TOL - 11th Jan, 2021

3 small cap value stocks primed for the rotation

Just when you thought enough records were broken in 2020, the greatest inflows to value vs. growth in history takes place. By now everyone’s likely to have read countless research on the forces driving the recent switch to value. So, rather than recap what’s already out there, we thought to share some insights on three small cap value plays primed to benefit from the switch.

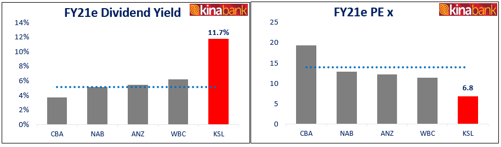

Kina Securities Limited (KSL) – Market Cap $255m

Fast Facts:

- KSL is a full service bank based in PNG offering the complete spectrum of banking services covering savings & deposits, business loans, mortgages, investments, stockbroking and funds management.

- Trading on a FY21f Price to Book value of 0.4x and Price to Earnings of 6x, representing a 64% and 56% discount respectfully to Australian banking peers.

- Attractive dividend yield of 11.7% almost triple its Australian peers.

Where’s the upside:

In November 2020 KSL acquired Westpac’s banking operations in PNG and Fiji for ~$420m. This acquisition more than doubles the size of KSL’s operations growing customers by 416%, net loans by 275% and branches and ATM’s by ~180%. Leading up to the acquisition KSL has been firing on all cylinders to grow market share and profit, they launched an extensive brand campaign, improved their digital channel and achieved a 3-year CAGR of 21%.

Key points to take from the Westpac transaction:

- KSL is cashed up from a $91m equity raise completed in October allowing them to fund the acquisition from a combination of cash and new debt;

- Importantly the acquisition will boost EPS back to levels prior to the raise, meaning there’s no earnings dilution. This also excludes any synergies KSL hopes to achieve which to us means there’s further upside to this transaction; and

- Integration risk is significantly lower with KSLs management team comprising of several ex-Westpac Executives.

KSL looks to be making all the right moves to drive immediate and future growth, paying a dividend yield well above market average and trading at a heavy discount – how long until the market picks this up?

QANTM Intellectual Property Ltd (QIP) – Market Cap $155m

Fast Facts:

- QIP owns leading Intellectual Property businesses with significant market share in Australia and a developing presence in Asia.

- Trading on a FY21f Price to Earnings multiple of 11x or ~30% discount to Industrial small cap peers.

- FY21f dividend yield of 6.1% fully franked almost double the sector average.

Where’s the upside:

We all know the certainties in life, death and taxes, I’m sure many in the business world would agree legal fees should be considered for inclusion. Often, they are non-discretionary and simply an unavoidable cost of doing business. This makes QIPs earnings defensive which was highlighted in their FY20 results. Revenue was largely uninterrupted by COVID, in fact it grow by almost 4%.

In addition to trading at a discount, offering safety with defensive earnings, and rewarding shareholders with an above average yield, the real opportunity lies in two factors:

- Firstly, management have implemented a business transformation plan estimated to cost $8m to $10m over the next 2 to 3 years with ongoing benefits of $4m to $6m p.a. This gives the project a 2 to 3 year payback period followed by ongoing benefits. If executed successfully, the transformation will strengthen margin performance which provides upside to the current share price.

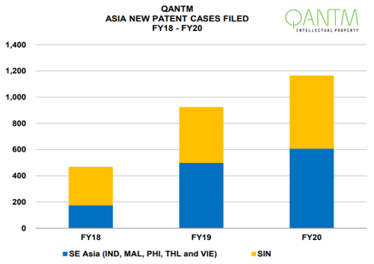

- Secondly, having already secured dominant market share in Australia, they’re building out their business in Asia with a two-pronged growth strategy. This includes replicating their exiting strategy and leveraging off their multinational client base. Total revenue from Asia currently represents 7% of group revenue, this leaves a lot of growth yet to be realised given the total addressable market of Asia.

Source: QIP management reports

Source: QIP management reportsQIP has taken charge of improving performance to drive higher margins and also pursuing external growth. Execution of these two strategies should see appreciation in the current share price, and adds to the attractiveness of this defensive and high yielding stock.

Southern Cross Electrical Engineering (SXE) – Market Cap $140m

Fast Facts:

- SXE is one of Australia’s leading electrical, instrumentation, communication and maintenance services companies.

- Trading on a FY21f Price to Earnings multiple of 12x or ~26% discount to Industrial small cap peers.

- FY21f dividend yield of 5.5% fully franked almost double the sector average.

Where’s the upside:

Over the past 4 years SXE focused on increasing diversification across sectors and they now have exposure to Resources (Mining & O&G), Industrial Projects, Utilities & Energy, Commercial Development, Public Infrastructure and Defense. This diversification adds defensiveness, and in FY20 SXE reported revenue of $415m (up 8% on pcp). This marks 3 consecutive years of record revenue which is impressive given the operating environment over the past year.

SXE is also focused on adding predictability to earnings by growing recurring revenue. Last month they completed the acquisition of Trivantage, a specialised electrical services company which is highly complementary to their existing business, and has a high degree of recurring revenue.

The opportunity lies in the following catalysts which could provide material upside:

- SXE finished FY20 with $55m cash and no debt leaving it in good shape to pursue growth organically and through M&A. The recent acquisition of Trivantage was funded with $25m cash and the balance staggered over the next 3 years. This left SXE with enough room on their balance sheet to pursue additional growth opportunities;

- The acquisition is expected to add strong double-digit EPS accretion in FY21 which provides upside to the earnings guidance provided by management in the FY20 results. SXE also hopes to achieve further upside from cross selling opportunities and achievement of synergies which will improve profit margin; and

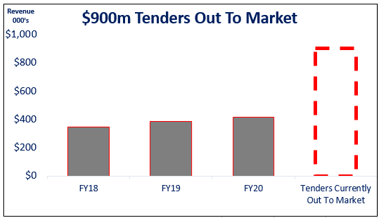

- SXE stands to benefit from Government initiatives to fast track projects and infrastructure spend. The current business development pipeline is strong with $900m of tenders out to market, this is more than double FY20 revenue.

Source: Katana Asset Management, Company Reports

Source: Katana Asset Management, Company ReportsManagement have done well to deliver 3 years of record revenue and SXE is in good shape to continue growing. SXE have tailwinds behind them in the form of government spending, and realisation of any of the above catalysts should see the stock push higher.

Closing

At Katana Asset Management we look for quality stocks with tailwinds and catalysts working to push the stock in the right direction. Quality stocks, offering growth, and real upside potential, rarely trade at a discount which makes these three value plays a strong pick for the rotation in 2021.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Hendrik is an Equities Analyst at Katana Asset Management, a specialist Australian Equities manager with over $120m FUM. He works alongside three Portfolio Managers conducting investment research and evaluation.

Hendrik has 10+ years Corporate Finance experience, and prior to joining Katana, held various positions including working on large debt restructure and capital raisings within the resource sector, Credit Analyst at Macquarie Bank and originally started his career as an Accountant at Ernst & Young.

2 topics

3 stocks mentioned

Hendrik is an Equities Analyst at Katana Asset Management, a specialist Australian Equities manager with over $120m FUM. He works alongside three Portfolio Managers conducting investment research and evaluation. Hendrik has 10+ years Corporate...

Expertise

Hendrik is an Equities Analyst at Katana Asset Management, a specialist Australian Equities manager with over $120m FUM. He works alongside three Portfolio Managers conducting investment research and evaluation. Hendrik has 10+ years Corporate...

Expertise

Comments

Comments

Sign In or Join Free to comment