An investor's guide to good government stimulus

We are in a strange political environment. Globally there have been trillions of dollars of government stimulus announced, deficit hawks have turned chicken, and formerly staunch opponents of government intervention have been leading the charge. How should investors assess each government stimulus announcement?

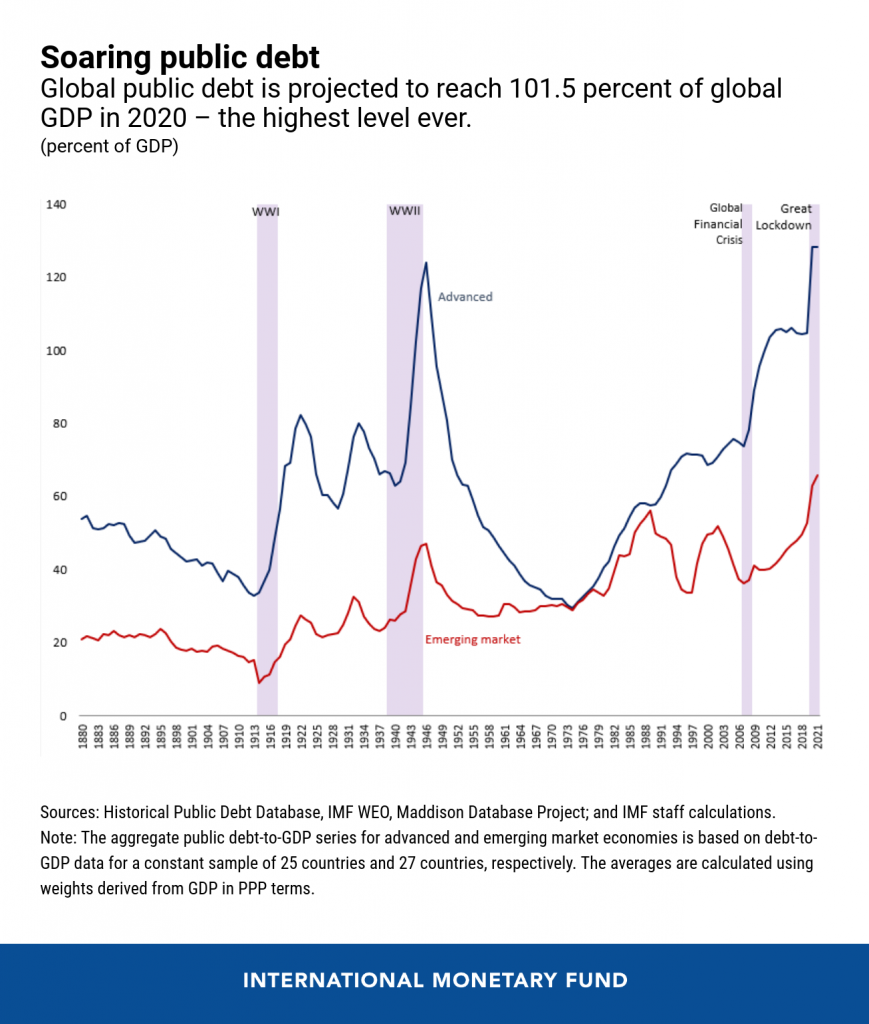

One day the Australian government told us they had the right level of stimulus. The next they announced a miscalculation by a cool 3% of GDP but assured the public that the new level was also correct.

Which begs the question: in today's world, is government stimulus ever wrong? Surely moar stimulus good / less stimulus bad for investment markets is too simple. Although some days it doesn't seem like it.

There are a few different frameworks investors should examine stimulus through:

Government stimulus effect on factors of production

First, I want to take you back to the OG economists, Adam Smith, Ricardo, Marx. Let's use a restaurant as an example of how they examine the factors of production:

- Land: the lease on the building

- Capital: Loans for the fit-out of the restaurant, or to the building owner to purchase the property.

- Workers: the waiting staff and chefs in the restaurant

- Entrepreneurs: the owner of the restaurant that took the economic risk to put it all together.

I'm going to extend this further. Let's say we live in a country with only four industries: a factory, a restaurant, a bank and a grocery store. And coronavirus hits. The restaurant is deserted and running at a loss, with the owner staring at bankruptcy.

The question is, who is going to bear the brunt of the economic pain?

- Land: The restaurant could have a considerable rent reduction. The downside is that the landowners will suffer, and might go bankrupt. But even if they do, another landowner would step in (at a reduced price), and our overall economy would still be OK with everyone employed. i.e. bad for an individual landowner, OK for the economy.

- Capital: The restaurant could stop paying interest to the bank and maybe write down some debt. The downside is the bank will suffer, and won't lend to others. But again the immediate economic impact is relatively low if most remain employed.

- Workers: We can fire a bunch of workers in the restaurant. The downside is that with no money, the workers don't spend on goods from the factory and reduce their grocery spend. Because of this, the factory has the same problem, and need to lay off staff. Which results in even less demand for the restaurant and the grocery store and a negative economic spiral ensues.

- Entrepreneurs: We could send the owner bankrupt. The problem here is you might end up with no restaurant, all of the workers fired and the same issues as above. The landlord is stuffed: it might be years before another entrepreneur opens a new restaurant. Plus our factory workers, grocers and bankers now have nowhere to eat out. And restaurants don't own many assets, and so the banks might not get much back.

Net Effect: Through this lens, the government stimulus targeted to help entrepreneurs and workers at the expense of capital and land will be less disruptive. I'm not making a moral judgement here about who "should" bear the pain. Just about which government policies and stimulus will have a more effective short term economic impact.

Demand-side or supply-side government stimulus

Government stimulus can target additional supply or target demand.

For example, subsidising a new factory or worker salaries, cutting taxes or regulation tend to be supply-side reforms. In particular, China has launched a number of these programs.

On the other side, demand-side involves more significant government consumption and income support for citizens.

The world is severely lacking demand. So, supply-side stimulus is not going to have the same impact, except indirectly by employing more people.

The other problem that supply-side stimulus creates is more trade tension. Say China subsidises the manufacture of more toasters through a mix of underpriced infrastructure, tax cuts and regulation. But there is reduced demand in China, and so these toasters need to be sold overseas. When the US government sends a cheque to an unemployed US citizen who uses it to buy a new toaster from China, the US has effectively subsidised a Chinese job. The US would much prefer their stimulus to be spent on a US toaster made by a US worker. And so China's supply-side stimulus is likely to see trade tensions escalate.

Net effect: to fight the coronavirus impact, demand-side stimulus is better than supply-side. With the caveat that supply-side will work if you can "steal" demand from other countries.

Governments: Adapting or clinging to the past

It was eminently reasonable for governments to put into place policies to "tide things over" for a few months in case there really was a V-shaped recovery. But these policies become self-defeating quickly.

Take, for example, the analysis above suggesting that keeping entrepreneurs afloat is a good policy. Many governments have suspended insolvency laws in some form which helps in the short term. But if this gets extended for too long, then it quickly becomes a more significant issue as moral hazard takes root. Say we have an industry with nine honourable retailers and one dishonourable retailer being supplied by six honourable suppliers:

- In a normal scenario, if the dishonourable retailer stops paying its supplier, the supplier takes it to court. The retailer either pays or is wound up.

- But now that isn't an option, and the dishonourable retailer can keep racking up bills, maybe even cycling through suppliers, not paying and not being able to be prosecuted.

- Some of the suppliers (being honourable) might even declare bankruptcy because of the non-payment while the dishonourable retailer stays afloat.

- This can then "infect" the other retailers who lose their suppliers.

- The one dishonourable retailer might have infected half of the industry by the time it is wound up.

Net effect: policies that help people and companies adapt to the new economic reality are good. Systems that try to maintain the old economy may have been helpfully initially, they no longer are.

Government Stimulus effect on Inequality

Economic inequality was already reaching relatively extreme levels in many countries. Coronavirus shutdowns are increasing that difference. Many lower-paying jobs cannot be performed from home, plus casual workers were the first to lose their jobs.

Central bank bond-buying leads to more inequality. It is up to governments to reverse this through stimulus.

If they don't, the greater economic inequality will lead to the election of increasingly extreme politicians and demagogues, promising snake oil solutions to the masses.

Investor Wrap up

It is time to move on. New policies are needed that assume the virus is with the world for an indefinite period. Investors should factor in low growth if tax cuts and supply-side stimulus dominate. And investors should also factor in increasing trade tensions.

The initial policy dump by governments and central banks was, for the most part, quite effective but focused on short term fixes. Economists and investment markets widely lauded these policies. The most significant growth risk is if politicians simply extend the short term policies, particularly the rules around insolvencies.

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Damien runs asset allocation and global stock portfolios for Nucleus Super, Nucleus Ethical and Nucleus Wealth. His 25 year+ career includes Global Quant at Schroders, Strategy at Wilson HTM & co-founder of Aegis.

........

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd - AFSL 515796.

5 topics

Damien runs asset allocation and global stock portfolios for Nucleus Super, Nucleus Ethical and Nucleus Wealth. His 25 year+ career includes Global Quant at Schroders, Strategy at Wilson HTM & co-founder of Aegis.

Expertise

Damien runs asset allocation and global stock portfolios for Nucleus Super, Nucleus Ethical and Nucleus Wealth. His 25 year+ career includes Global Quant at Schroders, Strategy at Wilson HTM & co-founder of Aegis.

Expertise

Comments

Comments

Sign In or Join Free to comment