Cheap(ish) Cobalt explorers are very hard to find - N27.ASX stood out against peers

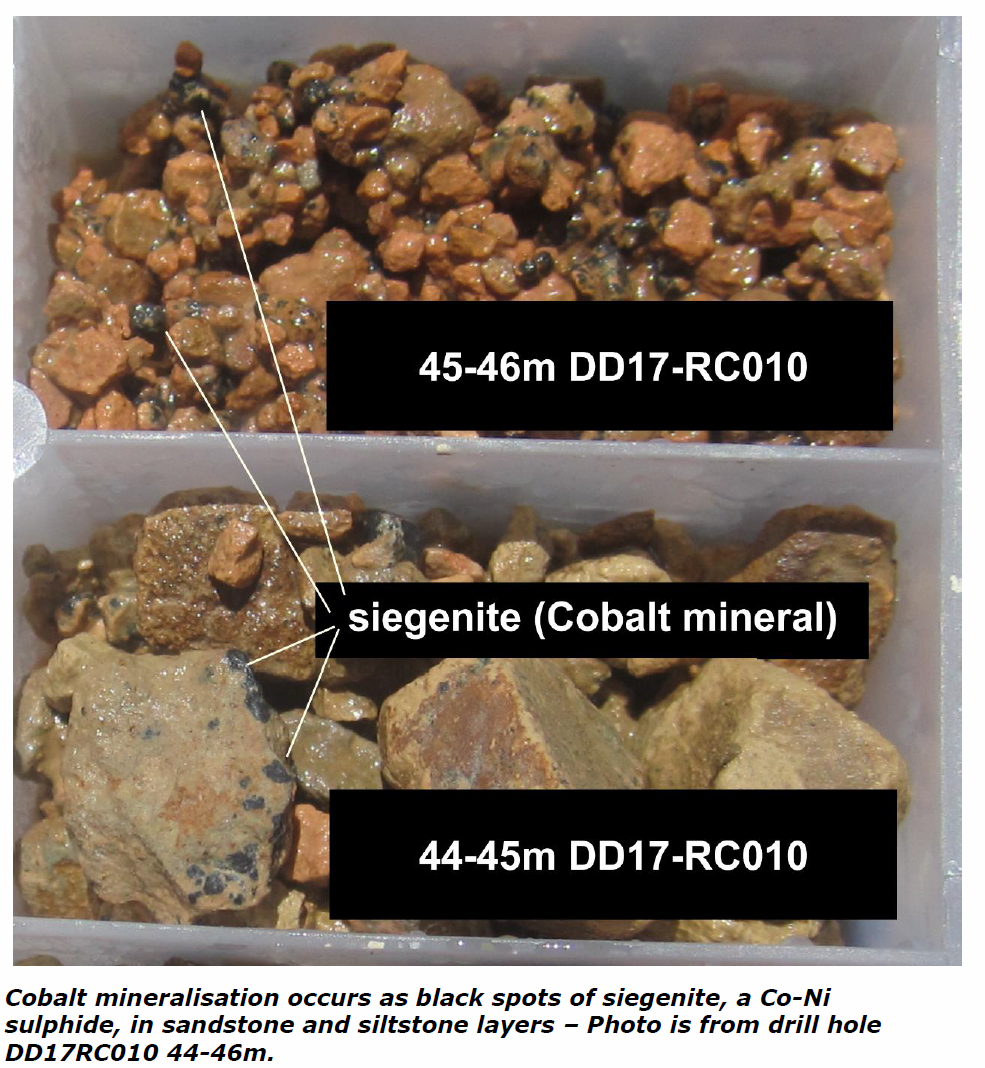

Tracking Kidman (KDR.ASX) through the Marindi (MZN.ASX) court case and beyond, has been rewarding for us in the Li space. It also focused attention on the EV/Battery space and as a derivative of that demand, Cobalt (Co + ~250% in 12 months). It is hard to find Co pure plays as Co historically sat as base metal credit for producers, and tiny grades barely got tongues wagging on drill results. Now Co has broken through US$60k/t, drill results with 0.15% Co grades get market interest! We struggled to find "relative" value amongst the junior Co explorers, with a lot already running on results. Yesterday, we sent a trading desk note to clients discussing relative value amongst juniors, highlighting one name we own, Northern Cobalt (N27.ASX), which, in our view, stood out on a comparative basis, given market cap, location, existing resource (JORC 2012 COMPLIANT INFERRED MIN RESOURCE 500,000T @ 0.17% Co, Ni 0.09% AND 0.11% Cu) and current 20,000m drill program. If the reader has interest in the junior explorer sector (and understands the associated risks) then the desk note might be of interest (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tom is a Founder and Head of Wealth Management. Since 2012, he has been running the Alpine Model Portfolios, focusing on macroeconomics and tactical equity positioning. These portfolios were initially created as a solution for "core wealth management" for Alpine's HNW clients, and are now openly available online through the website. Everything starts with the macro, and then we work back from there in terms of asset allocation and positioning for risk. We work with leading independent research providers and have a structured approach that has worked very well over time. Outside of the core portfolios, we look for opportunities in the small to mid-cap sectors of the market, where our experience can add value.

2 topics

Tom is a Founder and Head of Wealth Management. Since 2012, he has been running the Alpine Model Portfolios, focusing on macroeconomics and tactical equity positioning. These portfolios were initially created as a solution for "core wealth...

Expertise

Tom is a Founder and Head of Wealth Management. Since 2012, he has been running the Alpine Model Portfolios, focusing on macroeconomics and tactical equity positioning. These portfolios were initially created as a solution for "core wealth...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Could these 2 stocks become the ASX's next 10-baggers?

Livewire Markets

Equities

The 7 zombie companies lurking on the ASX 300

Livewire Markets