An extraordinary clash of conditions in investment markets

Investment markets have a host of both positive and negative factors fighting for supremacy. The real question is whether central banks and governments will engineer a continued suspension of capitalism. I was sceptical six months ago. I'm less sceptical now that capitalism will return anytime soon. On balance, however, there is still plenty of room for caution.

Short-term government policies to suspend capitalism (increased hurdle for bankruptcies, mortgage holidays, eviction moratoriums, banks not recognising bad debts, etc.) have morphed into medium-term policies. And, it is hard to see any government ready to exit. There is a quiet extension to each policy that lapses.

We took advantage of pre-election weakness to increase our risk exposure a little. But given the rise in markets since the election, the positive factors have mostly been reflected already. And, the positive factors tend to be short-term, the negative aspects tend to be medium-term.

Key positive factors for share prices

- Government stimulus: Global governments continue to add stimulus. The US has some question marks, and the stimulus won't be as large as if Biden won Senate majority. But it would seem additional stimulus is highly likely.

- Low probability of US tax hikes: Subject to the Georgia senate run-offs, it looks unlikely the US Senate will pass Biden's company tax rate increases. If passed, these would have reduced US earnings by around 10%.

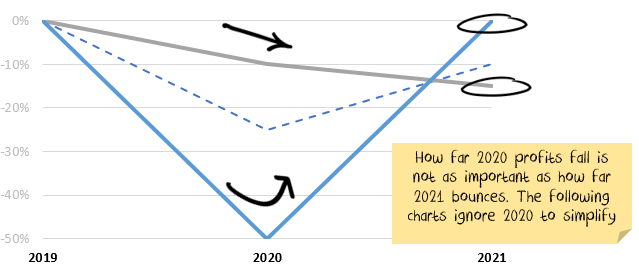

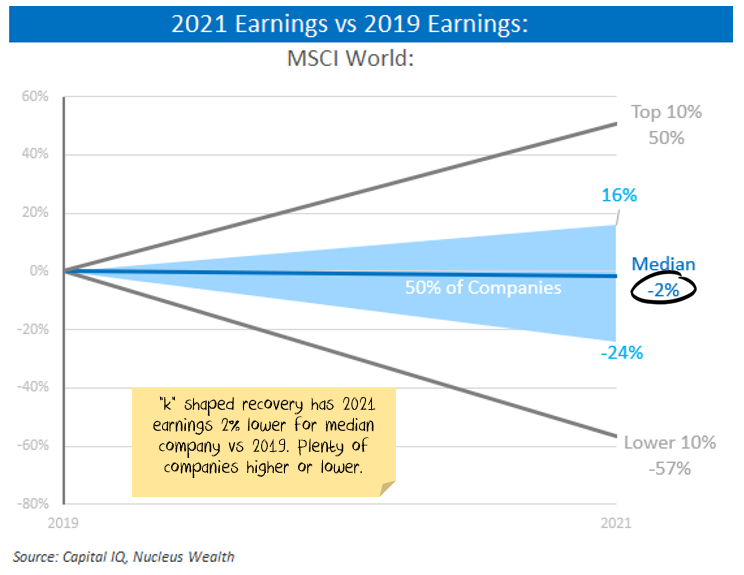

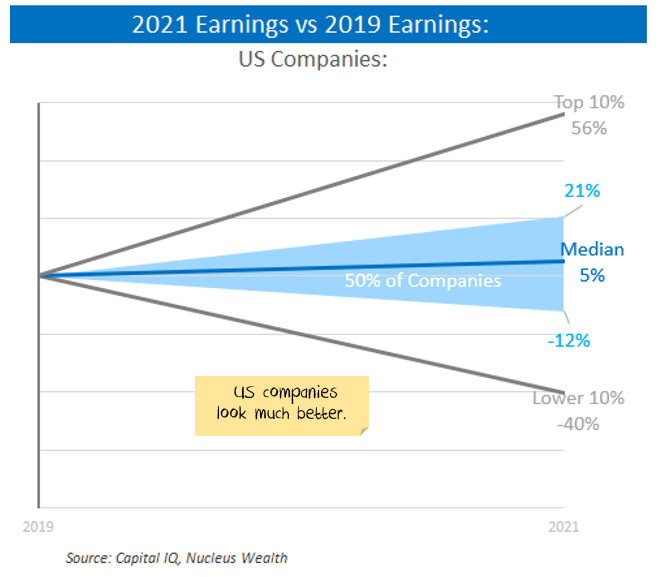

- Earnings very good: 3rd quarter earnings were much better than expected. Analyst forecasts haven't changed much, but that is better than usual! Typically, later year forecasts are far too optimistic and get revised down as they get closer. Forecast growth is 24% for 2021 and then 15% for 2022.

- Inequality to remain high: No changes to taxes in the US = economic inequality likely to remain high. In Australia, there are tax cuts for the rich, reduced support for the poor. Travel limitations depressing spending for the rich. Plus stimulus tends to be relatively indiscriminate; some ends up in the right hands, some in the hands of those that don't need it. Net effect: the rich have more money to put into investment markets.

