Is Telstra good value after its dip?

Telstra (TLS) is not high on the list of businesses we would most like to own. Having said that, it is not a terrible business, and at the right price it makes sense to own it, particularly given its steady dividend stream. So, with TLS’s share price down around 20 percent over the past year, we decided to assess its value.

One of the appealing features of TLS is its stability. Over many years, the company has delivered consistent revenues at consistent margins for consistent earnings. On the face of it, this should allow us to value the company fairly readily.

However, for several reasons the future for TLS looks different to the past: Firstly, migration to the NBN will take a large bite out of TLS’s fixed-line business, offset somewhat by a series of one-off and recurring payments it will receive from NBN Co. for handing over its copper and HFC networks. Secondly, there is the matter of TPG Telecom (TPM) planning to become Australia’s fourth mobile network operator.

Given this, we think it makes sense to split the valuation into four components:

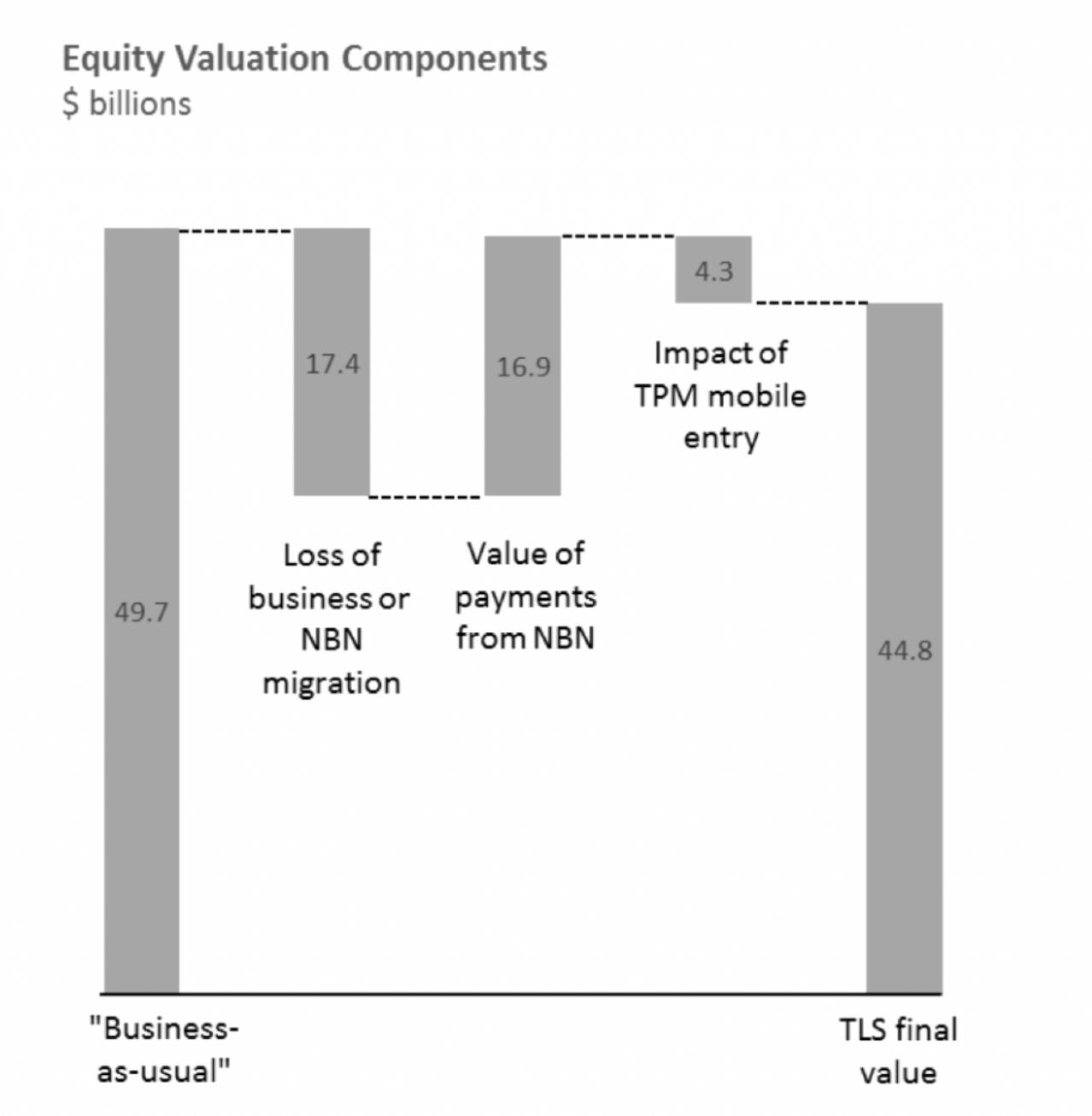

A “business-as-usual” valuation of TLS based on historical financial metrics;

A valuation of the earnings “hole” left by the migration to NBN;

The present value of payments TLS will receive from NBN Co; and

An adjustment for the impact of increasing competition in mobile.

