ASX 200 to rise, James Hardie's earnings beat + Morgan Stanley's reporting season picks

Get up to date on overnight market activity and the big events for the day.

ASX 200 futures are trading 29 points higher, up 0.40% as of 8:20 am AEST.

S&P 500 SESSION CHART

MARKETS

- S&P 500 +0.90%, Nasdaq +0.61%, Dow +1.16%, Russell 2000 -0.01%

- S&P 500 finished higher, near best levels and around 2% off recent highs

- Financials, Industrials, Real Estate and Healthcare led to the upside

- Tech underperformed as Apple (-1.7%) and Tesla (-0.95%) lagged

- Utilities was the only sector that finished lower

- No major directional drivers in play – Ahead of US inflation data

- Morgan Stanley's Wilson says fiscal tightening a risk for US stocks, potential for disappointment on sales growth (Bloomberg)

- Morgan Stanley warns of hit to equity valuation if US fiscal spending is cut in wake of recent credit rating downgrade (Reuters)

- US institutional investors could face restrictions on owning Chinese stocks (Reuters)

- China stocks lose out as investors chase Japan stocks (Bloomberg)

CENTRAL BANKS

- Fed's Williams says central bank pretty close to peak rate (NY Times)

- RBA could hike one more time then begin cutting cycle in 2024 (Bloomberg)

- ECB rate hikes could trim 4.0% from Eurozone economic output (Bloomberg)

STOCKS

- Tesla CFO steps down; flags second transition for the position in four years (CNBC)

- Amazon will meet with Federal Trade Commission to avoid antitrust lawsuit (Bloomberg)

- PayPal launches PayPal USD, a cryptocurrency pegged to the US dollar (Bloomberg)

ECONOMY

- US corporate bankruptcies at highest level since 2010 (Reuters)

- German industrial production dropped more than forecast in June, now below pandemic levels (Reuters)

- China economists told not to be negative as rebound falters (FT)

-

China's exports likely contracted further in July, imports downturn seen slowing (Reuters)

DEEPER DIVE

Waiting for earnings resilience

The theater-minded amongst you will be familiar with Samuel Beckett's most famous play "Waiting for Godot". In case you've never seen the play, let me spoil it for you - Godot is the titular character who never turns up while his two connections Didi and Gogo discuss the issues of the day. In the context of financial markets, you could easily replace Godot with the word "recession". The most forecasted recession of all time still hasn't come, and the more it's forecasted, the more businesses and investors are able to prepare for whatever onslaught is coming.

And speaking of businesses that face recession, this week is week two of the August full-year earnings season. Week one was more or less muted (bar a disappointing miss from ResMed which sent shareholders to the exit door). But this season is going to be all about clarity - clarity on earnings, outlook statements, and equity market sentiment.

Morgan Stanley has a proprietary earnings sentiment indicator which has been used to identify which companies could deliver on its positive earnings guidance. Among large-caps, it nominates Origin Energy (ASX: ORG), Suncorp (ASX: SUN), and WiseTech Global (ASX: WTC). Among small-caps, they quote McMillan Shakespeare (ASX: MMS), AUB Group (ASX: AUB), and Karoon Energy (ASX: KAR).

Never miss an update

Get the latest insights from me in your inbox when they’re published.

Advertisement

And, as with any good indicator, the team also have a list of stocks that they believe will disappoint on market expectations. Among the large-caps, they nominate ASX (ASX: ASX), Bank of Queensland (ASX: BOQ), and Ramsay Health Care (ASX: RHC). In the small-caps, they nominate Aussie Broadband (ASX: ABB), Bapcor (ASX: BAP), and Seven West Media (ASX: SWM).

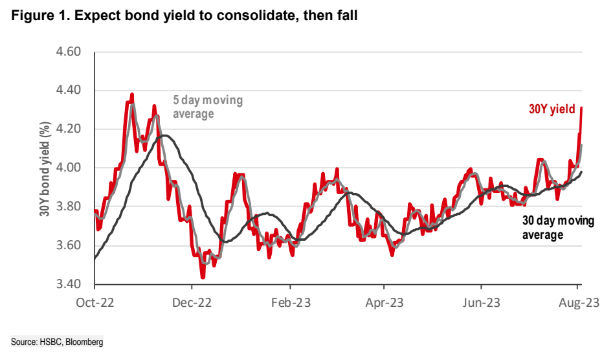

Chart of the Day

On the new edition of Signal or Noise, the most pertinent question we discuss is when the bond market's comeback will start. The assumption was based on the world returning to a more pre-2008 correlation where bonds go up and equities go down (and vice versa). For its part, HSBC believes that US long-end bond yields (i.e. assets which expire in many decades from now) will start to come good sooner rather than later. But first, they must go through a period of consolidation (which they say is happening now.)

Sectors to Watch

Major US benchmarks bounced as the market tries to consolidate on recent gains. Can the market establish a bit more 'right hand side' before trending higher? Or is this the beginning of a substantial correction? We'll find out more on Thursday after the all-important inflation print. As for sectors to watch:

SPDR Financial ETF (+1.4%): (This is basically the S&P 500 Financial sector) rallied strongly overnight. This could see some positive flow for local banks. Of note, a name like Commonwealth Bank is on a four day losing streak, down 3.8%. Heading into earnings season, Macquarie analysts are neutral on the sector with a preference of NAB over ANZ (in business banks) and WBC over CBA (in mortgage banks). As well as a preference for BEN over BOQ within regionals.

-

SPDR Homebuilders ETF (+1.16%): The Homebuilders ETF is up more than 30% since early April. It's pullbacks have been extremely shallow and its 0.3% off its recent high. Does this see more follow through strength for names like Boral, CSR, Adbri etc.

Its worth noting that James Hardie posted its first quarter earnings this morning (Earnings per share, revenue and Q2 guidance all ahead of analyst expectations)

Notable ETFs that rose overnight: US Jets (+1.03%), Cloud (+0.84%), Uranium (+0.76%)

Notable ETFs that eased overnight: Lithium & Battery Tech (-0.96%), Gold Miners (-0.78%), Rare Earths/Strategic Metals (-0.58%), Copper Miners (-0.15%)

KEY EVENTS

ASX corporate actions occurring today:

- Trading ex-div: None

- Dividends paid:None

- Listing: None

Economic calendar (AEST):

- 10:30 am: Australia Consumer Confidence

- 11:30 am: Australia Business Confidence

- 1:00 pm: China Balance of Trade

This Morning Wrap was first published for Market Index by Kerry Sun and Hans Lee.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire and Market Index's pre-opening bell news and analysis wrap. Available weekday mornings and written by Kerry Sun.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies (“Livewire Contributors”). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

12 stocks mentioned

2 contributors mentioned

Livewire and Market Index's pre-opening bell news and analysis wrap. Available weekday mornings and written by Kerry Sun.

Expertise

Livewire and Market Index's pre-opening bell news and analysis wrap. Available weekday mornings and written by Kerry Sun.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 stocks with massive growth runways

Livewire Markets