Apple Caps off the Resilience of US tech

Michael Smith

Kauri Asset Management

It was a prospect that seemed all but unimaginable just a few weeks ago. Amid what is shaping to be the greatest downturn since the Great Depression, the US market has staged an unlikely rally, with the S&P 500 up 30% from its recent low.

We believe this is due in no small part to the heavy lifting of the market’s tech giants, which are the same band of stocks that underpinned a multi-year bull run. Look no further than the NASDAQ, which overnight was still within an inch of where it finished 2019. You’d be mistaken for thinking there wasn’t an economic crisis on our hands.

Yet it is the resilience of the US tech sector, where the five largest companies make up 20% of the entire S&P 500, that we believe can be attributed to the marked ‘distortion’ between the state of the broader economy and the recent performance of the stock market.

There is one thing the tech sector has on its side in the current climate – each of the key stocks are leveraged to an online world that we are now even more dependent on.

Apple rounds out the tech heavyweights

We expected Apple (NASDAQ: APPL) to be hit hardest of any tech major heading into results, with the global pandemic weighing on its manufacturing supply chain and dampening consumer demand.

As the Coronavirus escalated in China, Apple cut its prior guidance. In recent days, it also announced production delays for its flagship iPhones set later this year.

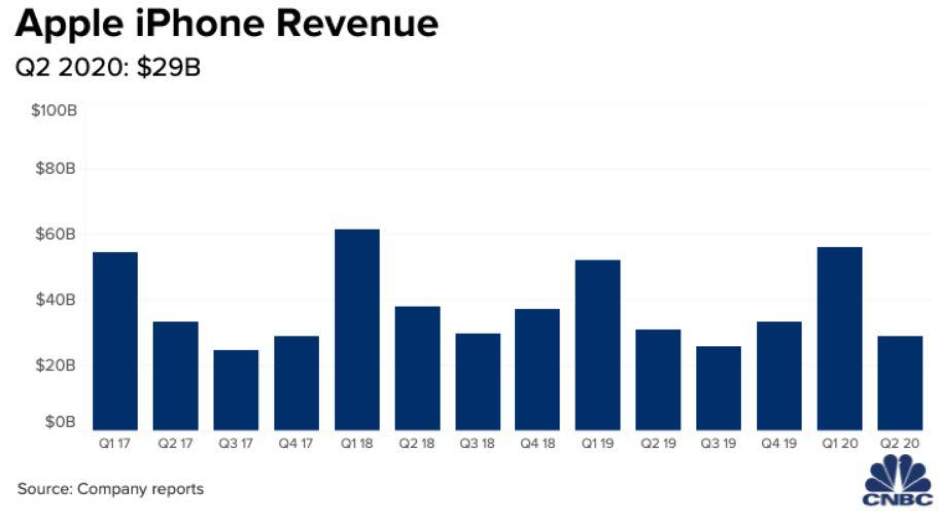

We consider these points are reflected in the company’s results, where iPhone revenue dropped 7% year-on-year to US$28.96 billion.

Source: CNBC

However, services revenue is playing an ever-increasing role, jumping 16% to US$13.34 billion. This includes sales from Apple Music, iCloud, Apple+ and the like. This was complemented by Wearables, Home and Accessories, where sales grew 22.5% to US$6.28 billion. We believe both are providing somewhat ‘defensive’ sources of revenue as consumers stay at home.

At a group level, earnings were US$2.55 per share, while revenue totalled US$58.3 billion. Both of these metrics were higher than the market’s expectations for EPS of US$2.26 and revenue of US$54.54 billion.

While opting not to issue a third-quarter guidance, Apple CEO Tim Cook left some room for optimism, stating that the steep drop in February “began to recover some in March, and we’ve seen further recovery in April”. We believe an increase in the company’s buyback program and dividend also align with the company’s expectation for a rebound.