Other positive factors for share prices

- Bankruptcies, evictions limited: in many countries bankruptcies are down 30%+, driven by a mix of stimulus and rule changes. Businesses feel richer if they haven't had to write down bad debts. Not fixing the problem, just delaying the pain.

- Mortgage repayment holidays: as above.

- Wage growth very low: helpful to company profits.

- Productivity: forced change/digitisation often results in better outcomes. Having to fire staff usually results in the least productive going first, increasing overall company productivity.

- Low oil prices: keeping transport costs down.

- Vaccine hope: successful trials give hope to an end of the virus.

- Policy certainty: President Biden is far less likely than Trump to be unpredictable.

Key negative factors for share prices

- COVID in the Northern Hemisphere: It is ripping through populations. Importantly, hospitals are reaching capacity, which means lockdowns have begun again in Europe and seem highly likely in the US.

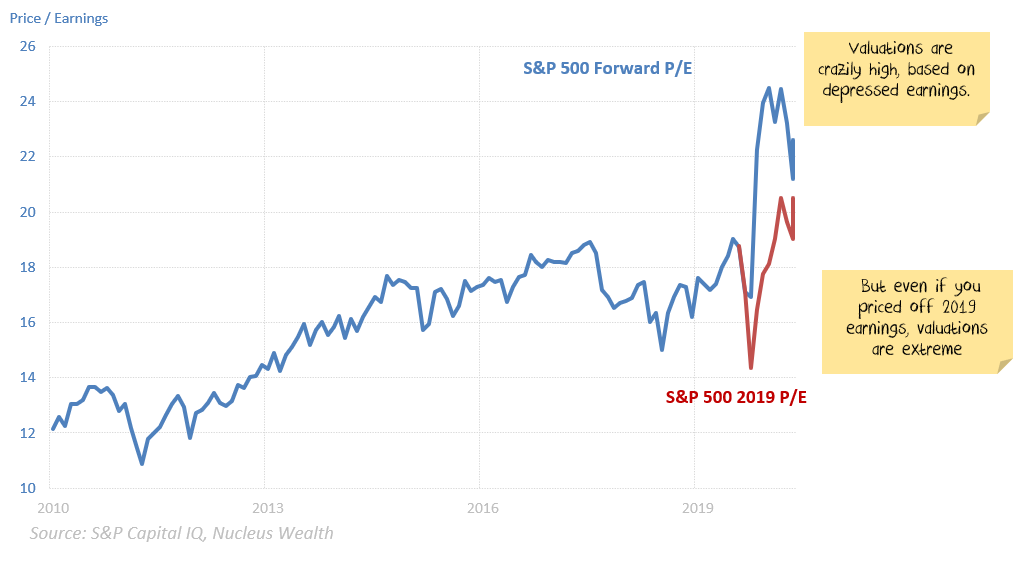

- Valuation: Share market valuations are extraordinarily high.

- Latent bankruptcies: Changing the rules so that companies and individuals who are otherwise bankrupt are allowed to increase their debt does not fix the problem. It also runs the risk that the bad actors not paying their bills start to pull down the good actors.

- Low genuine credit growth: credit growth has been poor; banks are still tightening lending standards. But the credit growth also includes mortgage holidays. And companies borrowing to survive rather than to make productive investments. Which means genuine credit growth is lower than the already weak headline numbers. Economic growth has been tied at the hip to credit growth for the last decade. It is difficult to see what will replace easy money as the only thing holding economic growth up.

Other negative factors for share prices

- Short term gap in US economic conditions: There may not be stimulus until Biden takes power. If so, there are three months with limited government support while the virus sets new records. This might be enough to tip the economy into a funk and result in more job losses.

- Inequality longer-term effects: the short term effect of increased inequality increases savings and investment and (probably) increases stock market valuations. The longer-term impact is depressed demand and profits. And more political upheaval.

- Australian stimulus badly targeted: supply-side rather than demand-side.

- Structural change: leading to weak demand, higher unemployment. There are industries like travel and tourism which will have to deal with lower sales and employment. The means job losses continue as former employees have to give up on finding a job and retrain for a new industry.

Net effect

It bears repeating: the positive factors for investment markets tend to be short-term, the negative ones medium-term. Will there be "clear air" for a few months before the consequences begin? Maybe. The stock market has had a lot thrown at it and is still holding up.

On the flip side, the risks are not symmetrical. The upside appears more limited than the downside.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Damien runs asset allocation and global stock portfolios for Nucleus Super, Nucleus Ethical and Nucleus Wealth. His 25 year+ career includes Global Quant at Schroders, Strategy at Wilson HTM & co-founder of Aegis.

........

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd - AFSL 515796.

5 topics

Damien runs asset allocation and global stock portfolios for Nucleus Super, Nucleus Ethical and Nucleus Wealth. His 25 year+ career includes Global Quant at Schroders, Strategy at Wilson HTM & co-founder of Aegis.

Expertise

Damien runs asset allocation and global stock portfolios for Nucleus Super, Nucleus Ethical and Nucleus Wealth. His 25 year+ career includes Global Quant at Schroders, Strategy at Wilson HTM & co-founder of Aegis.

Expertise

Comments

Comments

Sign In or Join Free to comment