ASX banks ANZ, CBA, NAB, WBC still uninvestible say major brokers, but value is improving

A catch up on the latest upgrades, downgrades, and price target changes for ANZ, CBA, NAB, WBC & Co. The big brokers have been very busy!

The big banks. You love 'em, but the big brokers generally hate 'em.

You love them because they've paid steady and reliable fully franked dividends for as long as you've owned them (I'm guessing I've got a few veterans of several bear markets reading right now!), and you're not fussed about the fact that over that time your banks probably didn’t deliver the absolute best capital gains compared to other sectors. Opportunity cost? Meh! I only care about "income and stability" – and that's exactly what my big bank stocks have afforded me.

The brokers, on the other hand, tend to be less fussed about those bond-like income streams and stability, and more concerned about opportunity cost and valuations. To be fair, it's their job to advise their clients on these things, and therefore they tend to be less devoted to the big banks than your average mum and dad investor.

Which makes it super interesting when the broking community generally goes a bit sour on the banks. Despite their remonstrations about generational overvaluations (as in – many standard deviations from the mean), no doubt among mum and dad investors, the big brokers’ recent calls to sell Aussie bank shares have gone unheeded. Ho and hum!

In previous roles as portfolio manager and financial adviser, I too learned it was pointless to tell mum and dad investors to sell their bank shares. They only ever wanted to know which of the big banks they didn't already own had the best dividend yield, and therefore was the best one to buy!

Given there's been quite a bit of movement recently in terms of big brokers vs big Aussie bank shares, let's catch up on the latest upgrades, downgrades, and price target changes in the sector. As we'll see, the pullback in bank share prices has provided many brokers with an opportunity to tweak their ratings and price targets to look less at odds with the sector’s huge rally through 2024 (you can check how bearish they were in this review I did back in December).

Thank goodness for Trump’s trade war!

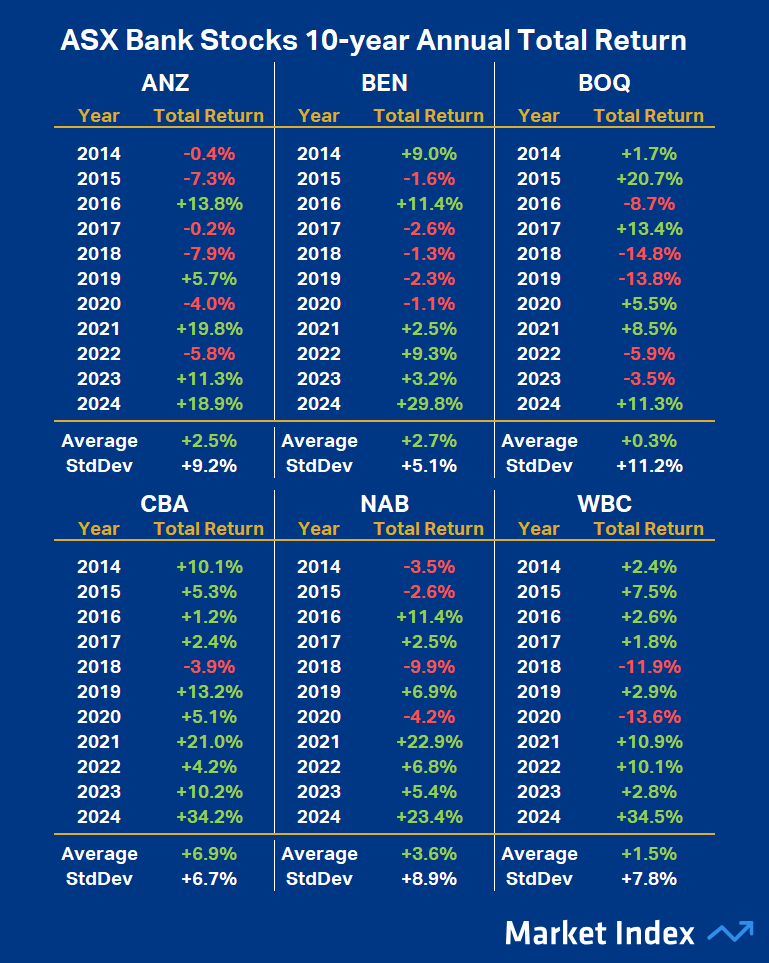

Prior to the recent market correction, the big ASX banks were flying. My own research in early December suggested that at the time, returns in the sector for 2024 were between roughly 2-5 standard deviations from the 10-year mean. That’s “usually won’t happen 95-99.97% of the time” sort of stuff!

ASX Banks Annual Performance 10 years to December 3, 2024. (click here for full size image)

{kind=link}

The big brokers were bearish on the ASX bank sector due to such a perception of overvaluation, with most citing abnormal demand-supply conditions as driving an unsustainable rally in bank share prices. At the approximate height of the rally in December last year, UBS noted that a combination of “animal spirits” and “flow-driven momentum” were to blame for high bank share prices, while blanket-sell-rated at the time Citi suggested earnings growth was “almost non-existent”.

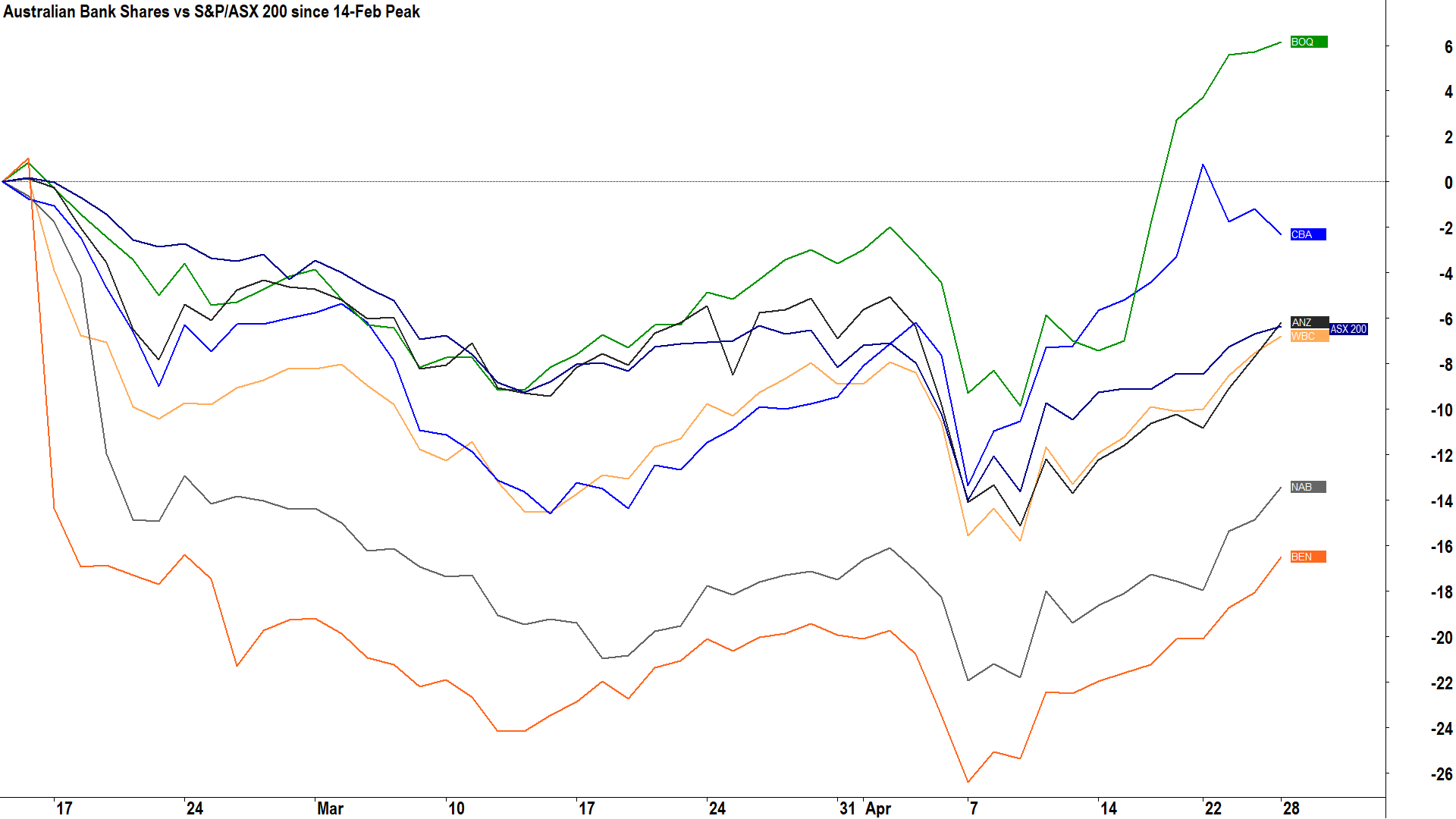

Fast forward to today, and many bank share prices have pulled back, with BEN and NAB the hardest hit, now trading 12-14% below their recent highs. BOQ and CBA are the only two banks to have notched a new high since the correction, and among the Big 4, CBA is the clear leader in terms of overall share price performance over the past 12 months.

ASX Banks Performance since the 14 February peak on the S&P/ASX 200 (click here for full size image)

{kind=link}

Note the chart above doesn’t include dividends, so the performances of CBA (ex-div 19-Feb, add approx. 2%) and BEN bank (ex-div 26-Feb add approx. +4%) improve modestly after accounting for ex-dividend and franking credit declines during the lookback period.

The recent correction, sparked by President Trump’s trade war, potentially allowed many brokers to claim victory in their fight against what they saw as crazy overvaluations in the ASX bank sector. As you’ll see, if facilitated several upgrades from SELL or sell-equivalents to HOLD or hold-equivalents, and there’s even the odd BUY or buy equivalent now creeping in.

Generally, price targets have also been ratcheted higher to more closely mark-to-market what were typically very low-ball assessments of value in the sector.

We’ll start with a look at each of the broker consensus updates for the big ASX banks, covering the latest ratings and price target changes since 14 February, i.e., the so-called Valentines Day Peak. Then, we’ll conclude by looking at a summary of the major broker updates across the sector.

Group 1 - The Big 4: ANZ, CBA, NAB, WBC

For all of the stocks covered, to obtain a Broker Consensus Rating, we assign a Rating Value of +1 to any broker rating better than HOLD/NEUTRAL/MARKETWEIGHT; a Rating Value of 0 for any broker rating equivalent to HOLD/NEUTRAL/MARKETWEIGHT; and a Rating Value of -1 to any broker rating worse than HOLD/NEUTRAL/MARKETWEIGHT.

We then take the average of all Rating Values and assign a Broker Consensus Rating of BUY to values +0.5 or above; a Broker Consensus Rating of HOLD for values between -0.5 and +0.5; and a Broker Consensus Rating of SELL for values -0.5 or below.

The Broker Consensus Target is simply the average of the target prices we have on file for each broker. Typically, brokers define their target price as a 12-month forecast, and each target price is based on a broker’s fundamental valuation assumptions. We have only assessed broker ratings and target prices within the last 3 months to account for recent relevance.

ANZ Group (ASX: ANZ)

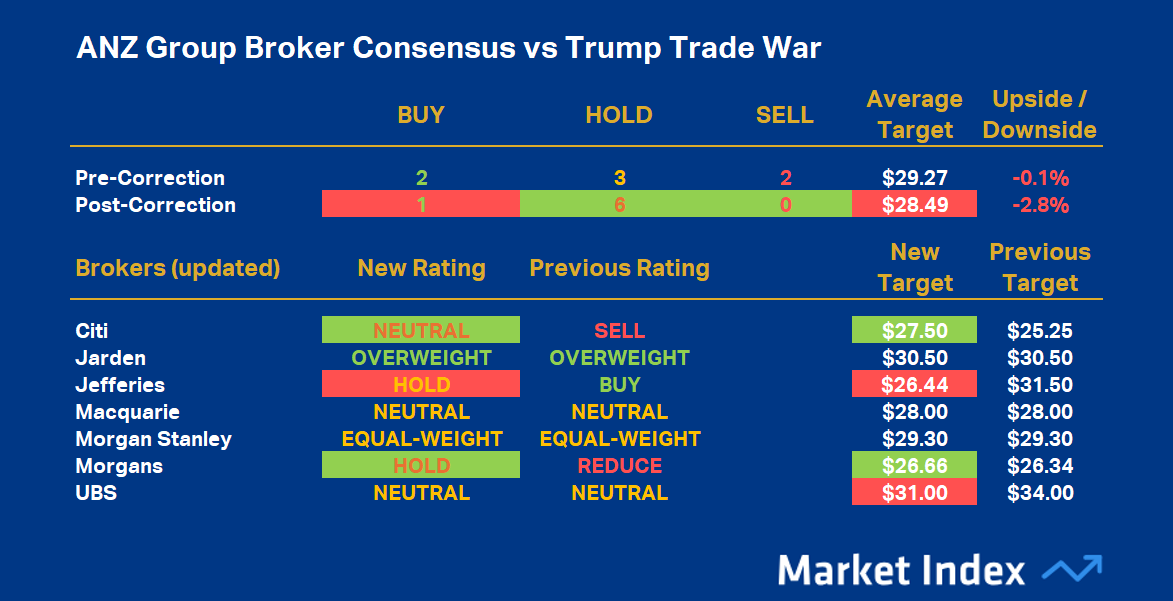

ANZ broker consensus table (click here for full-size image)

{kind=link}

ANZ’s average Rating Value is +0.14, resulting in a Broker Consensus Rating of HOLD. This is up from its prior average Rating Value of +0.00 and Broker Consensus Rating of HOLD.

ANZ’s Broker Consensus Target is $28.49 (down 2.7% from $29.27 prior to the 14-Feb peak in the ASX 200). This suggests brokers collectively believe the stock is around 2.8% overvalued based upon the closing price on Monday, 28 April of $29.31.

Commonwealth Bank of Australia (ASX: CBA)

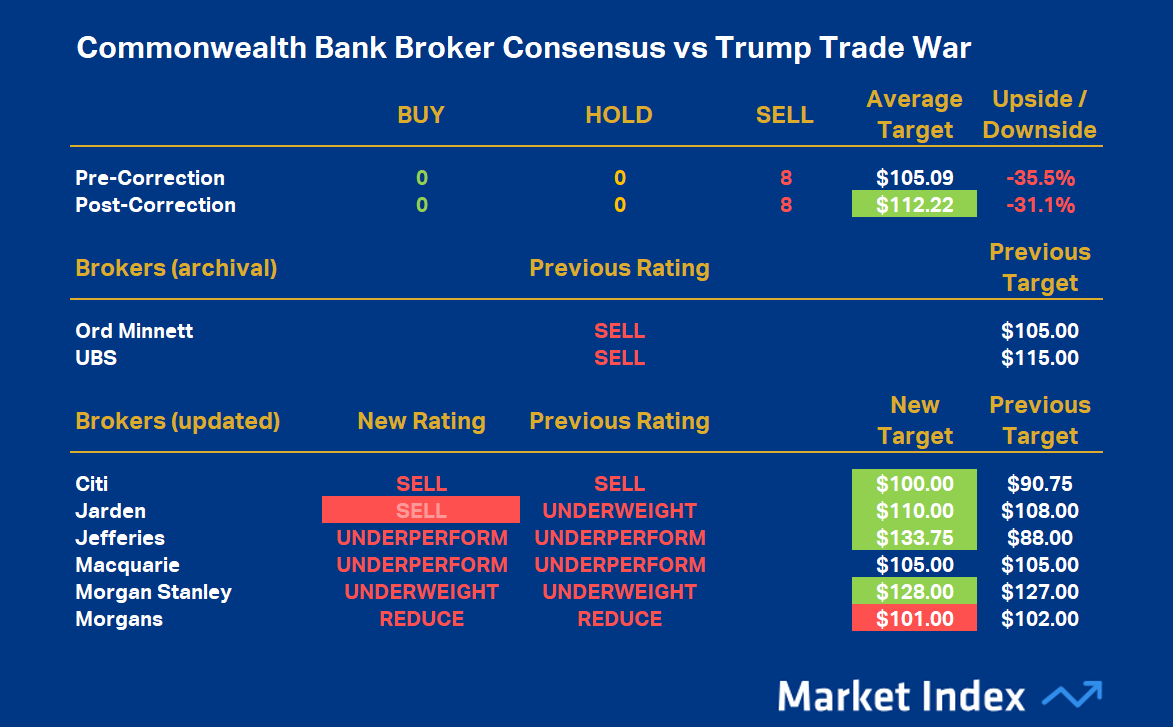

CBA broker consensus table (click here for full-size image)

{kind=link}

CBA’s average Rating Value is -1.0, resulting in a Broker Consensus Rating of SELL. This is unchanged from its prior average Rating Value -1.0 and Broker Consensus Rating of SELL.

CBA’s Broker Consensus Target is $112.22 (up 6.8% from $105.09 prior to the 14-Feb peak in the ASX 200). This suggests brokers collectively believe the stock is around 31.1% overvalued based upon the closing price on Monday, 28 April of $162.85.

Note however, if we only consider broker updates received since 2 April, CBA’s Broker Consensus Target rises further to $112.95 (30.6% overvalued), albeit with the same perfect SELL average Rating Value of -1.0.

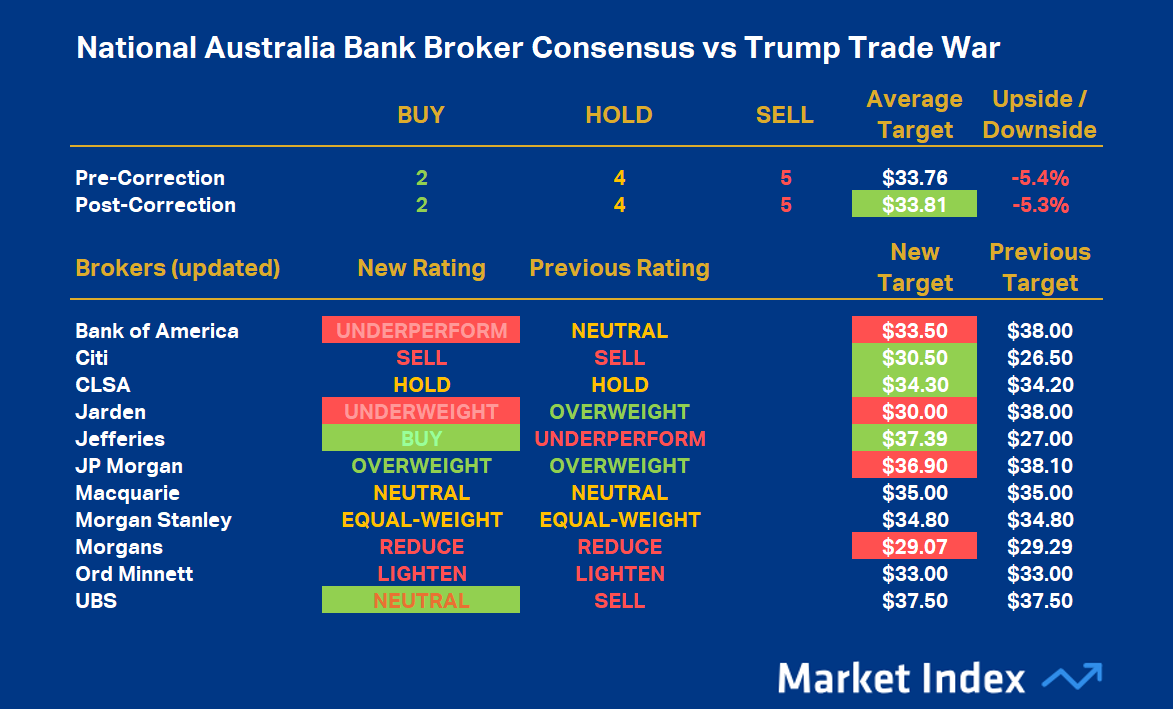

National Australia Bank (ASX: NAB)

{kind=link}

NAB’s average Rating Value is -0.27, resulting in a Broker Consensus Rating of HOLD. This is unchanged from its prior average Rating Value of -0.27 and Broker Consensus Rating of HOLD.

NAB’s Broker Consensus Target is $33.81 (up 0.2% from $33.76 prior to the 14-Feb peak in the ASX 200). This suggests brokers collectively believe the stock is around 5.3% overvalued based upon the closing price on Monday, 28 April of $35.70.

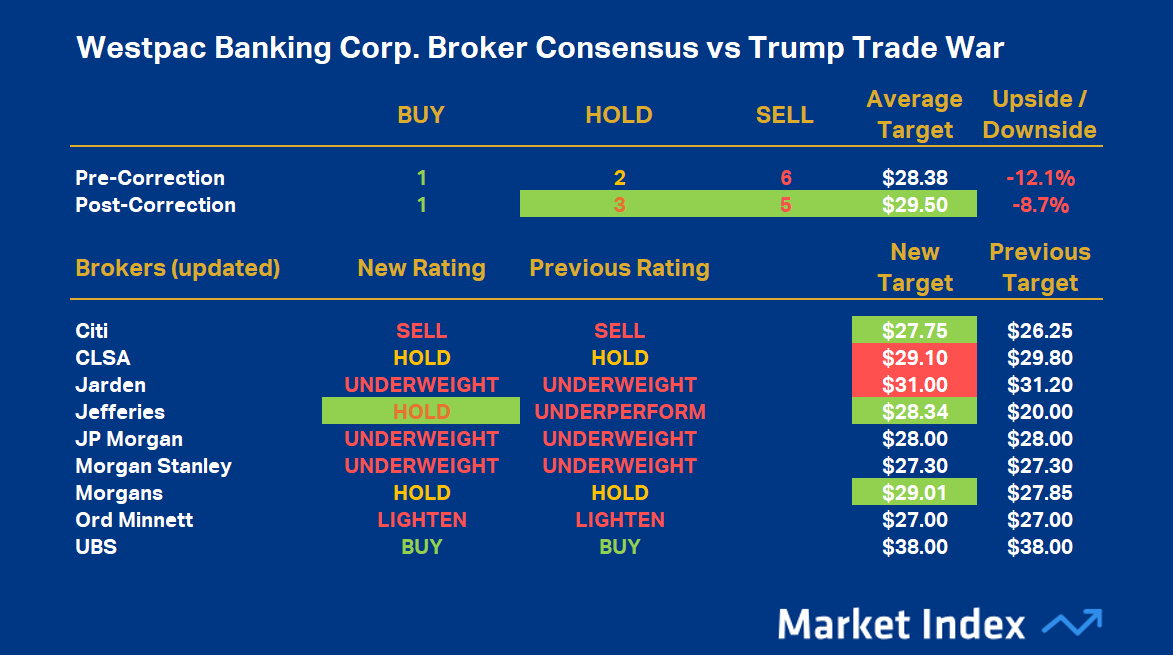

Westpac Banking Corporation (ASX: WBC)

WBC broker consensus table (click here for full-size image)

{kind=link}

WBC’s average Rating Value is -0.44, resulting in a Broker Consensus Rating of HOLD. This is up from its prior average Rating Value of -0.56 and Broker Consensus Rating of SELL – effectively a Broker Consensus Rating upgrade.

WBC’s Broker Consensus Target is $29.50 (up 4.0% from $28.38 prior to the 14-Feb peak in the ASX 200). This suggests brokers collectively believe the stock is around 8.7% overvalued based upon the closing price on Monday, 28 April of $32.30.

Group 2 - Regionals: BEN, BOQ

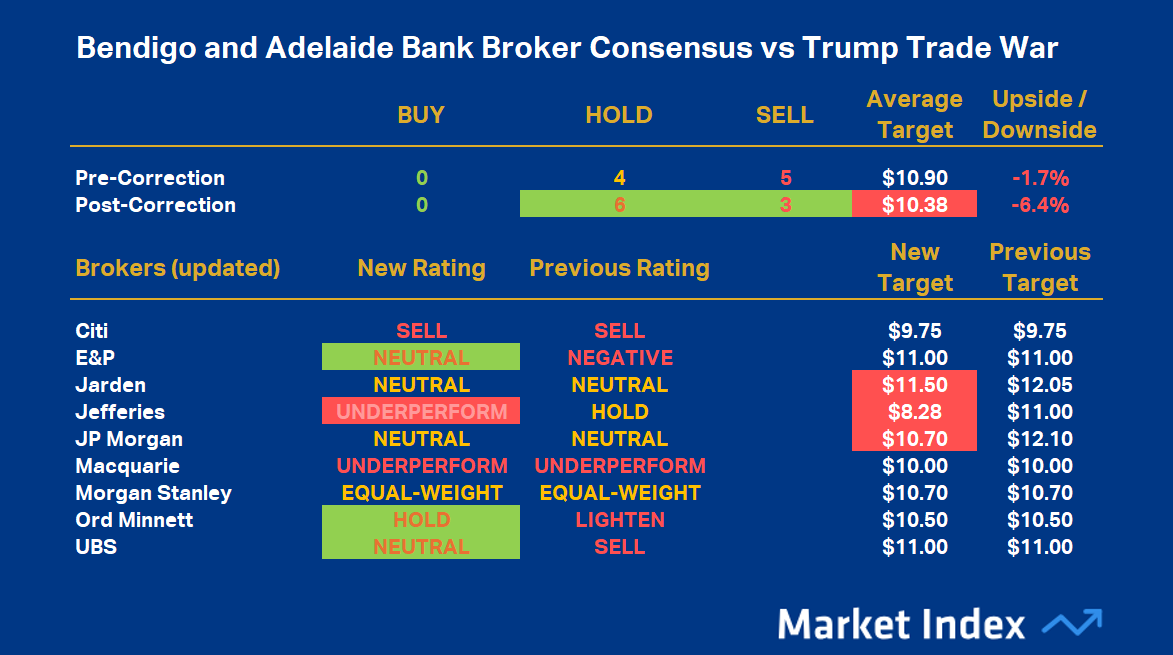

Bendigo and Adelaide Bank (ASX: BEN)

BEN broker consensus table (click here for full-size image)

{kind=link}

BEN’s average Rating Value is -0.33, resulting in a Broker Consensus Rating of HOLD. This is up from its prior average Rating Value of -0.56 and Broker Consensus Rating of SELL – effectively a Broker Consensus Rating upgrade.

BEN’s Broker Consensus Target is $10.38 (down 4.8% from $10.90 prior to the 14-Feb peak in the ASX 200). This suggests brokers collectively believe the stock is around 6.4% overvalued based upon the closing price on Monday, 28 April of $11.09.

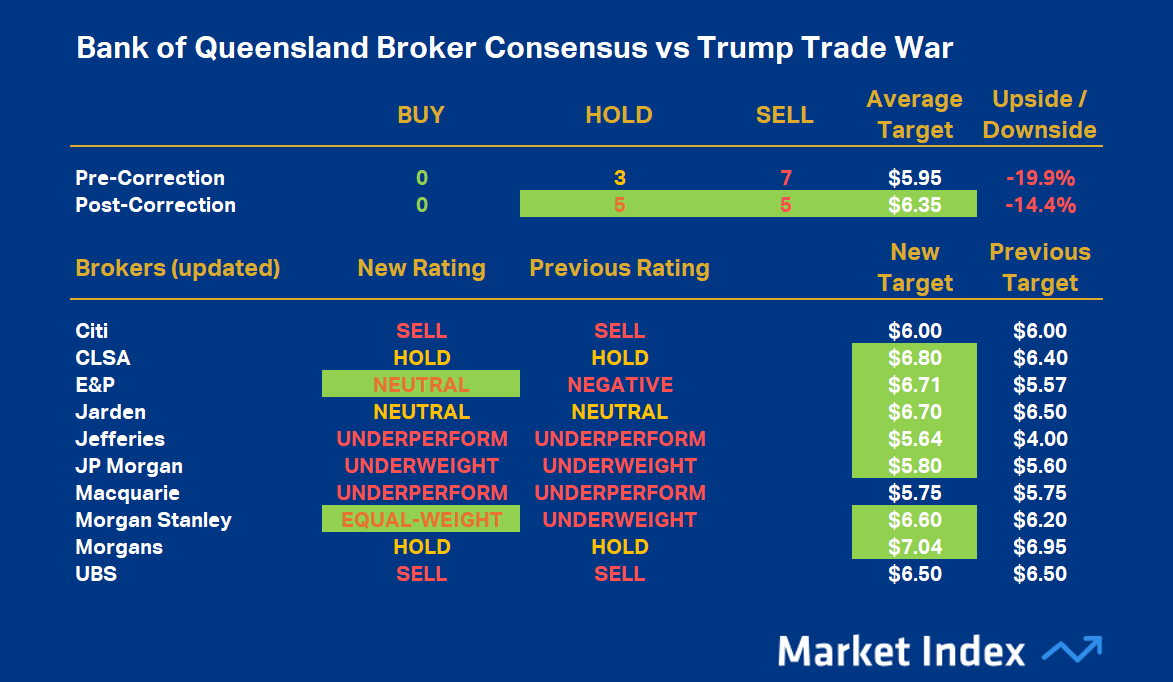

Bank of Queensland (ASX: BOQ)

{kind=link}

BOQ’s average Rating Value is -0.50 resulting in a Broker Consensus Rating of SELL. This is up from its prior average Rating Value of -0.70 and Broker Consensus Rating of SELL.

BOQ’s Broker Consensus Target is $6.35 (up 6.8% from $5.95 prior to the 14-Feb peak in the ASX 200). This suggests brokers collectively believe the stock is around 14.4% overvalued based upon the closing price on Monday, 28 April of $7.42.

Conclusions

The big brokers have done the analysis, they’ve tweaked their valuation models, and through their new ratings and target prices, we can get a better idea of the likely impact of the recent correction on ASX bank stocks.

