8 strategies for selecting small caps

One reason regularly quoted to buy a certain stock is because it offers ‘good value’. It is certainly an easy (and lazy) argument for stockbrokers to recommend a company. When I select stocks in the small cap space (ex ASX200) I do not focus on value as I find 'value’ to be one of the most confused, overused, misleading and irrelevant factors with respect to share-market opportunities.

I don't think readers specifically want to find ‘value’, they simply want to invest in stocks that will deliver a significant positive overall return over time (capital growth and income, but mostly capital growth) with minimal to moderate risk.

What I will try to convey are a number of clear, logical and achievable processes, ideas and practices that will assist in discovering and profiting from small cap opportunities in the Australian market.

Coming briefly back to traditional 'value'. It is easy to find; any investor with a financial data source and rudimentary excel skills has the capacity to sort the universe looking for 'value criteria': a low PE (ignoring the negatives); a high dividend yield and perhaps, if they're feeling a little creative; an attractive EV/EBITDA ratio or a discounted Price/NTA ratio.

Unfortunately, this type of analysis, albeit fundamentally correct in many cases, is fraught with danger.

Looking for value invariably focuses the spotlight on the discounted stocks in the share-market; the oversold; the ignored; the disliked, distrusted and disappointed sectors of the market. Think of it as the discount or ‘sin bin’ end of the market. As a wise friend and mentor many years ago once told me,

"Good stocks aren't cheap and cheap stocks aren't good".

Efficient market hypothesis (EMH) states that stock market efficiency causes existing share prices to always incorporate and reflect all relevant information. So the value end of the market is reflecting all the negative current sentiment. So in its essence, it can often mean that "the crap has floated to the top".

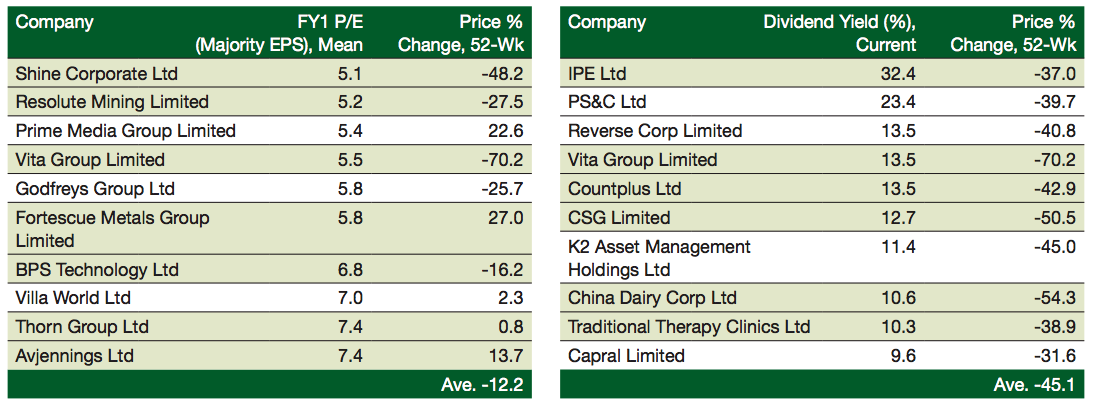

I've run a screen on the cheapest stocks in the market (on a prospective PE basis and dividend yield) and their respective 1-year performance. On this simplistic measure, the average fall over for the cheapest 10 stocks over the past 12 months has been -45% for the high yielders, and -12.5% for the low PE stocks.

Buying stocks because they offer 'good value' is simply a strategy one would only employ if they wished to reduce a capital gains tax bill!

So let's look at it a different way and throw the whole 'value' idea out the window. If we accept EMH then how do we best find those stocks that are likely to make you money?

Distilling our investment process into a simplified form, we aim to find (and invest) in companies that are likely to perform better than market expectations. If this occurs, regardless of 'value', these share prices almost invariably rise over time.

So here are 8 tips outside the basic financial investment fundamentals that I believe will help guide you to creating a well-positioned, defensive and profitable portfolio at the smaller end of the market:

1: Follow the momentum

We rarely buy stocks that are falling in price. More often than not (see EMH) falling share prices indicate there are integral problems or structural challenges with the company or the industry in which the business operates. Don't be afraid of buying a stock if it's cresting a record high. As a rule at Cyan we do not buy stocks if they've fallen to a record low and rarely buy into shares that are in a downward trend. It sounds simplistic, and in many ways it is, but this simple rule has saved us from countless historical losing positions. The only time we overlook this rule is when there has been a material change to a business; new management team, a capital raising providing a growth catalyst, an attractive acquisition, or a competitor misstep.

2: Investigate (and invest) in what you understand

We never invest in biotechnology businesses or any business that we cannot understand. We avoid biotech because we don't have scientific backgrounds and do not understand the technology, science or have grasp of the opportunity or the industry, Fortunately (for us), there are no more than a handful of these businesses that have performed anywhere close to their initial promises and expectations. We also avoid the resources sector because we are not confident in predicting the macro-economic drivers of underlying commodity prices. All this is not to say significant returns cannot be generated from investing in these industries. Just be humble enough to recognize what you feel you can understand and have some hope of predicting.

3: Utilise anecdotal evidence

One of the advantages of investing in the Australian stock market is that you can be close to the action and have the ability to experience first-hand the performance of certain businesses. For instance one of the most successful businesses for us recently has been the payments processing technology company, Afterpay (ASX:APT). Both in store and online it has been evident that this business is gaining significant traction in the retail space. Our anecdotal evidence (friends and family using and recommending the Afterpay system) has further strengthened our positive view of the performance of the company, in addition to the information that has been released to the ASX. Whether it’s in the retail space, financial services, infrastructure, food, healthcare or real estate, don't discount the value of your own experiences with listed companies.

4: Relentlessly follow cash flow

"Revenue is Vanity. Profit is Sanity. Cash is Reality." Without doubt, the most valuable financial report released by companies to investors is the cash flow statement. Even better, are the quarterly 4C statements, for companies that are required to report them (typically for newer loss-making businesses where more than half of the entity’s tangible assets are in cash). The cash flow statement gives complete transparency as to revenue run rate, company expenses and cash backing. They can be a clear indication as the true cash profitability of a business, or for those in earlier stages of their lifecycle, if or when a company might be required to raise capital. The cash flow statement is the very first thing we look at in a company’s financial report.

5: Beware the Executive Chairman

We find there's a fine balance between a healthy level of company ownership by management and too much. Often that manifests itself in the title of Executive Chairman. If an individual owns a high percentage of the company then that influence should be mitigated by an independent and non-executive chairman. The EC role tends to shout the word, "Minority Shareholder".

6: Be dynamic

It is nice in theory to buy shares at their lowest price and sell them at the very top. We all seem to have one friend or colleague that does that regularly. The fact is that it’s impossible to get anywhere close to that over a cycle. We aim, over time, to buy parcels of shares as we become increasingly confident in a business and sell them either as the price increases or be we lose confidence in a company. Over a 2 year holding period, we will make regular changes to our target weightings of any specific company relative to our overall portfolio.

For instance we bought into Bellamys (BAL:ASX) at listing at $1, saw it rise to over $15 and sold out the last of our stock at $8.30. Over that 18 month holding period we changed our weighting in the company on more than 30 occasions. Of course not all those trades were profitable but over time we did well for our clients. Think of an investment like sailing a yacht, even if you set off in the correct direction, you always need to be vigilantly watching for changed conditions and always need to trimming the sails and altering your course.

7: Understand the conflicts of interest in broker research

Here’s how the system works:

If an analyst puts a ‘Buy’ on a company it has the following consequences:

- A ‘Buy’ rating potentially appeals to every client, those that own the stock and those that don’t. Hence the broking house is more likely to write more business in the stock with a ‘Buy’ rating.

- It keeps the company happy.

- It encourages the company to engage the broking house in corporate services.

If an analyst puts a ‘Sell’ on a company it:

- Is only of interest to owners of that stock (unless it can be shorted). Hence the ‘Sell’ recommendation is likely to only generate limited business.

- Often upsets existing holders of the stock (who don't want to see a negative view being circulated).

- Upsets the company itself which is therefore less likely to engage the house in further corporate work.

So the moral of the story is, although sometimes the content is an excellent source of information, pretty much ignore analyst recommendations (and sometimes even the valuations).

8: Have humility and never cross your fingers

Invariably investments fail to perform to expectations. Certainly one of the aspects of stock-market investing that we believe private investors do most poorly is selling. Whenever a business or company disappoints us we immediately take action to sell our position in that company, REGARDLESS OF PRICE. There are over 2000 companies listed on the exchange and we never feel that we need to be backing companies that disappoint. Just as you would never return to a restaurant that served you a bad meal we never return to disappointing businesses.

It takes a certain self-assurance to admit you’re wrong and take a loss, but this is a crucial part of the process. The philosophy of “I'll cross my fingers and hope this gets better over time” is one reason why part-time investors' portfolios do not perform as well as they should. Don’t be scared about booking an immediate loss when something goes wrong. Believe me, things usually get worse. And from a taxation perspective, a realised capital loss holds more value than an unrealised loss.

Summary

So investing in the small end of the market is not easy. There are no algorithms or systems or rules or gurus or books that can guarantee you winning. It’s not a part-time job. It takes common sense and humility and confidence and hard work.

Good luck.

Originally published on the Australian Shareholders Association website.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Dean has over 25 years experience in the funds management industry covering all major asset classes. He holds as Master of Applied Finance and is a Graduate of the Australian Institute of Company Directors.

2 stocks mentioned

Dean has over 25 years experience in the funds management industry covering all major asset classes. He holds as Master of Applied Finance and is a Graduate of the Australian Institute of Company Directors.

Expertise

Dean has over 25 years experience in the funds management industry covering all major asset classes. He holds as Master of Applied Finance and is a Graduate of the Australian Institute of Company Directors.

Expertise

Comments

Comments

Sign In or Join Free to comment