We consider each of these in turn.

“Business-as-usual”

As noted above, TLS has historically been a very stable business, and the “business-as-usual” valuation is a relatively straightforward extrapolation of historical financials. Using an 8% cost of capital and a 1.5% p.a. growth rate, we arrive at an estimated value of just under $50 billion for the equity in TLS, or around $4.20 per share.

NBN earnings hole

We then come to the NBN earnings hole. TLS has provided guidance as to the EBITDA impact it expects when the migration is complete, and our “business-as-usual” valuation gives us an implied EBITDA multiple with which we can capitalise this impact. We estimate that this amounts to a fairly meaningful $17.4 billion of equity value, equivalent to around $1.46 per share.

Payments from NBN Co.

Happily, this earnings hole is largely compensated for by one-off and recurring payments it expects to receive from NBN Co. TLS has provided estimates of the value of these payments, but we believe the discount rate applied to these payments should be lower than the one TLS has used (which is generally 10%). We have evaluated TLS on the basis of an 8% WACC, and we see these payments as having somewhat lower risk than the overall TLS business, and so we apply a 7% discount rate. On this basis, we estimate the value of payments yet to be received from NBN Co at around $16.9 billion after tax – a larger figure than quoted by TLS, and one that substantially makes up for the value lost from TLS’s fixed line business.

Increasing competition

Finally, we consider the impact of TPM’s entry into the mobile market. As a point of reference, we note the impact of the 2012 entry into the French market by low-cost operator, Free mobile. In that example, ARPUs for the leading player, Orange, declined by 10-15% over several years, as the new entrant moved to take market share of 15%.

This sort of outcome would imply a very material loss of value for TLS. However, for a range of reasons, we expect TLS to experience a less dire outcome. These reasons include:

Free benefitted from a roaming agreement with Orange. However, the ACCC has indicated it does not support roaming in Australia. This is an important constraint on TPM which plans to spend relatively little on its network build and will achieve relatively limited population coverage;

Approximately 53% of TLS mobile subscribers are outside the major cities, and therefore less vulnerable to competition, as TPM focuses its network spend on the major cities;

A large part of TLS’s mobile revenues are derived from business subscribers, who would also be less susceptible to a TPM offering; and

Across its entire customer base, TLS maintains a price premium position in the Australian market due to perceptions of coverage and quality. TPM’s low-cost offering will more directly impact Optus and Vodafone (and is thought to potentially be a strategy to pressure Vodafone into a consolidation).

Our valuation of Telstra

Taking these factors into account, we anticipate a couple of percentage points of lost market share for TLS, and perhaps a 5% decline to ARPUs. On this basis, we estimate that the value of TLS falls by around $4.3 billion, or around $0.36 per share – still a material impact.

We then assemble the different valuation components into an overall picture, as follows, to arrive at an estimated value for TLS equity of around $44.8 billion, which equates to around $3.77 per share.

Against today’s share price of $4.42, this makes TLS look around 15% expensive, although it should be noted that we consider large sections of the Australian equity market to be expensive, so this conclusion perhaps comes as no surprise. It is also worth noting that different judgements around discount rates might lead other analysts to a different conclusion.

The Montgomery Alpha Plus Fund – which is fully-invested and uses a machine learning model analysing many different variables to drive investment decisions – holds a modest position in TLS in its long portfolio. For the Montgomery Fund, however, we are particular about valuation and are happy to hold cash when value is scarce. Accordingly, TLS does not find its way into our long-only funds at the current price, regardless of its dividend-yielding appeal.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tim Kelley has retired from Montgomery Investment Management, effective 30 September 2021. Tim’s final project has been drafting our investment guidelines to integrate environmental, social and corporate governance (ESG) considerations into our investment process. Tim remains a shareholder of Montgomery Investment Management.

1 stock mentioned

Tim Kelley has retired from Montgomery Investment Management, effective 30 September 2021. Tim’s final project has been drafting our investment guidelines to integrate environmental, social and corporate governance (ESG) considerations into our...

Expertise

Tim Kelley has retired from Montgomery Investment Management, effective 30 September 2021. Tim’s final project has been drafting our investment guidelines to integrate environmental, social and corporate governance (ESG) considerations into our...

Expertise

Comments

Comments

Sign In or Join Free to comment