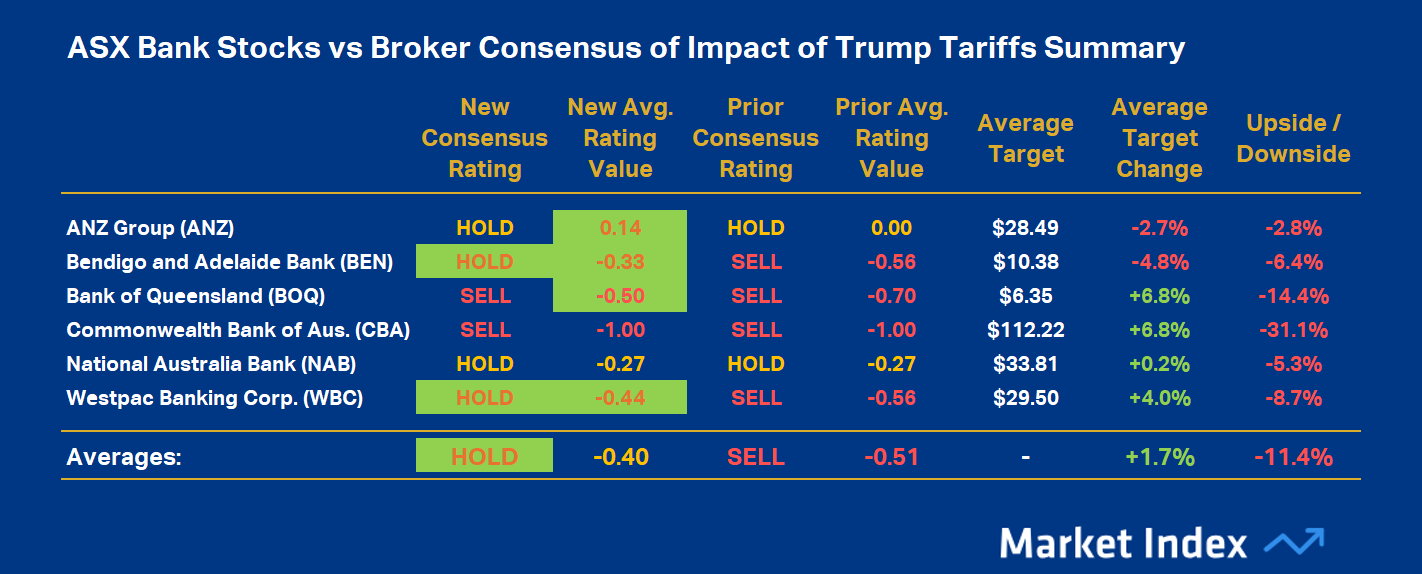

ASX broker consensus changes summary (since 14 February peak to Thursday 24 April) (click here for full size image)

{kind=link}

Generally, the brokers used the recent market correction as an opportunity to raise their ratings and price targets to more closely match current bank sector valuations, with target prices across the 6 major bank stocks covered here rising by around 1.7% on average. Ratings have also improved, with the sector average Rating Value rising to -0.40 from -0.51 – effectively a sector Broker Consensus Rating upgrade to HOLD from SELL.

Don’t forget that for most of 2024, broker ratings were collectively a SELL, and banks had their best year by several standard deviations from the mean. The slightly improved average Broker Consensus Target and average Broker Consensus Rating are hardly a glowing endorsement of newly perceived value in the ASX bank sector. On average, the big brokers still believe Aussie bank stocks are collectively 11.4% overvalued.

It's also worth highlighting specific winners, for example BEN and WBC, which each enjoyed Broker Consensus Rating upgrades (to HOLD from SELL). ANZ is the only major ASX bank stock to enjoy a positive Broker Consensus Rating (of +0.14, the equivalent of a HOLD).

CBA enjoyed the largest price target increase, which is possibly no surprise given the brokers were most collectively wrong with respect to its price target through 2024. Citi and Jefferies contributed the greatest proportion of average Broker Consensus Target increase here, with adjustments of +10.2% and +52%, respectively. Consider that Citi still believes CBA shares could drop by as much as 38% based on Monday’s closing price.

One could argue the brokers had it right – that at the depths of the correction, their bearish calls on ASX bank stocks throughout 2024 were vindicated. Certainly, it appears many of them used the recent correction to mark-to-market several arguably out-of-kilter-with-reality forecasts. Even so, if the latest consensus ratings and targets are anything to go by, the broking community still believes your investing dollar is better placed elsewhere. Aussie bank stocks remain a no-go zone 🚫.

Want to know which sectors the brokers collectively feel are cheap – as in 50-60% undervalued and in some cases more? Check out these two recent massive Brokers vs ASX Sector Reviews we did recently:

Brokers vs ASX Mining Stocks like BHP, RIO, FMG, MIN, PLS, IGO, SFR and more…

Brokers vs ASX Energy Stocks like WDS, STO, KAR, BOE, PDN, WHC and more…

This article first appeared on Market Index on Tuesday 29 April 2025.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

Never miss an update

Get the latest insights from me in your inbox when they’re published.

5 topics

6 stocks mentioned

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

This recently triggered market signal has never failed to predict gains

Ophir Asset Management