Broad-based tech revenue remains resilient

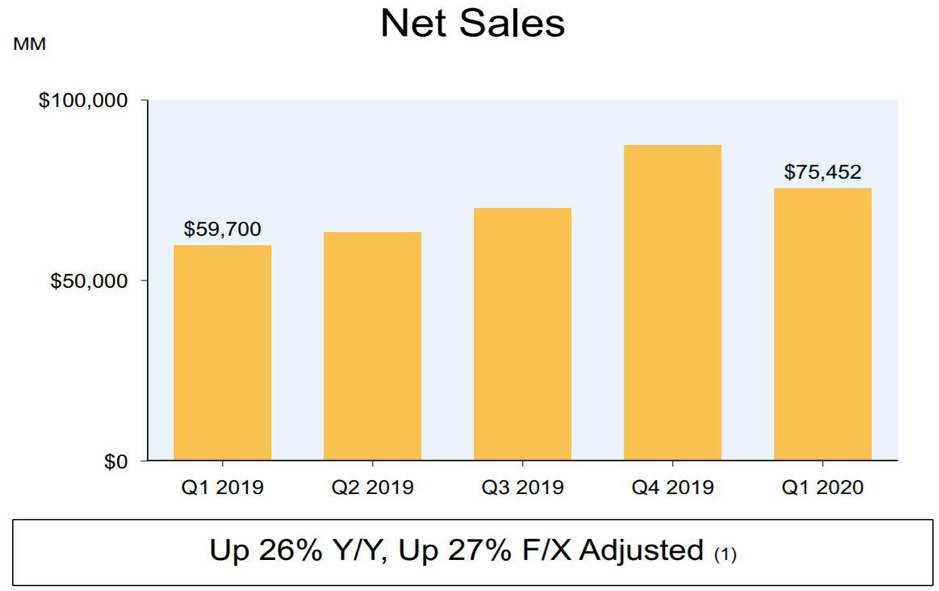

We considered that Amazon (NASDAQ: AMZN) would be one of the biggest beneficiaries of a transition to the digital economy. Largely, that showed up through above-forecast revenue of US$75.45 billion, and its Amazon Web Services division surpassing US$10 billion in revenue for the first time.

However, earnings were below forecast at US$5.01 per share, with the entirety of its US$4 billion operating profit set to be allocated to Coronavirus expenses like employee virus testing. We consider the defensiveness of the underlying business remains strong, offset by abnormal expenses.

Source: Amazon Company Presentation

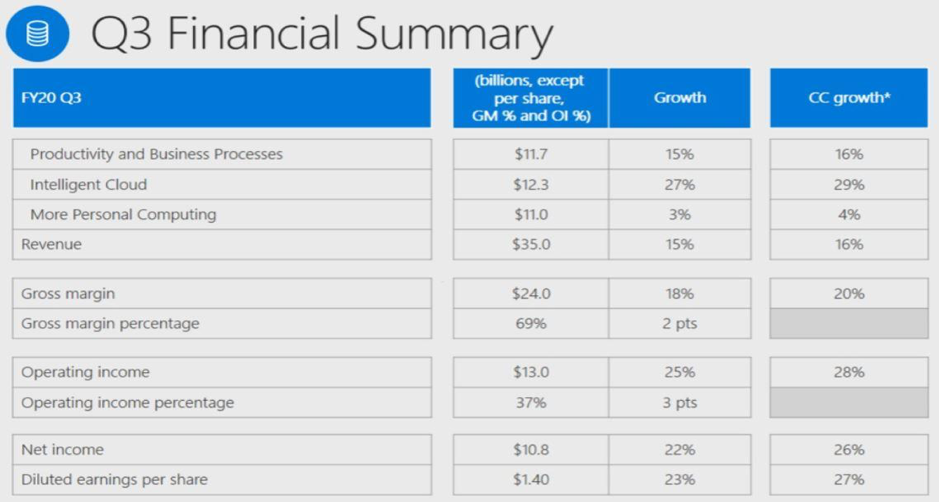

In the case of Microsoft (NASDAQ: MSFT), the tech giant delivered an out-and-out beat. Revenue jumped 15% to circa US$35 billion, which was nearly 4% better than consensus forecasts. EPS came in at US$1.40, an 11% beat.

Although LinkedIn is a drag on performance, the increasing necessity of the cloud is underpinning growth. Microsoft’s intelligent cloud business unit grew revenue by 27%, with its lucrative Azure division seeing sales climb 59%.

All the while, consumer and business demand has remained robust as end-users shift to remote work, play and learning. The company is even going it alone with plans to increase capex spending this quarter to cope with demand, a positive sign in our view.

