A quick-take on Passive QT

As expected (by me and pretty much everyone else) the Fed held interest rates unchanged and announced that it would commence its balance sheet normalization plan in October. The balance sheet normalization plan involves gradually ceasing reinvestment of principal from maturing bonds, and will result in a passive/automatic run-down of the Fed's asset holdings from the large scale asset purchase programs aka Quantitative Easing or QE. This is a monetary policy tightening measure, hence my calling it Quantitative Tightening or QT - specifically passive QT. For clarity, active QT would involve the outright selling of asset holdings - an unlikely course of action.

Note: the Fed basically recognizes that this is a tightening measure as they have noted that balance sheet normalization will be deactivated and full reinvestment of principal will recommence should economic conditions deteriorate. In other words, the balance sheet remains an important and actively used part of the monetary policy tool kit for managing the cycle in both directions.

As I have previously noted, this move is US dollar positive, and bearish for bonds, and will at the margin tighten financial conditions, and by definition will present a headwind to stocks. The initial market reaction reflects this view and is more or less as expected. Thus I retain a bearish bias on bonds, bullish tactical view on the US dollar, and underweight view on US equities (in preference of global/emerging markets).

The charts...

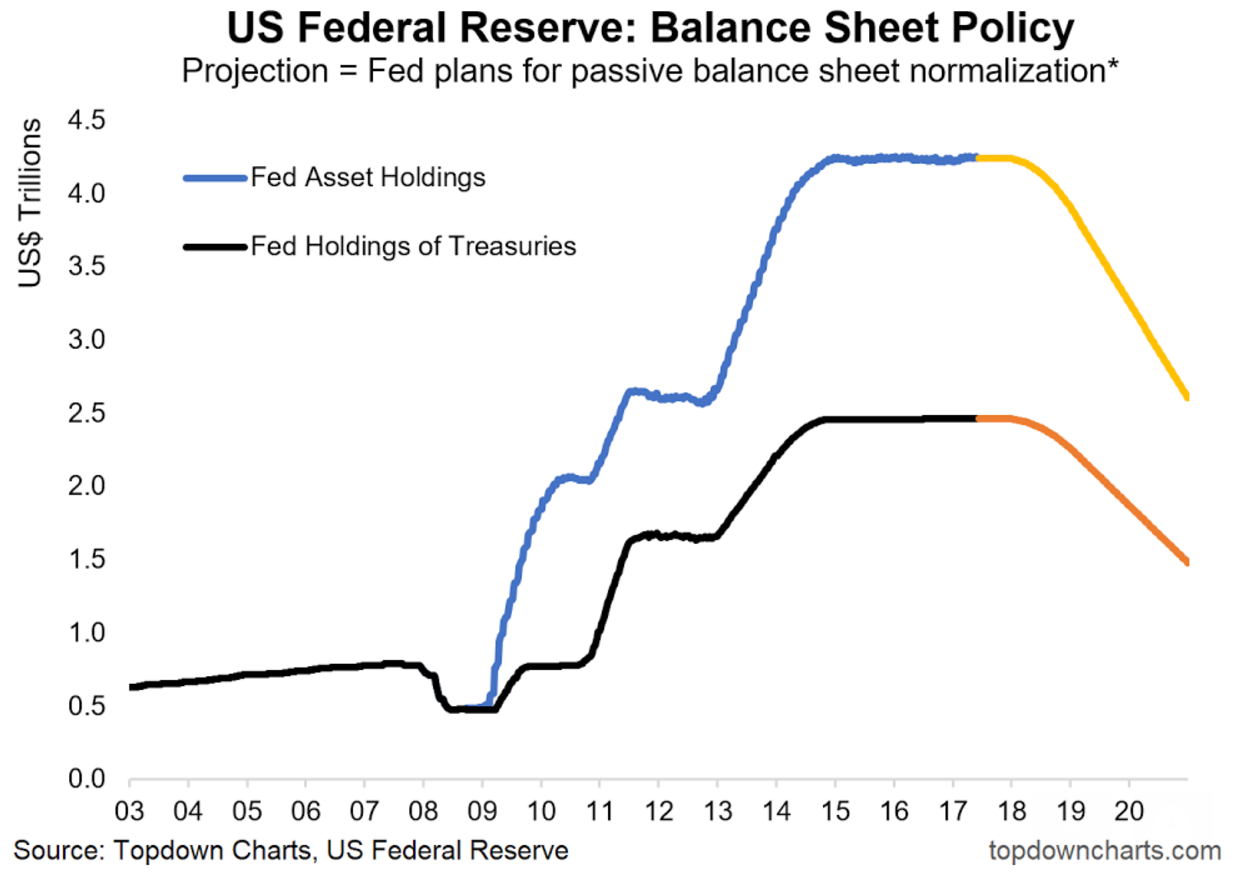

This chart shows the projected Fed balance sheet run-down based on the caps of reinvestment cessation ($10B per month initially, rising to $50B per month ongoing in 12 months time). Note: the Fed has mentioned it will recommence reinvestment if the economic outlook warrants (i.e. this is a tightening measure and can be reverted to an easing measure if needed).

Initial market reaction to the announcement: stocks down, bond yields up, US dollar up (all makes sense).

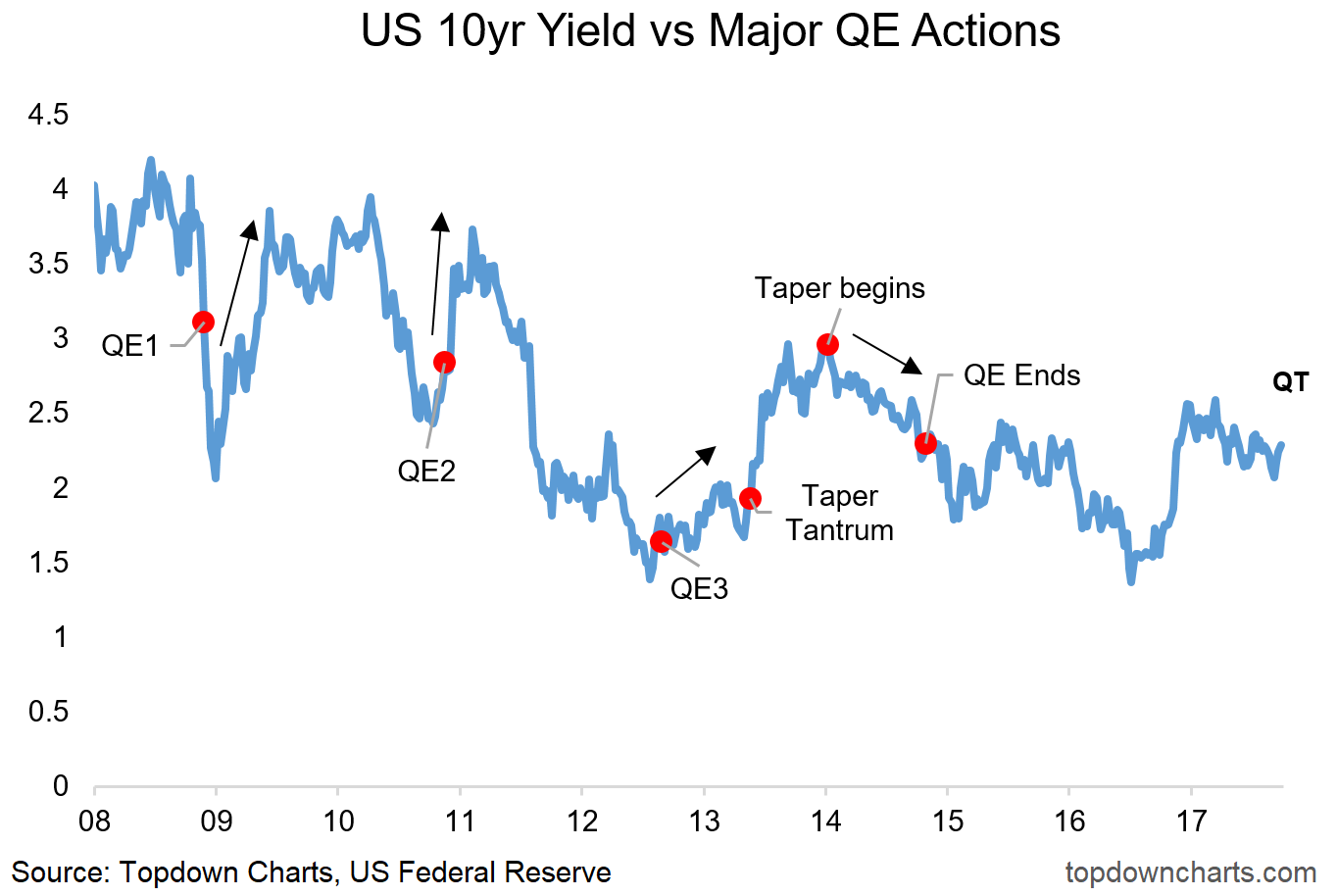

Here's the history of the US 10-year bond yield vs some of the major QE actions and announcements. The experience has been that QE announcements often coincide with market bottoms, whereas the actual commencement of taper coincided with a top in yields. QT could have a counter-intuitive impact of resulting in lower bond yields if it resulted in materially tighter financial conditions and slowed growth/inflation expectations.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Callum is Head of Research at Topdown Charts.

Topdown Charts is a chart-driven macro research house covering global Asset Allocation and Economics.

5 topics

Callum is Head of Research at Topdown Charts. Topdown Charts is a chart-driven macro research house covering global Asset Allocation and Economics.

Expertise

Callum is Head of Research at Topdown Charts. Topdown Charts is a chart-driven macro research house covering global Asset Allocation and Economics.

Expertise

Comments

Comments

Sign In or Join Free to comment