What’s the single most important data point in property today?

Property has been in the spotlight in recent months, with price growth decreasing, or ceasing altogether, across Australian cities, while concerns build over potential oversupply, easing rents, and falling confidence. Falling rates have for years been a key driver of rising prices, but with increasing speculation that rates could turn higher, how would this play out in the property sector? To get some expert views on what investors could expect across residential, commercial and global property, Livewire reached out to four contributors to ask what the single most important data point is, and what is it telling them right now? Thanks for responses from Mark Pratt, General Manager at Australian Unity Real Estate Investment; Justin Blaess – Portfolio Manager Quay Global Investors; John McBain; Group CEO Centuria Capital; and Pete Wargent, Director AllenWargent.

While the Aus 10-year yield has fallen 350 bps, the AREIT index (green) has doubled

Source: FactSet

Spread between capitalisation rates and interest rates is key

Mark Pratt, General Manager at Australian Unity Real Estate Investment

Australian commercial property has seen strong demand in recent years as the global hunt for yield continues. This demand has come from onshore investors, as well as offshore investors including sovereign wealth funds. As with other yielding assets, strong demand has weighed on commercial property’s capitalisation rate: the ratio of net operating income to market value. To ask what the single most important data point to look at when assessing valuations in the sector, Livewire reached out to Mark Pratt, General Manager, Australian Unity Real Estate Investment. In this video, he explains how he reads capitalisation rates, where he things the sector goes from here, and also an emerging risk investors need to be aware of.

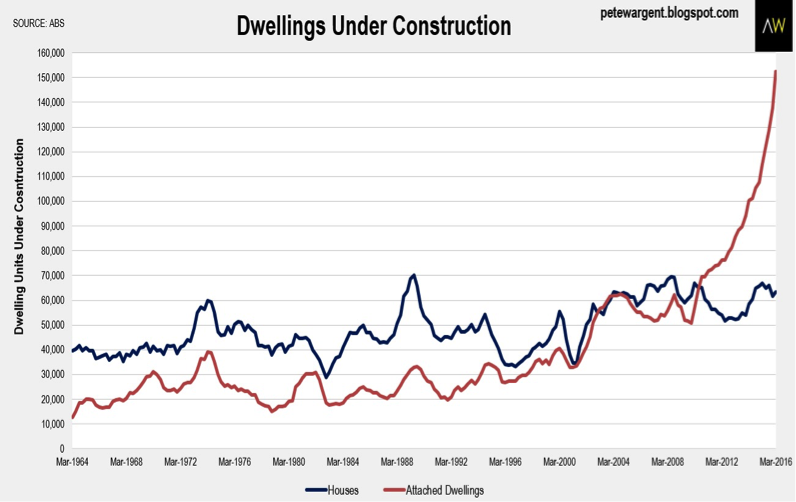

Record dwelling completions make defaults a certainty

Pete Wargent, Director, AllenWargent.

With record numbers of attached dwelling completions expected over the next two years, the key data point to watch will be new apartment non-settlements. During reporting season, non-settlements on new apartments were generally either in line with or below, long run averages. However, with Australia’s major financiers reluctant to lend to non-resident buyers, settlement risks are rising. With more than 200,000 attached dwelling completions expected across the next two years, it is a near certainty that defaults will rise from here. Mortgage stress presently isn’t that high in the capital cities, though a shift in the interest rate outlook could quickly change that.

Risk of oversupply for East Coast apartments

Justin Blaess – Portfolio Manager Quay Global Investors

We closely monitor what is happening in the markets that our investees are operating in, and a key data point to monitor is supply. If asset prices are transacting above replacement cost, developers will be incentivised to supply the market until the profit opportunities don’t exist, leading to oversupply. It is this that leads to the price and rent cycles. There is undersupply in some markets such as US housing, hence we expect robust growth and have a positive return outlook. In contrast, there seems to be risk from oversupply in other markets, such as apartments along the east coast of Australia. In the short term, noise around possible rate rises is likely to cause volatility, but it is important to understand that real estate isn’t simply an interest rate play. In fact in the last interest rate tightening cycle in the US, between June 04 and May 06, US REITs delivered +64%.

Investors position for “lower for even longer”

John McBain; Group CEO Centuria Capital

As a property funds manager investing in commercial property assets we are very focused on the premium that retail investors expect over the risk free rate of return. In practice for many small investors this becomes the premium to bank term deposit rates. There is strong support amongst this group for the proposition that interest rates will be "lower for even longer" hence we are witnessing an acceptance of lower returns for investment products than we have witnessed historically.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

1 topic

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

This recently triggered market signal has never failed to predict gains

Ophir Asset Management