TOL - 26th Mar, 2025

BHP, RIO, SFR or small caps? Which are the best ASX copper stocks to buy as Dr. Copper soars?

The Doc is back! Copper prices are again on the rise and so too are the prices of ASX copper stocks. So, which are the best to watch?

For many investors, copper was meant to be “the next big thing” of 2024 – what with all the talk of looming supply shortages and burgeoning demand from the booming decarbonisation industry. But, after a massive rally that peaked last May, it was largely a year of disappointment for copper bulls.

Fast forward to the new year, and there has been a major revitalisation of the copper price – arguably this time without the next big thing narrative. Instead, copper’s recent fortunes appear more to be about the impact of the escalating global trade war.

So, can the run continue? And if so, which ASX stocks are best placed to take advantage? I’m glad you asked – let’s dive in with expert fundamental and technical views on copper, as well as how to play its resurgence via ASX copper stocks both big and small.

The experts’ view on copper

In its latest update on copper (Metal Matters March 12, 2025), Citi Research upgraded its short-term outlook, reflecting a growing bullish stance driven by U.S. import demand and looming tariff implications. The broker now forecasts a copper price target of $10,000/t over the next three months, up from its prior estimate of $8,500/t.

That’s a nice upgrade, around 17.6%, but given the recent run-up in the copper price Citi’s new $10,000/t target is now largely achieved. The current price of London Metals Exchange (LME) copper is US$9,911/t (FYI, it closed at US$9,776 the day Citi made its new call – so their then-prevailing US$8,500/t call was already behind the eight-ball).

Citi attributes this revision to a confluence of factors, including “temporarily stronger US copper import demand,” and increased interest in physical arbitrage opportunities created by anticipated tariffs in the second half of 2025. The firm expects copper to remain robust into the second quarter, with US copper contract demand tightening ex-US markets before a tariff-related unwind later in the year.

Citi’s bullish near-term copper analysis summary:

U.S. Import Surge: Citi notes a significant drawdown in LME inventories of non-Russian-origin copper, down to around 80,000 tons in February, reflecting heightened US demand. “This reflects the arb-related surge in US import demand”, Citi explains.

Tariff Expectations: Citi expects a 25% US import tariff will be applied to copper before the end of the year, though current market pricing via 1-year forwards contracts suggests only approximately 11% is so far factored in.

China’s Supply Constraints: Treatment charges for copper concentrate in China have hit multi-year lows, underscoring raw material shortages against expanding smelting capacity.

Fund Positioning: Copper net long positions have soared, driven by fresh longs and short covering, predominantly on the LME.

While bullish in the near term, Citi cautions that the incentive to stockpile copper ahead of tariffs could reverse post-implementation, potentially pressuring prices later in 2025. For now, though, the brokerage sees a relatively clear runway for continued copper price strength.

In a Morgan Stanley research report released Wednesday titled “Can Copper's Climb Continue?”, this broker also noted significant transfers of physical copper from ex-US sources, particularly Asia, into the US ahead of an expected 25% import tariff. Also contributing to the prevailing tightness in copper markets is around 250kt of supply guidance downgrades year to date from producers, plus a greater than expected seasonal decline in production output from Chile.

Morgan Stanley agrees the current backdrop for copper appears supportive of recent price increases in the metal, and also has a mid-year target of US$10,000/t. However, the firm warns that positioning is increasingly becoming skewed to the long side (implying the market is already factoring in positive fundamentals), but not yet as extreme as it was heading into the 2024 May peak. The key risk to the copper price, suggests Morgan Stanley, is if a US import tariff doesn't materialise.

The technical analyst’s view on copper

Just like Hannibal Smith said back in the 80’s action hit “The A-Team”, “I love it when a plan comes together” – well, I love it when the fundamentals and technicals align!

I’ve been tracking the gyrations of the copper price – both on the LME and on the COMEX exchange in the US via my regular ChartWatch section of our Market Index Evening Wraps. In those updates, I flipped bullish after the long, volume-backed demand-side candle on 13 March – relatively early in the Feb-May move – and then expressed major concerns about the sustainability of the trend after the huge supply-side candle on 22 May (i.e., pretty much nailed it!).

I’ll admit, I bought the dummy on the Sep-Oct rally, only to be soon disappointed, but then remained largely bearish-neutral until 6 February this year. In that edition of ChartWatch, I cited the strong demand-side candle of 5 February, as well as the preceding candles, as a credible signal the demand-side had returned to control of the short-term copper price. I have remained consistently bullish in several updates since (pretty much nailed it again!).

%20COMEX%20chart%2020%20March%202025.png)

Now, I note both short and long term uptrends (represented by the light green and dark green ribbons) are well-established, and both trend ribbons appear to be acting as zones of dynamic demand (the price action is bouncing off them). This is consistent with strong demand-side control and a healthy bull market.

The price action, i.e., the relative positioning of peaks and troughs is rising peaks and rising troughs, a signal of supply removal and demand reinforcement. Candles are predominantly demand-side in nature (i.e., white-bodied and or with downward pointing shadows). Both factors are consistent with strong demand-side control and a healthy bull market.

However, and here’s a bit of a short-term sticking point – I do expect there to be a substantial amount of excess supply in a wide zone defined by the 28 May peak of 5.0845, and up to the ‘big one’ – a smaller zone defined by the 20 May peak of 5.3805 and the 7 Mar 2022 major peak of 5.3935.

So, as good as copper looks, and as good as the signs are that the demand side remains firmly in control of its price – we could start to see the fingerprints of excess supply creep in from here. By this, I mean investors should be attentive for:

- A growing prevalence and increased size of supply-side candles (i.e., black-bodied and or those with upward-pointing shadows

- If these supply-side candles develop into a peak, or series of falling peaks in the supply zone, and or into a series of falling troughs.

- If the price closes below the short-term trend ribbon.

But I am not a trend prognosticator – this is a futile exercise as the future is unknown – I am a trend follower. So, until I see the fingerprints of excess supply listed above, I have no reason to doubt the prevailing short and long term uptrends.

The experts’ views on ASX copper sTOCKS

Let’s start with the big caps and work our way down. Obviously, the smaller we go in terms of market capitalisation – the slimmer the pickings with respect to broker coverage. Keep in mind that a stock that has only one or two ratings hardly constitutes a “consensus” – so in line with this, we’ll only provide a Consensus Rating and Consensus Target for companies that have at least three broker reports within the last 3 months (to keep it current).

To obtain a stock’s Consensus Rating, we assign a value of +1 to any rating better than HOLD/NEUTRAL/MARKETWEIGHT, a value of 0 for any rating equivalent to HOLD/NEUTRAL/MARKETWEIGHT, and a value of -1 to any rating worse than HOLD/NEUTRAL/MARKETWEIGHT.

We then take the average of all assigned rating values and assign a Consensus Rating of BUY to values greater than +0.5, a rating of HOLD for values between -0.5 and +0.5, and a rating of SELL for values less than -0.5.

The Consensus Target is simply the average of the target prices we have on file for each broker. Typically, brokers define their target price as a 12-month forecast, and each target price is based on a broker’s fundamental valuation assumptions.

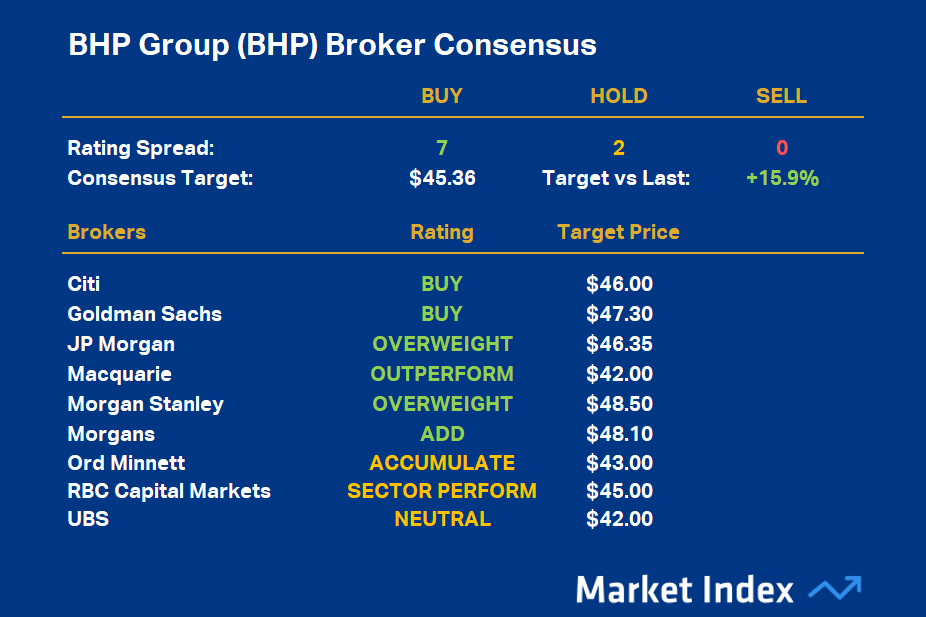

BHP Group (ASX: BHP) - Market Cap: $208 billion

%20Broker%20Consensus.png)

BHP’s broker consensus rating is +0.78, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $45.36. This suggests brokers collectively believe the stock is around 15.9% undervalued based upon the closing price on Thursday, 20 March of $39.13.

BHP - Copper quick take:

- BHP has interests in copper mines in Chile (Chile: Escondida (57.5%), Spense, Pampa Norte), Peru (Antamina (33.75%)), the USA (Resolution Copper (45%) (development)), and Australia (Olympic Dam, Carrapateena, Prominent Hill).

- Iron ore is still the main game at BHP, but it boasts the largest copper reserves and resources of any ASX copper company, as well as the highest annual production.

- Fourth largest copper producer in the world (the third largest independent producer) with FY24 copper production of 1,865kt.

- Dividend yield approximately 4.8% fully franked.

- According to Morgan Stanley, copper contributes 34% of BHP Group’s revenue (49% comes from iron ore, and 14% from metallurgical coal).

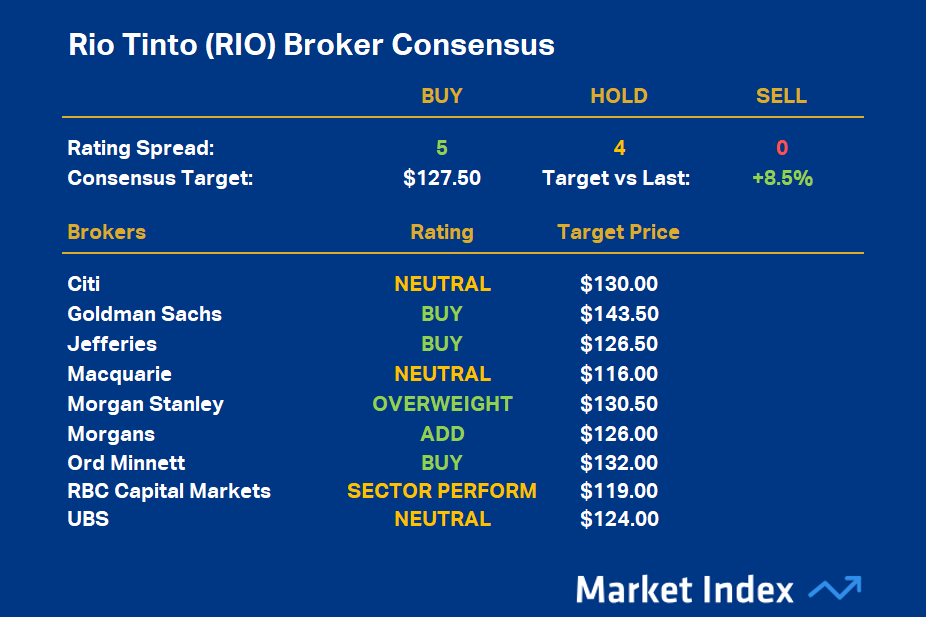

Rio Tinto (ASX: RIO) - Market Cap: $203 billion

%20Broker%20Consensus.png)

RIO’s broker consensus rating is +0.56, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $127.50. This suggests brokers collectively believe the stock is around 8.5% undervalued based upon the closing price on Thursday, 20 March of $117.50.

RIO - Copper quick take:

- Rio has interests in copper mines in Chile (Escondida (30%), Nuevo Cobre (development)), the USA (Kennecott, Resolution Copper 55% (development)), and Mongolia (Oyu Tolgoi).

- RIO produced 697kt of copper in FY24.

- The Oyu Tolgoi ramp-up is expected to result in production of around 500kt of copper per year on average from 2028 to 2036, compared to 130kt tonnes in 2022. By 2030, Oyu Tolgoi is expected to be the fourth-largest copper mine in the world.

- Dividend yield approximately 5.2% fully franked.

According to Morgan Stanley, copper contributes 12% of Rio Tinto’s revenue (57% comes from iron ore, and 22% from aluminium). In terms of group EBITDA, copper’s contribution is 9%, and this is expected to grow to around 27% by 2025.

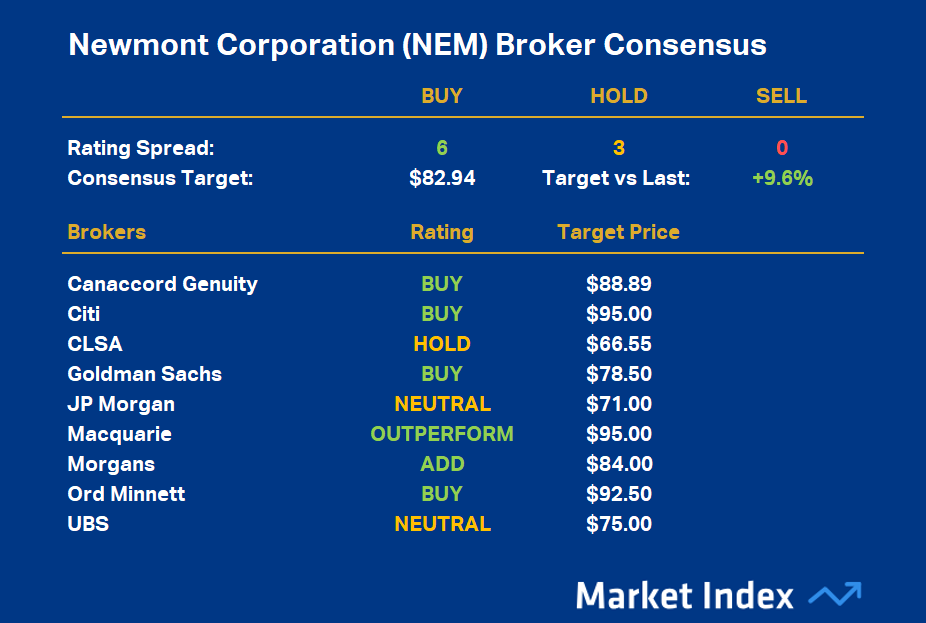

Newmont Corporation (ASX: NEM) - Market Cap: $92 billion

%20Broker%20Consensus.png)

NEM’s broker consensus rating is +0.67, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $82.94. This suggests brokers collectively believe the stock is around 9.6% undervalued based upon the closing price on Thursday, 20 March of $75.66.

NEM - Copper quick take:

- Is the world’s largest gold producer (a bit of a bonus at the moment 🥇!)!

- Copper is typically produced by NEM as a by product of its gold mining, but it does have interests in copper-focussed mines in Chile (Nueva Unión (50%), Norte Abierto (50%)) and Peru (Yanacocha).

- NEM will produced approximately 35kt of copper in 2024.

- Dividend yield approximately 1.9% unfranked.

- Copper accounts for approximately 15% of Newmont’s revenue.

South32 (ASX: S32) - Market Cap: $16.3 billion

%20Broker%20Consensus.png)

S32’s broker consensus rating is +0.70, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $3.92. This suggests brokers collectively believe the stock is around 8.1% undervalued based upon the closing price on Thursday, 20 March of $3.62.

S32 - Copper quick take:

- S32 owns 45% of the Sierra Gorda copper mine in Chile.

- S32 produced approximately 61kt of copper in FY24.

- Dividend yield approximately 2.8% fully franked.

- According to Morgan Stanley, copper contributes 6% of South32’s revenue (53% comes from aluminium and alumina, 14% from metallurgical coal, 6% from Nickel, 3% from silver, 3% from lead, 2% from zinc and 1% from thermal coal).

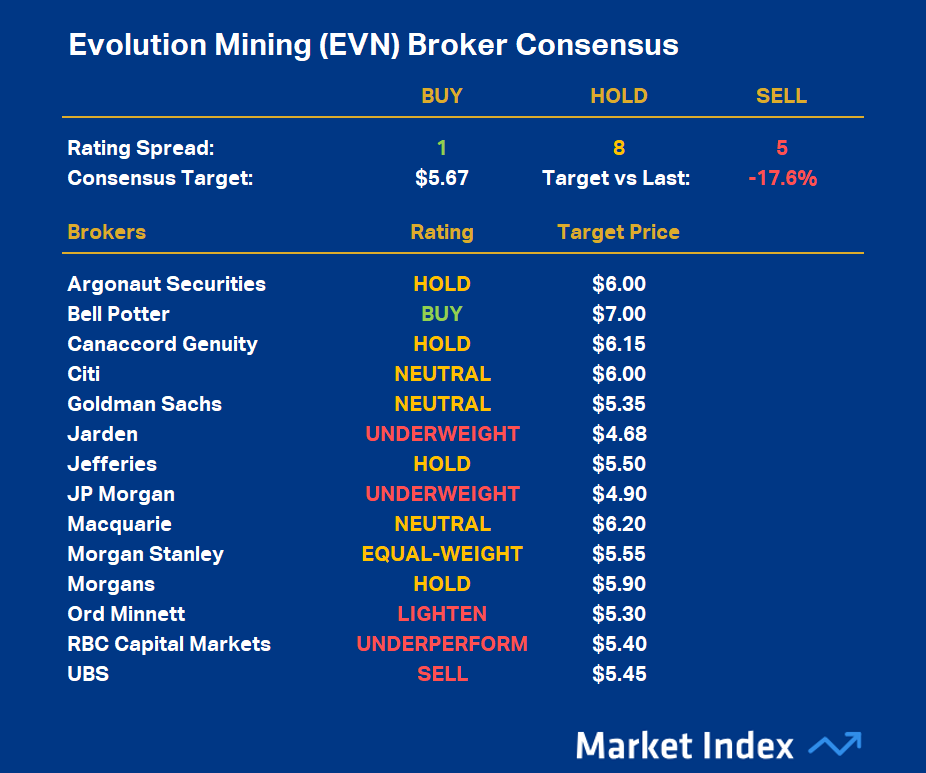

Evolution Mining (ASX: EVN) - Market Cap: $13.7 billion

%20Broker%20Consensus.png)

EVN’s broker consensus rating is -0.29, resulting in a Broker Consensus Rating of HOLD. Its Broker Consensus Target is $5.67. This suggests brokers collectively believe the stock is around 17.6% overvalued based upon the closing price on Thursday, 20 March of $6.88.

EVN - Copper quick take:

- Copper is typically produced by EVN as a by product of its gold mining.

- RIO produced 68kt of copper in FY24.

- Dividend yield approximately 1.8% fully franked.

- According to Morgan Stanley, copper contributes 26% of Evolution Mining’s revenue (74% comes from gold).

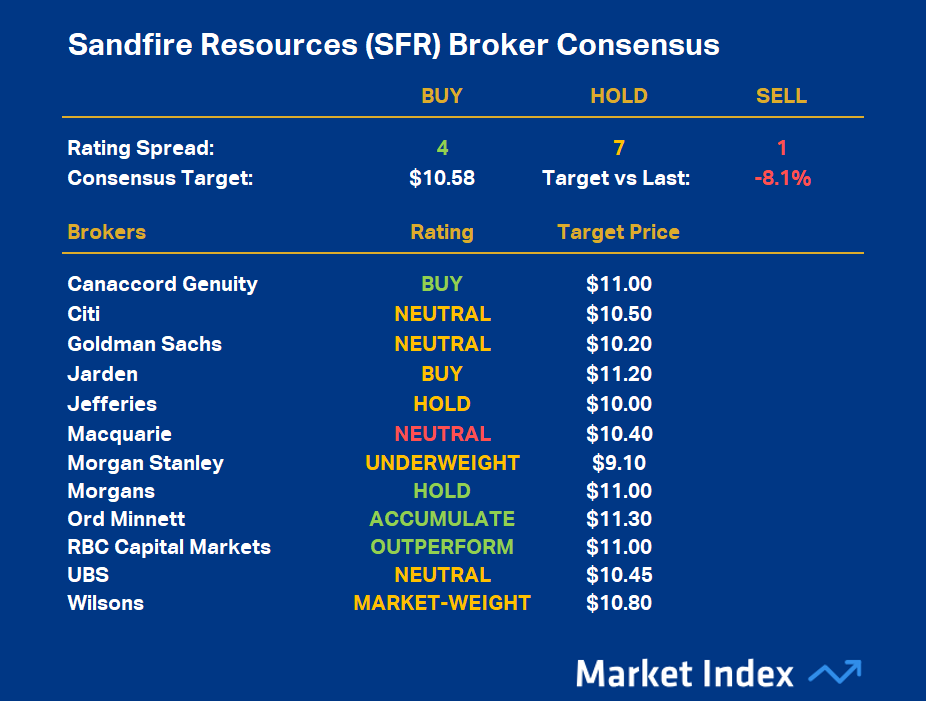

Sandfire Resources (ASX: SFR) - Market Cap: $5.3 billion

%20Broker%20Consensus.png)

SFR’s broker consensus rating is +0.25, resulting in a Broker Consensus Rating of HOLD. Its Broker Consensus Target is $10.58. This suggests brokers collectively believe the stock is around 8.1% overvalued based upon the closing price on Thursday, 20 March of $11.51.

SFR - Copper quick take:

- Sandfire is a copper-focussed company (the first in this list - making it the largest ASX listed copper-pure play) with major operations located in Botswana (Motheo) and Spain (MATSA), it also has a development project in the USA (Black Butte).

- SFR produced 134kt of copper in FY24.

- According to Morgan Stanley, copper contributes 77% of Sandfire Resources’ revenue (15% comes from zinc, 6% comes from silver, and 2% comes from lead).

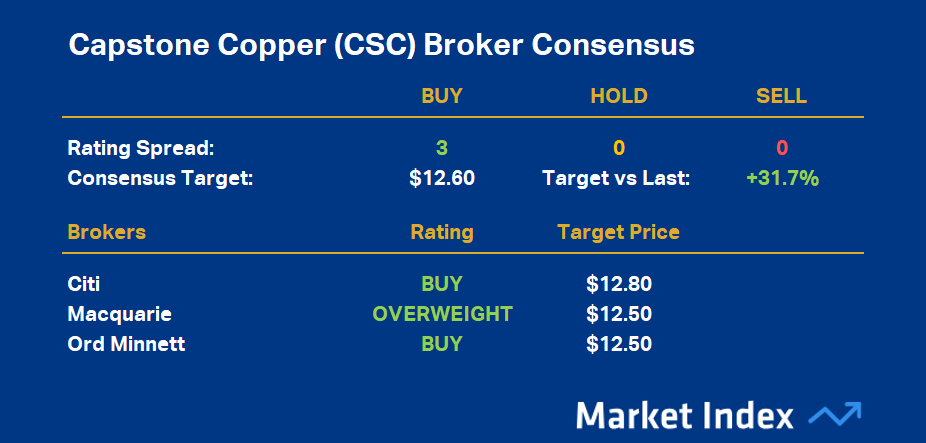

Capstone Copper Corp. (ASX: CSC) - Market Cap: $1.7 billion

%20Broker%20Consensus.png)

CSC’s broker consensus rating is +1.0, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $12.60. This suggests brokers collectively believe the stock is around 31.7% undervalued based upon the closing price on Thursday, 20 March of $9.57.

CSC - Copper quick take:

- CSC produces copper from several mines located in the USA (Pinto Valley), Mexico (Cozamin), Chile (Mantos Blancos, Mantoverde (70%), Santo Domingo).

- CSC produced a total of 184kt of copper in 2024 at a C1 cash cost of US$2.53/lb.

MAC Copper (ASX: MAC) - Market Cap: $679 million

%20Broker%20Consensus.png)

MAC’s broker consensus rating is +1.0, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $24.38. This suggests brokers collectively believe the stock is around 41.9% undervalued based upon the closing price on Thursday, 20 March of $17.18.

MAC - Copper quick take:

- Acquired 100% of CSA Copper Mine located in NSW from Glencore in June 2023.

- MAC claims the CSA Copper Mine is the “Highest-grade copper mine in Australia with an Ore Reserve grade of 4.0% Cu and a Mineral Resource grade of 5.32%”.

- MAC produced 41.2kt of copper in 2024.

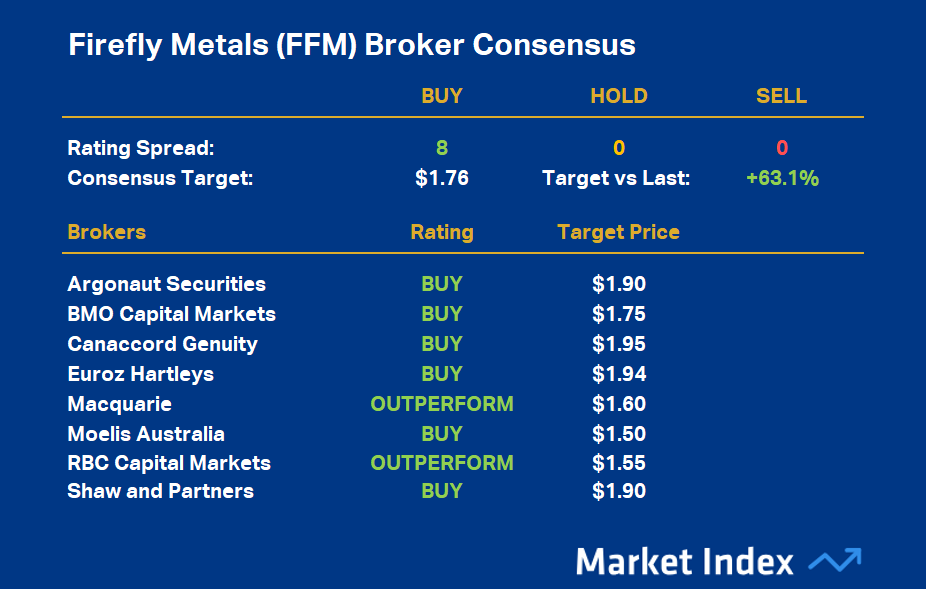

Firefly Metals (ASX: FFM) - Market Cap: $610 million

%20Broker%20Consensus.png)

FFM’s broker consensus rating is +1.0, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $1.76. This suggests brokers collectively believe the stock is around 63.1% undervalued based upon the closing price on Thursday, 20 March of $1.080.

FFM - Copper quick take:

- FFM owns the Green Bay copper-gold project is located in the Baie Verte district of north-east Newfoundland, Canada.

- Green Bay has Measured and Indicated Mineral Resources of 460kt of contained copper at 1.9% copper equivalent cutoff and Inferred Mineral Resource of 690kt of contained copper at 2.0% copper equivalent cutoff, but also has deposits of gold and silver.

- The company is at the exploration stage, and therefore is unlikely to be producing copper in the short-medium term.

Aurelia Metals (ASX: AMI) - Market Cap: $431 million

%20Broker%20Consensus.png)

With only two brokers covering AMI, we did not calculate its broker consensus data.

AMI - Copper quick take:

- AMI has three main Australian-based copper interests: Peak (North and South), Federation (development), and Great Cobar (development).

- AMI is expected to produce 2.5-3.5kt of copper in FY25 (but also 40-50koz gold, 14-20kt zinc, and 13-19kt lead).

- According to Macquarie, in FY24 approximately 58% of revenue exposure is from gold, approximately 42% from base metals; in FY25 this will transition to approximately 30% of revenue exposure to come from gold and approximately 70% from base metals with around 30% from copper.

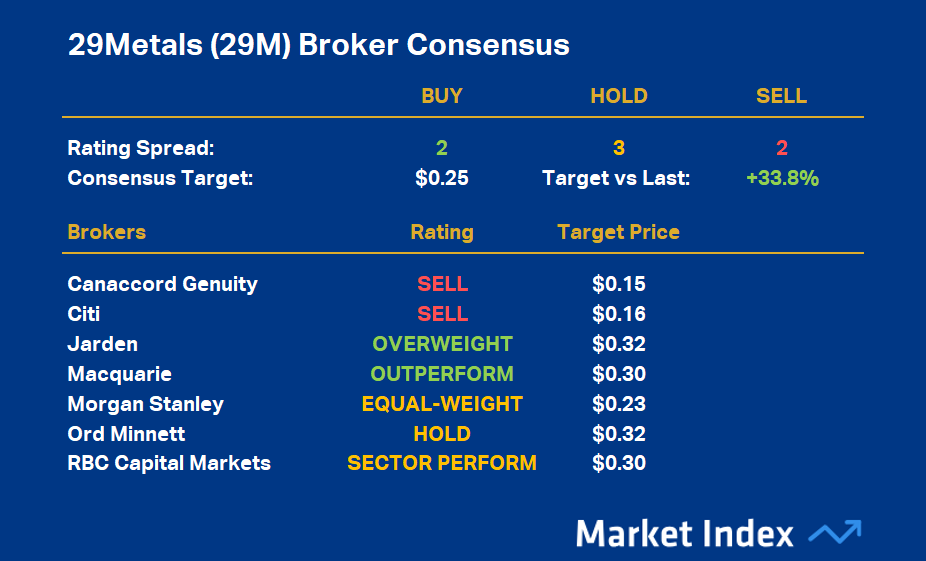

29Metals (ASX: 29M) - Market Cap: $260 million

%20Broker%20Consensus.png)

29M’s broker consensus rating is +0.0, resulting in a Broker Consensus Rating of HOLD. Its Broker Consensus Target is $0.254. This suggests brokers collectively believe the stock is around 33.8% undervalued based upon the closing price on Thursday, 20 March of $0.190.

29M - Copper quick take:

- AMI has three main Australian-based copper interests: Golden Grove, Capricorn Copper, and Redhill.

- On 26 March 2024, 29Metals announced the closure of their Capricorn Copper mine due to flooding. The company has not specified a time that operations will recommence.

- 29M produced 5.3kt of copper in 2024.

- According to Morgan Stanley, copper contributes 59% of 29Metals revenue (25% comes from zinc, 8% from gold, and 6% from silver).

AIC Mines (ASX: A1M) - Market Cap: $242 million

%20Broker%20Consensus.png)

A1M’s broker consensus rating is +1.0, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $0.730. This suggests brokers collectively believe the stock is around 73.8% undervalued based upon the closing price on Thursday, 20 March of $0.420.

AIC - Copper quick take:

- AMI has three main Australian-based copper interests: Eloise, Marymia (development), and Lamil (50%) (development).

- AIC Mines is targeting annual production of approximately 12.5kt of copper production and 5koz of gold production in FY25.

- Approximately 88% of the company’s revenue comes from copper versus approximately 12% from gold.

- The long term goal at Eloise is to get to 20kt p.a. production for a 10 year mine life (plus 7.5koz p.a. gold).

Aeris Resources (ASX: AIS) - Market Cap: $170 million

%20Broker%20Consensus.png)

AIS’s broker consensus rating is +0.67, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $0.270. This suggests brokers collectively believe the stock is around 54.3% undervalued based upon the closing price on Thursday, 20 March of $0.175.

AIS - Copper quick take:

- AMI has four main Australian-based copper interests: Tritton, North Queensland (Mt. Colin), Jaguar, and Stockman.

- AIS produced 19.7kt of copper in 2024.

- Approximately 66% of the company’s revenue comes from copper versus 25.5% from gold.

The technical analyst’s views on ASX copper stocks

How do the charts of each of the abovementioned ASX copper stocks look? Can they keep rising?

We’ll do these on Monday, so be sure to keep an eye on the LiveWire latest news feed!

This article first appeared on Market Index on Friday 21 March.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

%20COMEX%20chart%2020%20March%202025.png){kind=link}

%20Broker%20Consensus.png){kind=link}

%20Broker%20Consensus.png){kind=link}

%20Broker%20Consensus.png){kind=link}

%20Broker%20Consensus.png){kind=link}

%20Broker%20Consensus.png){kind=link}

%20Broker%20Consensus.png){kind=link}

%20Broker%20Consensus.png){kind=link}

%20Broker%20Consensus.png){kind=link}

%20Broker%20Consensus.png){kind=link}

%20Broker%20Consensus.png){kind=link}

%20Broker%20Consensus.png){kind=link}

%20Broker%20Consensus.png){kind=link}

5 topics

13 stocks mentioned

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment