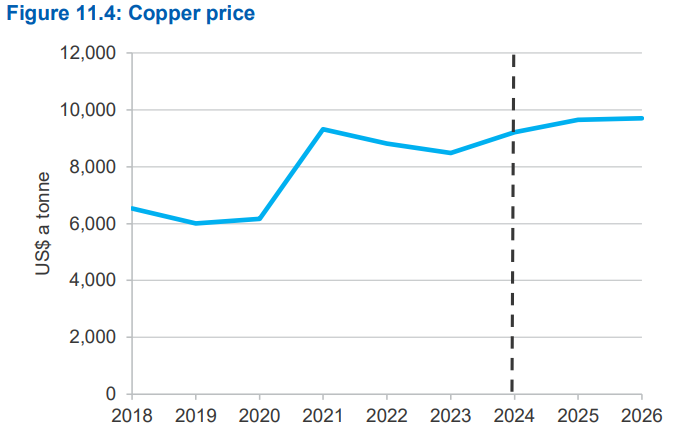

Copper: Higher Prices, Mixed Catalysts

- Near-term demand and supply drivers: China's economic slowdown, particularly in the property sector, has dampened near-term demand. However, investments in advanced manufacturing and clean energy are providing partial offsets. Global copper mine production grew by an estimated 5% in 2024, driven by operational improvements and new projects.

- However, political instability in Peru and operational challenges in Chile (both major producers) are limiting production growth potential. Copper inventories on metal exchanges such as the LME also remain low, providing an upside risk to prices if demand rebounds faster than expected.

- Price forecast: Copper prices are expected to average US$9,477 a tonne (US$4.3/lb) supported by a gradual recovery in demand and constrained inventory levels. Prices are forecast to rise further to US$9,690 (US$4.39/lb) by 2026, driven by growing demand from the energy transition and limited new supply.

- Upside risks: Faster-than-expected adoption of renewable energy systems, accelerated global infrastructure spending, delays in major mining products (e.g. Peru's Quellaveco Mine).

-

Downside risks: Prolonged property market weakness in China (consumes over 50% of global copper), faster-than-expected production ramp ups in regions such as the DRC or Mongolia.

Lithium: Another 'Nothing' Year

- Near-term demand and supply drivers: EV adoption continues to drive lithium demand globally, particularly in key markets like China, the US, and Europe. However, short-term demand has softened due to a cyclical slowdown in EV sales growth, partly tied to economic uncertainties and reduced subsidies in China.

- Major expansions in Australia, the world's largest lithium producer, and new projects in Latin America (Chile, Argentina) have contributed to a surge in supply. While emerging players in Africa, particularly Zimbabwe, are beginning to add capacity.

- Australian lithium spodumene export earnings fell 69% year-on-year in the September quarter, while lithium mine output is estimated to have risen 14% over the same time period.

- Price forecast: Lithium spodumene prices are forecast to average US$878 a tonne in 2025, reflecting the current inventory surplus and softer EV demand growth. Prices are expected to rebound to US$1,075 by 2026 as the market rebalances, supported by further EV adoption, increased renewable energy deployment and production adjustments.

- Upside risks: Delays in new mining projects, faster-than-expected EV adoption, resource nationalism (e.g. Chile, Argentina and Bolivia).

-

Downside risks: Further aggressive production expansion (Australia, Latin America and Africa), increased adoption of alternative battery technologies, further economic slowdown and changes to government subsidies.

Source: Department of Industry, Science and Resources (2024)

Source: Department of Industry, Science and Resources (2024)

This article first appeared on Market Index on Tuesday 7 January 2025.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Kerry is a Content Strategist at Market Index. He writes the daily Morning Wrap and Weekend Newsletter. Kerry is passionate about trading and the catalysts that influence the market. His content focuses on highlighting the key data and insights that matter most to investors.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies (“Livewire Contributors”). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

5 topics

Kerry is a Content Strategist at Market Index. He writes the daily Morning Wrap and Weekend Newsletter. Kerry is passionate about trading and the catalysts that influence the market. His content focuses on highlighting the key data and insights...

Expertise

Kerry is a Content Strategist at Market Index. He writes the daily Morning Wrap and Weekend Newsletter. Kerry is passionate about trading and the catalysts that influence the market. His content focuses on highlighting the key data and insights...

Expertise

Comments

Comments

Sign In or Join Free to comment