26 income opportunities are better than 10

Last Tuesday’s RBA interest rate cut and accompanying statement didn’t bode well for investors that rely on income producing assets such as bonds. Investors need to look beyond traditional asset classes to enhance yield. Emerging markets bonds have been overlooked by Australian investors and they are potentially missing out on the diversification and yield benefits.

Diversified portfolios that include emerging market bonds can achieve higher returns and lower risk than those that do not, according to VanEck’s new whitepaper, More than zero: Using emerging markets bonds to optimise portfolios.

This month's extraordinary rate cut set the official interest rate at an unprecedented 0.10%. The RBA also announced it will purchase $100 billion of five to 10-year government bonds over the next six months.

In a statement, the RBA laid out its medium term forecast: “Given the outlook for both employment and inflation, monetary and fiscal support will be required for some time. For its part, the Board will not increase the cash rate until actual inflation is sustainably within the 2 to 3 per cent target range.

“For this to occur, wages growth will have to be materially higher than it is currently. This will require significant gains in employment and a return to a tight labour market. Given the outlook, the Board is not expecting to increase the cash rate for at least three years.”

Cash is still considered risk-free, but with no yield to warrant a strategic allocation, the search to enhance yield may well force investors up the risk curve.

The EM alternative

One asset class that can enhance their yield but has been overlooked by Australian investors is emerging market bonds. There are several reasons Australian investors may not have an allocation to EM bonds based on old world beliefs, but this is the new world, where interest rates are set to stay lower for longer.

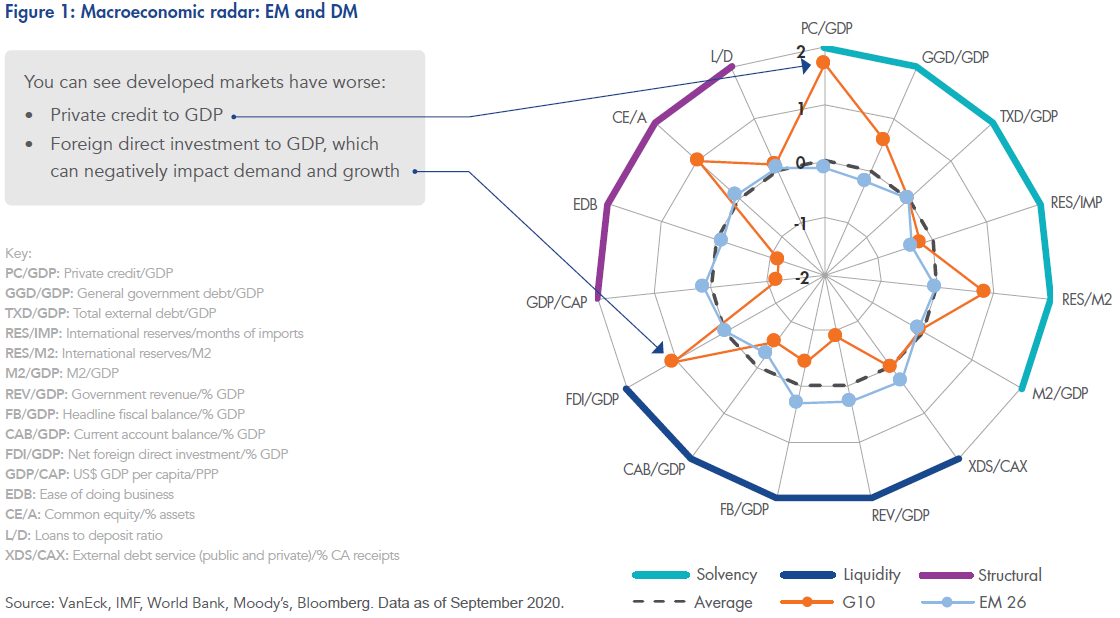

Global comparisons show that many emerging market economies are now as liquid and structurally sound as developed markets, or better. Emerging markets generally have stronger balance sheets. Looking at Figure 1, on the radar chart, the red line is the global mean. The circles represent standard deviations above and below the mean. The further you are away from the centre, the worse it is. On many metrics the G10 economies are worse than the largest 26 emerging markets.

Despite their stronger fundamentals, emerging market governments and corporations generally pay more than their developed market counterparts when they issue bonds. This presents an opportunity for investors.

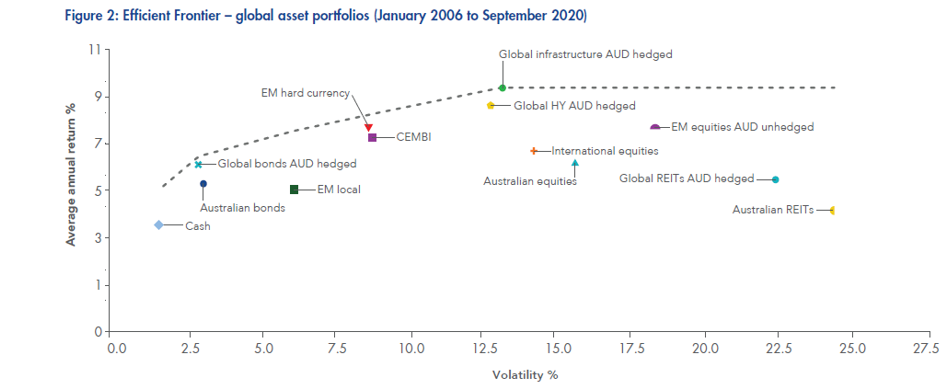

If you consider the risk and reward trade off, as you’d expect, emerging market bond volatility sits above that of developed market bonds, but well below equities. The chart below also shows that since 2006, developed market high yield bonds have experienced nearly double the risk of emerging market hard currency bonds for a similar return.

In the new world make sure your clients aren’t “Missing Out” because you haven’t considered an allocation to emerging market bonds. We recently released a whitepaper analysing the different ways investors can use emerging markets bonds in a diversified portfolio. We found that on both backward and forward looking metrics, the allocation should be more than zero – click here to find out more.

Many individual emerging market countries boast economies that are well managed and resilient bond issuers. There are many emerging market countries that have handled the COVID-19 crisis with aplomb.

This is where active management in emerging market bonds can come to the fore. Active management allows the manager to avoid those countries with weaker fundamentals and prefer those emerging market economies that are better managed and therefore better insulated from shocks such as the contraction in international trade due to a COVID-19 event.

VanEck Emerging Income Opportunities Active ETF (Managed Fund) (ASX: EBND) is an actively managed fund that is available on ASX.

VanEck’s unconstrained approach offers a number of benefits including greater diversification than approaches limited to only hard or local currency. We believe an optimal portfolio of emerging market bonds is unconstrained by indices, and invests in bonds that offer the best value relative to their fundamentals while managing risk.

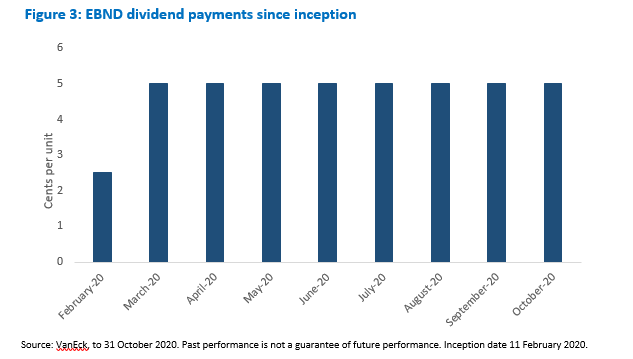

Monthly income: 5% p.a. target yield*

EBND pays dividends monthly. EBND has a target yield of 5% p.a.* Because it is a fully transparent Active ETF, EBND will trade close to its fair value because it is supported by an external market maker, which also facilitates liquidity.

At the current dividend amount, the fund is on track to have yielded 5% at the end of its first year.*

*In determining each month’s dividend VanEck will target an annual dividend yield for the fund of 5% p.a. of the capital invested at the beginning of the year. Dividend yields may differ for individual investors. From time to time we may amend this target

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Arian founded VanEck Australia and leads VanEck's Asia Pacific business. Recognised as a thought leader and with deep experience in asset management across a range of asset classes, Arian’s passion lies in designing investment solutions and he is a pioneer of smart beta strategies in Australia. VanEck is the fastest growing ETF provider in Australia.

........

Issued by VanEck Investments Limited ABN 22 146 596 116 AFSL 416755 (‘VanEck’) as the responsible entity of the VanEck Emerging Income Opportunities Active ETF (Managed Fund) (‘EBND’). Nothing in this content is a solicitation to buy or an offer to sell shares of any investment in any jurisdiction including where the offer or solicitation would be unlawful under the securities laws of such jurisdiction. This is general information only about a financial product and not personal financial advice. It does not take into account any person’s individual objectives, financial situation or needs. Before making an investment decision, you should read the PDS and with the assistance of a financial adviser consider if it is appropriate for your circumstances. The PDS is available here. An investment in EBND carries risks associated with: emerging markets bonds and currencies, bond markets generally, interest rate movements, issuer default, currency hedging, credit ratings, country and issuer concentration, liquidity and fund manager and fund operations. See the PDS for details. No member of the VanEck group of companies gives any guarantee or assurance as to the repayment of capital, the payment of income, performance, or any particular rate of return from EBND.

5 topics

Arian founded VanEck Australia and leads VanEck's Asia Pacific business. Recognised as a thought leader and with deep experience in asset management across a range of asset classes, Arian’s passion lies in designing investment solutions and he is...

Arian founded VanEck Australia and leads VanEck's Asia Pacific business. Recognised as a thought leader and with deep experience in asset management across a range of asset classes, Arian’s passion lies in designing investment solutions and he is...

Comments

Comments

Sign In or Join Free to comment