Source: Microsoft Presentation

Meanwhile, Alphabet (NASDAQ: GOOGL) grew Q1 earnings from US$6.66 billion to US$6.84 billion but missed forecasts. Revenue after removing traffic-acquisition costs proved far more resilient, increasing from US$29.48 billion to US$33.7 billion, beating the market forecast of US$33.32.

In addition, the company’s outlook offered some cautious hope, with Alphabet CFO Ruth Porat noting “some very early signs of recovery in commercial search behaviour by users”. YouTube revenue grew 33%, while the company’s cloud business held its 52% growth rate from the prior quarter, something we believe is fundamental to the company’s earnings trajectory.

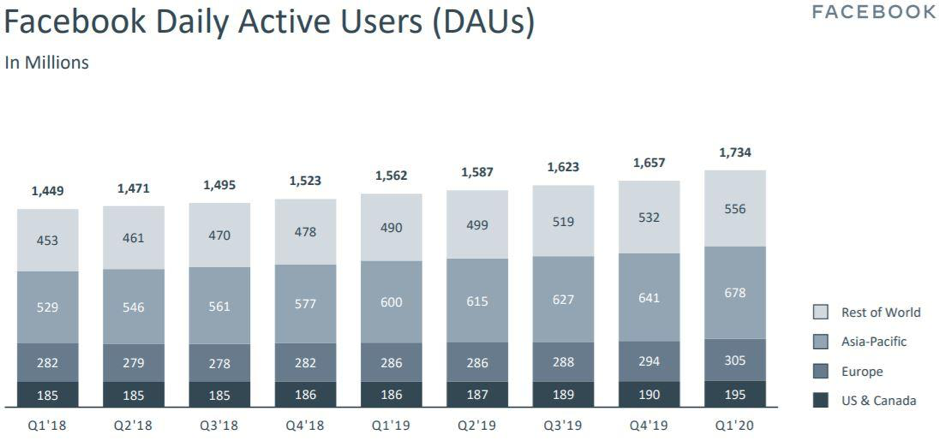

It was a similar story for Facebook (NASDAQ: FB). While the company more than doubled profits year-on-year to US$4.9 billion, it missed earnings forecasts. But the strength again rested in better-than-expected revenue, which rose 17% to US$17.74 billion.

Like Alphabet, however, amid the uncertainty it reported “signs of stability [in advertising revenue] reflected in the first three weeks of April”. We view the company’s strongest daily active user (DAUs) growth in years as a bright spot offering Facebook the prospect of a fast rebound once advertising activity accelerates out of the downturn.

Source: Facebook Presentation

Elsewhere, the likes of Tesla (NASDAQ: TLSA), which delivered a first-quarter profit for the first time, as well ServiceNow (NYSE: NOW) and chip-maker Qualcomm (NASDAQ: QCOM) all delivered results that we believe were better than expected.

In the case of Qualcomm, the company was another to voice the possibility of some positivity ahead, reporting that demand in China, the world’s largest market for smartphones, was said to be nearing a return to ‘normal’ levels.

Final thoughts

Apple’s results this morning cap off what we believe are signs of resilience in the tech sector. These are businesses that we see as best-equipped to withstand the COVID-19 crisis, such that they can continue to outperform on account of their large balance sheets and business models that align with tailwinds in cloud computing, communication, online shopping and more.

At the same time, however, we believe the market’s upbeat response to earnings this week should still sound some caution for investors. In our view, commentary that suggests diminishing consumer activity is ‘moderating’ or ‘stabilising’ means expectations have been set higher.

While none of these companies are ‘cheap’ by any sense of traditional valuation methods, we do see in times like these why they each command a market premium.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

With over 15 years of experience within the financial services industry, Mike possesses an outstanding acumen and extensive insight when it comes to global equity markets and a range of financial services products.

5 topics

Michael Smith

Managing Partner

Kauri Asset Management

With over 15 years of experience within the financial services industry, Mike possesses an outstanding acumen and extensive insight when it comes to global equity markets and a range of financial services products.

Expertise

Michael Smith

Managing Partner

Kauri Asset Management

With over 15 years of experience within the financial services industry, Mike possesses an outstanding acumen and extensive insight when it comes to global equity markets and a range of financial services products.

Expertise

Comments

Comments

Sign In or Join Free to comment