Australia victim of containment success: it may have massively over-stimulated and needs to exit fast...

Australia's exceptional efforts in flattening the COVID-19 curve quickly and crushing viral transmissions means that we may be a victim of our own success. The government's fiscal stimulus may have been calibrated for a situation that is much worse than the one we face.

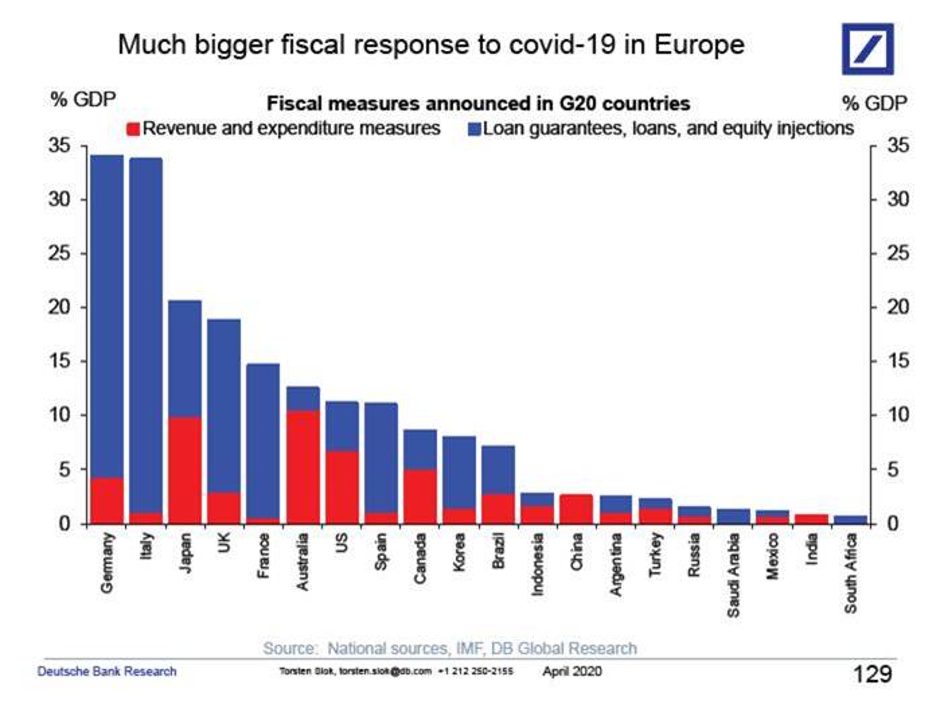

New analysis presented by Deutsche Bank economist Torsten Slok shows that amongst the 20 countries he examined, no nation has provided more fiscal support as a share of GDP than Australia in revenue and expenditure terms.

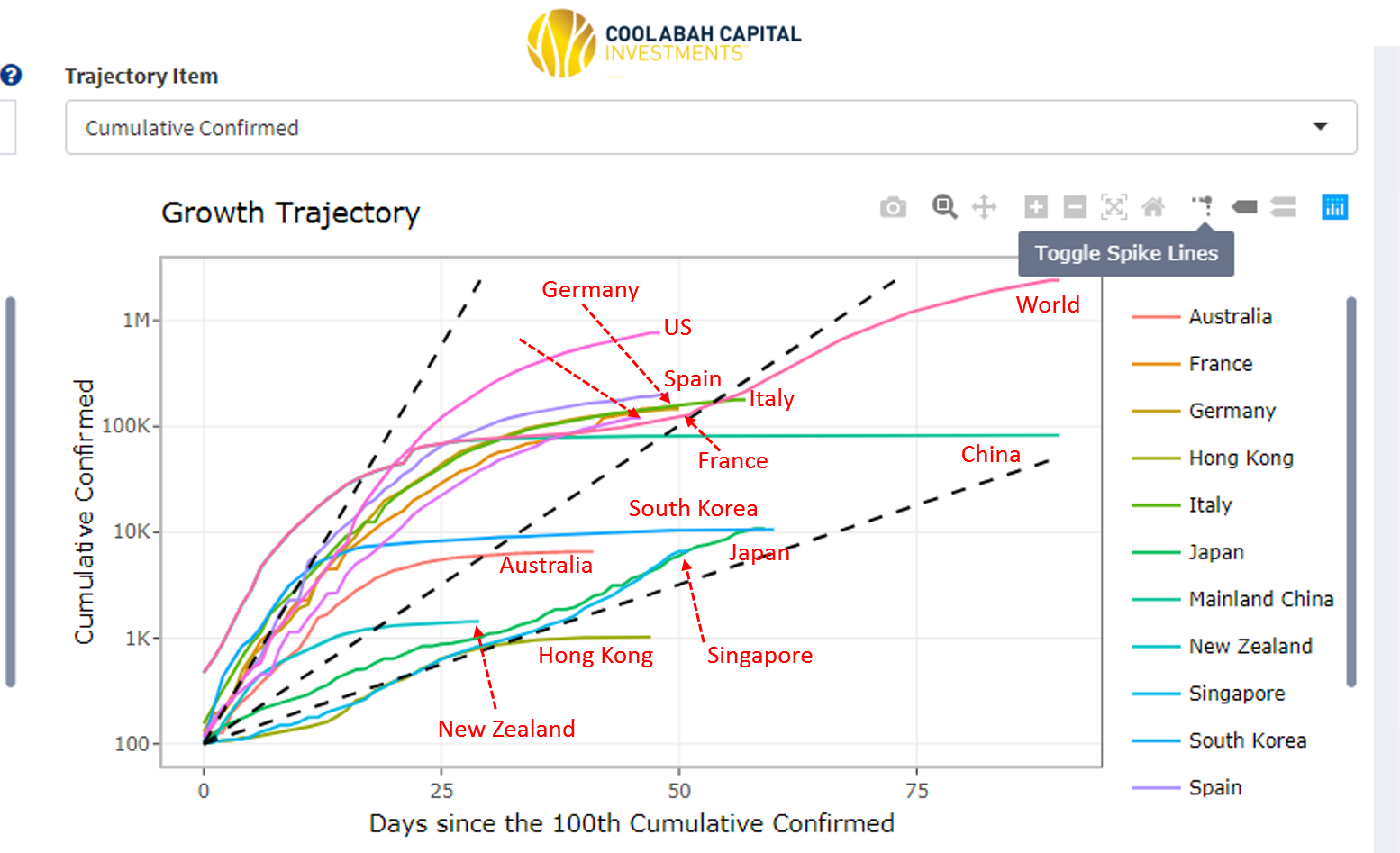

And yet according to our real-time COVID-19 infection and fatality tracking systems, Australia’s new infection numbers peaked at the start of the month. This was slightly ahead of our contrarian March forecast for a peak in US and Australian infections in early April (the US peaked on April 11).

In fact, it appears that Australia’s containment efficacy has been superior to almost all developed countries globally save Hong Kong and New Zealand, which is a tribute to Prime Minister Scott Morrison and the state premiers' policy fortitude. As a disease, COVID-19 has all but disappeared across the land. (This does not mean that there will not be small outbreaks in the future that require targeted lock-downs of specific areas, as we have seen in Tasmania.)

My fear is that the huge size of Australia’s fiscal stimulus could reduce at the margin the incentive for workers and businesses to spin activity back up. And it could unnecessarily damage Australia’s fiscal balance, burdening future generations with massive amounts of debt that was not actually warranted.

Of course, there is a circularity here: the longer you want to contain, the more stimulus and debt you need. The one thing we now know with certainty is that Australia does not need to hibernate businesses for six months, as we argued in March.

Another fear is that it might be much harder to reactivate businesses the longer we wait to do so, with the permanent economic damage increasing as a function of time.

Finally, the permanent damage wrought by lock-downs---as represented by a structural increase in unemployment, risk-aversion (ie, reduced animal spirits), and, perhaps on a more positive note, the death of Zombie businesses---might be bigger than we currently understand.

We have long argued that the rise of over-leveraged and unprofitable businesses, especially those that issue high-yield bonds, is a source of huge investment risk.

The classic case is Virgin Airlines, which in October last year issued investors a $325 million bond on the ASX. That security (ASX: VAHHA), which we did not touch because Virgin was a zombie from central casting, has traded down from $100 to $39 before it was suspended. It is presumably worth nothing now and will join the other "zeroes" in a high yield bond graveyard that is about to get increasingly full as defaults soar globally.

This is also a growing problem for the high yield debt funds listed on the ASX via Listed Investment Trusts (LITs), which suffered steep 20 per cent to 40 per cent plus losses in March, and traded at enormous discounts to their net tangible asset values, as we had repeatedly warned they would do over the last year.

Given Australia’s success with containment and the risks of over-stimulating, I would urge the government to fast-track staged and targeted exits from the current strategy as soon as possible (and work to commensurately withdraw its stimulus measures as activity normalises).

Contrary to some claims, there are potentially enormous economic, social, and health costs that directly result from a depressionary containment strategy that kills activity with the upside that it has the profound benefit of cauterising COVID-19. To blindly ignore these trade-offs on the basis of hope rather than any empirical evidence would be a unique form of policy madness.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

........

Disclaimer: This information has been prepared by Smarter Money Investments Pty Ltd. It is general information only and is not intended to provide you with financial advice. You should not rely on any information herein in making any investment decisions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Past performance is not an indicator of nor assures any future returns or risks. Smarter Money Investments Pty Limited (ACN 153 555 867) is authorised representative #000414337 of Coolabah Capital Institutional Investments Pty Ltd, which holds Australian Financial Services Licence No. 482238 and authorised representative #001277030 of EQT Responsible Entity Services Ltd that holds Australian Financial Services Licence No. 223271.

2 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment