CBA: Much, much better than expected

Normally the semi-annual profit results from the Commonwealth Bank are fairly staid affairs, with the bank delivering consistent profits with few surprises. However, this reporting season the CBA result will face a far greater degree of scrutiny after the annus horribilis of 2018.

In this period, the bank has faced 9 challenges:

1) Royal Commission

2) CEO resignation

3) CFO resignation

4) Settlement with AUSTRAC for $700 million

5) Demerging Colonial Wealth Management

6) APRA Inquiry

7) Sale of life insurance business,

8) settlement of interest-rate rigging case with ASIC and

9) A weak 3rd quarter update in May.

When companies confront the range of issues that CBA has faced over the past 12 months, new management teams often have the opportunity to rebase earnings downwards, thus giving themselves easier hurdles to jump over in the future.

The market was quite pessimistic on CBA going into this result and so has been surprised at the +3.7% increase in cash profits and that the dividend was slightly increased.

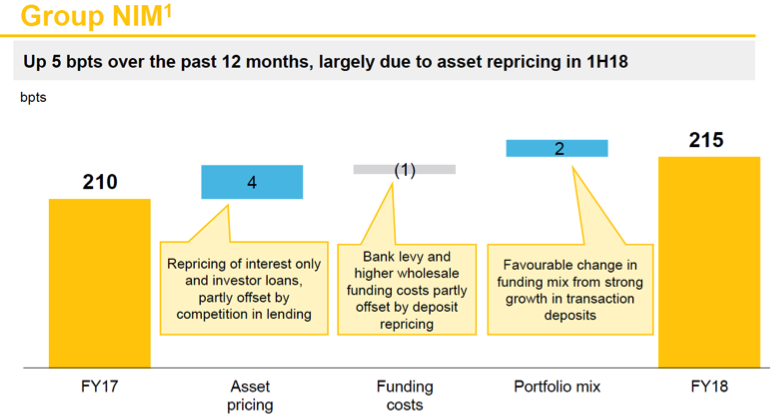

The 2018 result also showed that the bank had increased their net interest margin [(Interest Received - Interest Paid) divided by Average Invested Assets] from 2.1% to 2.15%. Whilst this does not sound like much, small changes in this margin are beneficial when applied to an asset base of $975 billion.

The expansion in this margin shows that over the past year CBA has been successful in both raising prices on their loans and reducing the interest rates paid to those that lend the bank money such as depositors.

A significant feature in the profit growth that the major Australian banks have enjoyed over the past five years has been declining bad debt charges. Consequently, one of the key financial indicators to look at is a banks' bad debt charge, as a rise in this charge is likely to indicate the start of a cycle of rising bad debts as these charges normalise to a long-term average of around 0.3% of gross loans. This result showed that CBA’s impairment charge actually fell further to 0.13% over the past six months.

Result was better than we expected

2018 has been a tough year for investors in bank stocks and in particular for CBA shareholders. The prevailing narrative has been a negative one dominated by concerns about the Royal Commission, house prices and exciting fintech companies displacing the banks.

We added to the CBA weight during the Royal Commission and going into the result, as we saw that the market price discounted both the resilience of the CBA’s key profit centre retail banking services and management’s ability to respond to the changing environment.

Our positive investment view towards Australia’s premier retail bank has not changed, though in fairness this result was better than we expected.

What the market was underestimating

Going into this result the market has been overlooking CBA’s ability to pull various levers to maintain profits in response to changing market conditions.

Going into this result the market was expecting contractions in the bank’s net interest margin, due to rising funding costs as measured by the BBSW (bank bill swap rate) and the impact of 2017’s big bank levy.

The below table shows the levers pulled by management to maintain profits, namely raising rates on loans and controlling the rates that the bank pays for retail deposits.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Atlas is a boutique investment manager focused on income-related strategies in both Australian Equities and Listed Property and Infrastructure. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth & Praemium. Atlas' Australian Equity Income Fund (ASX:AFM01) provides quarterly income with low volatility. Click follow to be the first to get my next wire.

3 topics

1 stock mentioned

Atlas is a boutique investment manager focused on income-related strategies in both Australian Equities and Listed Property and Infrastructure. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available...

Expertise

Atlas is a boutique investment manager focused on income-related strategies in both Australian Equities and Listed Property and Infrastructure. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available...

Expertise

Comments

Comments

Sign In or Join Free to comment