Bread, Water and FAANGs

The tremendous performance of the U.S. equity market over the past six months has confounded many investors. Yet, look under the surface and it might make more sense. While cyclical segments of the market have floundered under the lingering weight of lockdown effects and pandemic fear, companies which can complement and improve life with COVID-19—the likes of Facebook, Amazon, Apple, Netflix and Google—have thrived, rolling out stellar results and powering overall market performance. With populations largely confined to their homes and having to socialize, work, shop and find entertainment online, households have prioritised their spending to bread, water, and FAANGs.

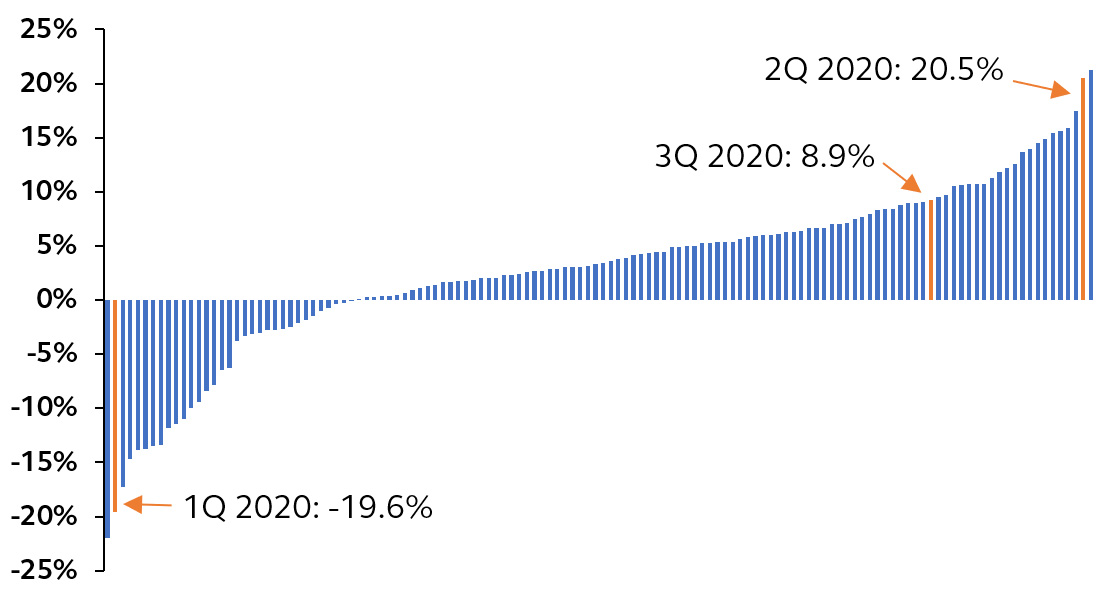

S&P 500 Total Return Index quarterly performance

Percent, 1988 – present

Source: Bloomberg, Principal Global Investors. Data as of September 30, 2020.

The top five companies in the S&P 500, Facebook, Apple, Microsoft, Amazon and Google (inconveniently creating the less enticing acronym FAMAG), make up over a fifth of the entire market capitalisation of the S&P 500 index and around half of the NASDAQ 100. These tech-ish darlings—Amazon is considered a consumer discretionary company, not tech—have done some serious heavy lifting. At the end of September, even as less than half the stocks on the New York Stock Exchange closed above their 200-day moving average, the S&P 500 index capped its best two-quarter performance since 2009, rising some 30% while, even more astoundingly, the tech-heavy NASDAQ Composite index has recorded a 45% increase in the past 6 months alone.

NYSE stocks trading above 200 day moving average

Percent, September 2010 – present

Source: Bloomberg, Principal Global Investors. Data as of September 30, 2020.

These frenzied moves higher have inevitably stretched investors’ belief in the sustainability of Big Tech’s outperformance. Price to earnings ratios have been propelled to levels associated with the dot-com boom, and our own PGAA Equity Valuation Composite suggests that the MSCI USA Growth index (which has significant tech exposure) has almost never been more expensive. At these elevated levels, investors increasingly require vindication in the form of robust earnings growth in order to maintain their tech exposure, multiplying concerns about the overall market’s heavy reliance on the technology sector to generate earnings in a post-COVID world.

A September swoon

Admittedly, although the Q3 market performance was decidedly solid, this was despite a more difficult September. Market sentiment was tainted by growing concerns around several issues, including fears around the U.S. Presidential Election, rising COVID cases, and disappointment over U.S. fiscal stimulus. By themselves, none of these events were sufficiently important to drive a market pullback. Yet, they coincided with stretched valuations, heavily overbought conditions and investor complacency, bringing a temporary end to the post-COVID rebound in financial markets.

Big Tech was not immune, and the best performing sector converted into an underperformer. The Nasdaq Composite fell into correction territory—defined as at least a 10% drop from the recent high—just three sessions after hitting a record, the speediest-ever such fall.

While Big Tech has since regained some ground, investors have expressed concern about their continued rattled performance. Yet, we consider the September swoon as a natural speed bump for the sector.

Conditions remain broadly supportive of Big Tech

While other sectors have struggled to survive, the COVID crisis created the perfect trio of conditions for Big Tech firms to thrive: limited physical social interaction, an uncertain economic backdrop, and depressed bond yields. These conditions remain firmly in place.

- COVID-19: The pandemic is by no means over and cases are once again rising in the U.S. and even spiking above the April peaks in Europe. While deaths have generally remained low, permitting governments to prioritize economic reopening, several European cities have clamped down once again on social gatherings, while New York City is considering reintroducing new public health restrictions. As such, the acceleration of digital trends for business, education and households in the wake of the pandemic is unlikely to fade anytime soon. The stay-at-home trade is still in vogue.

- Economic backdrop: The global economic recovery has progressed faster than many had envisaged, yet there is still some way to go before the global economy returns to pre-pandemic levels. Generous government stimulus and insurance programs that have buffeted the recovery are beginning to wind down and economic scarring is likely to become more apparent as companies increasingly report closures and job cuts in Q4. What’s more, with the pandemic still at large, consumers and businesses will remain restrained by virus fear, thereby sustaining the uncertain backdrop. Big Tech companies—with their strong balance sheets, positive cash flow and resilient earnings—will continue to be considered as a relative safe haven.

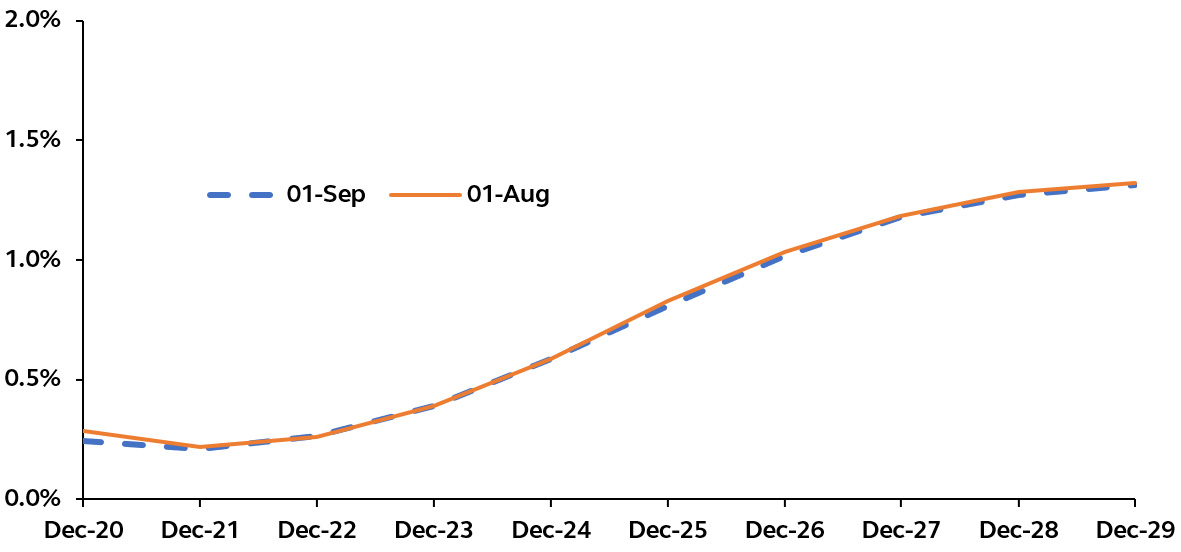

- Bond yields: As so much of Big Tech profits lie far in the future, their valuations benefit tremendously from low rates. The Federal Reserve’s recent adoption of a new average inflation targeting framework explicitly permits inflation to tick above 2% for some time before the central bank looks to tighten monetary policy. The implication is that asset purchases will continue, policy rates are essentially locked near zero, and investors can expect short-term bond yields to be pinned down for the foreseeable future. What’s more, while the economy is healing, inflationary pressures will be contained, putting little upward pressure on long-end bond yields over the next year or so.

Forward path for Fed Funds rate

Euro$ futures, percent, 2020-2029

Source: Bloomberg, Principal Global Investors. Data as of September 30, 2020.

Without evidence of a broader economic recovery and rekindling of inflation pressure, there is little in the fundamental market dynamics to suggest tech disappointment in the near-term.

Of course, technology stocks are by no means bullet proof. Each passing day seems to bring positive announcements regarding a viable and effective vaccine. While a breakthrough would clearly be great news, it would be less positive for the tech sector. The pandemic has triggered many behavioral changes and, just as definitive progress on COVID-19 and a pick-up in global growth momentum would likely result in a reflation rotation, a vaccine would trigger a re-allocation into less-loved cyclical sectors.

At the same time, while tech sector valuations are elevated, the earnings and revenue potential in the coming years from areas such as cloud computing, artificial intelligence, and cyber security will remain sturdy, regardless of a vaccine. Investors should be reassured that, while dependence on technology will likely fade somewhat as households and companies look to return to a more normal way of life, technology will inevitably continue play a greater role than it did pre-COVID.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors. Enjoy this wire? Hit the 'like' button to let us know.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire