BeFIT is now BFAT

What do gyms look like in a post coronavirus world?

Have you ever signed up to the gym with the intention that this is the year you will get in shape, only for this to quickly dissipate? You are not alone. Only a quarter of gym members actually go to the gym regularly. In fact, the less people who attend (but pay membership) is the recipe for a great gym! As a high fixed cost business, gyms have substantial operating leverage and are effectively reliant on membership wastage to turn a profit. As membership levels drift lower, the unit economics of a gym quickly deteriorates. In a post coronavirus environment, gyms could look very different. With frequent touching of equipment, this will mean regular cleaning (higher operating costs) as well as fewer new members (people not wanting to risk infection). Higher unemployment means that discretionary expenses such as gym memberships are also likely to come closer under the microscope.

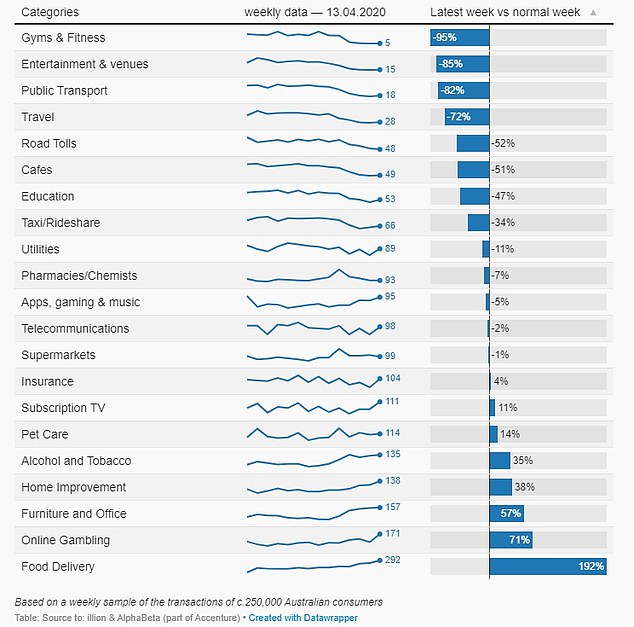

Reflective of Australia's lockdown laws, weekly spending in the gyms and fitness category in April was catastrophic, down a whopping 95% on the previous year.

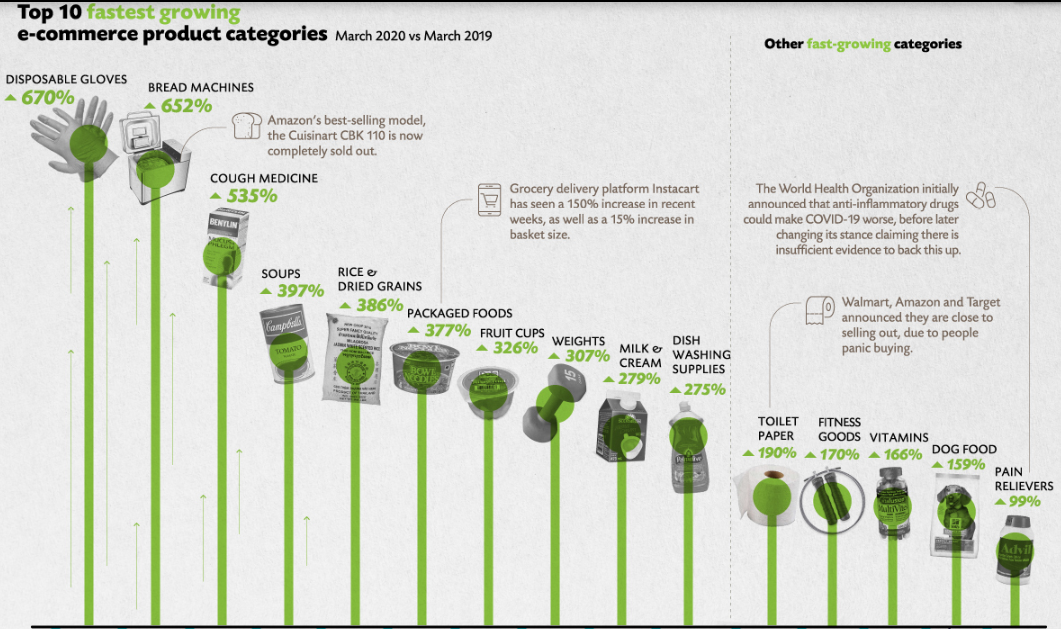

Simultaneously, home fitness equipment sales have soared. Fitness goods were one of the hottest US e-commerce categories in March, up 170%. In effect, the pandemic has pulled forward the shift towards virtual at-home fitness workouts at the expense of physical gyms.

The fallout on physical gyms can already be felt. Gold's Gym, made famous by Arnold Schwarzenegger in the documentary Pumping Iron filed for bankruptcy in recent weeks and gym chain 24 Hour Fitness is also reportedly contemplating bankruptcy.

Our research into the gym sector led us to the Netherland listed Basic-Fit (BFIT NA). In the past five years, the company has grown spectacularly, tripling its gym footprint to over 800 gyms. As a low-cost gym, its return on capital is more attractive than traditional gyms but remains capital intensive. To fund its growth, the company's net debt position has ballooned to c.€500m vs 2019 EBITDA of €155m. While we are currently in a very low-interest rate environment, we view this level of gearing as perilously high for this type of business. The company's formerly high flying share price was fuelled by rampant growth, but we struggle to see how this is sustainable given sector headwinds and gearing levels nearing debt covenant levels.

BasicFit has halved from its pre-COVID levels, but is still trading at 9x EV/EBITDA. We think the debt-fuelled growth narrative is challenged given the continued closures of gyms due to lockdown. Combined with substantial near and longer-term earnings risk we expect the share price has further downside risk.

Disclaimer: Fiftyone Capital is a global long/short fund and currently holds a short position in BFIT.

Get investment ideas from industry insiders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott is the Executive Chairman at Fiftyone Capital. As the previous CEO, Scott founded the company to manage not only his own wealth, but the wealth of other investors and families looking for a safe harbour for their capital.

2 topics

Scott is the Executive Chairman at Fiftyone Capital. As the previous CEO, Scott founded the company to manage not only his own wealth, but the wealth of other investors and families looking for a safe harbour for their capital.

Scott is the Executive Chairman at Fiftyone Capital. As the previous CEO, Scott founded the company to manage not only his own wealth, but the wealth of other investors and families looking for a safe harbour for their capital.

Comments

Comments

Sign In or Join Free to comment