TOL - 24th Oct, 2024

Citi downgrades ASX lithium sector earnings. This is its only remaining buy

Citi has revised its lithium forecast, noting a “cautious approach”. This means downgrades for some ASX lithium stocks within its coverage.

Major broker Citi has just released a new research note on the Australian lithium sector outlining its reasons for downgrading its earnings forecasts for several producers and developers within its ASX lithium coverage.

The broker notes it now has only one BUY-rated pick – a relative minnow compared to the major producers. In the big caps, a stock it presently rates as NEUTRAL remains its “preferred name”. Let’s unpack the rationale behind Citi’s revised lithium outlook as well as the broker's changes to its earnings forecasts for its ASX lithium coverage.

“Cautious in the short term” on lithium mineral prices

Citi notes that its global commodity team remains “cautious in the short-term” over the prospect of a recovery in lithium minerals prices. The main reason is that lithium carbonate production has “trended up” even despite some destocking during the September-October peak season.

The production increase has occurred despite the recent announcement by Contemporary Amperex Technology Co. Limited (CATL), the world’s largest producer of lithium-ion batteries for EVs, that it would suspend production at its lepidolite operations in Jiangxi province. Chinese lepidolite production is widely viewed as a key source of marginal swing production in the lithium minerals market.

Citi analysts aren’t taking CATL’s production cuts all that seriously, “the majority of the supply cuts can be restarted should pricing improve”, the broker notes. This would likely cap “near-term upside”.

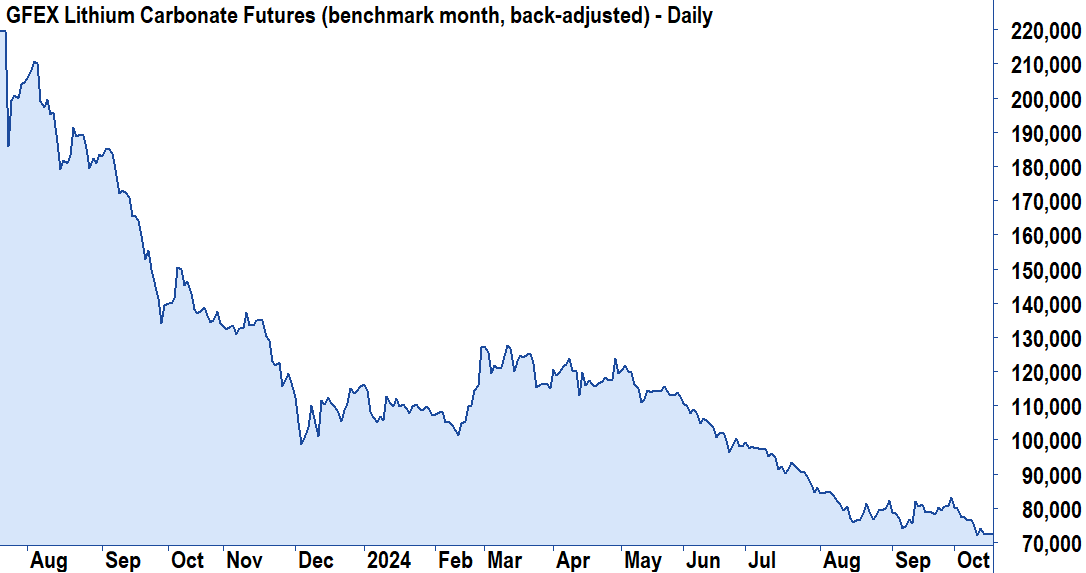

Lithium prices staged a very brief recovery after the CATL announcement, which occurred around the same time battery producers tend to be stocking up in the lead-up to Chinese New Year. As can be seen from the chart below, however, prices are again slumping back to multi-year lows.

%20chart%2021%20October%202024.png)

Whilst the supply side of the lithium minerals equation may continue to be hampered in the near term, Citi notes that the demand side – China EV battery consumption – has been a “bright spot”. The broker has revised up its pure EV (i.e., battery as the only source of power “BEV”) forecasts for the country by 3% for 2025 and by 11% for 2026.

This “pales in comparison”, says Citi, to the increases in its forecasts for hybrid and plug-in hybrid (“PHEV”) vehicles. Combined, these EV classes received an upgrade of 30% in 2025 and 18% in 2026 from the broker.

Still, the growing preference for non-BEV options among Chinese consumers is a double-edged sword, notes Citi. A lack of charging infrastructure, range anxiety, and China’s auto trade-in policy are driving consumers towards these less-lithium intensive EVs.

Further, looking abroad, a trend towards austerity in some European countries has led to the withdrawal of government incentives, therefore hampering EV penetration rates. At around 15% and holding, European EV penetration is “300-400 bp” lower than Citi’s auto team had forecast 12-18 months ago.

The arrival of new, cheaper models aimed at the EUR30,000 price point should help boost demand next year, says Citi, but the broker notes its European auto team “still sees risks to the downside” for European penetration out to 2030, which it now sees at 40%.

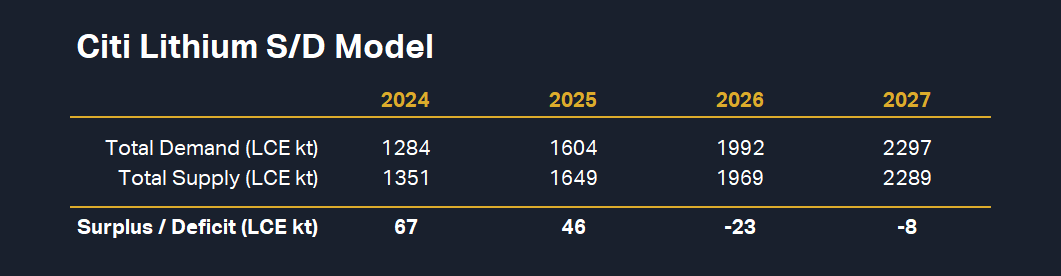

Pulling all of the threads together for us, Citi concludes that renewed weak pricing may ultimately be the cure for weak pricing, that is, it will do enough to disincentivise industry production and pull forward the brokers forecast supply deficit to 2026.

“Current pricing is not profitable for the majority of producers as our lithium cost curve work highlights”, the broker notes, adding “Funding new projects is challenging against this backdrop”.

What about ASX lithium stocks?

The tweaks to Citi’s lithium price forecasts have translated into earnings forecast changes for several ASX-listed lithium producers and developers within its coverage. The broker notes that its near-term cautiousness towards the lithium price is “reflected in our stock ratings”.

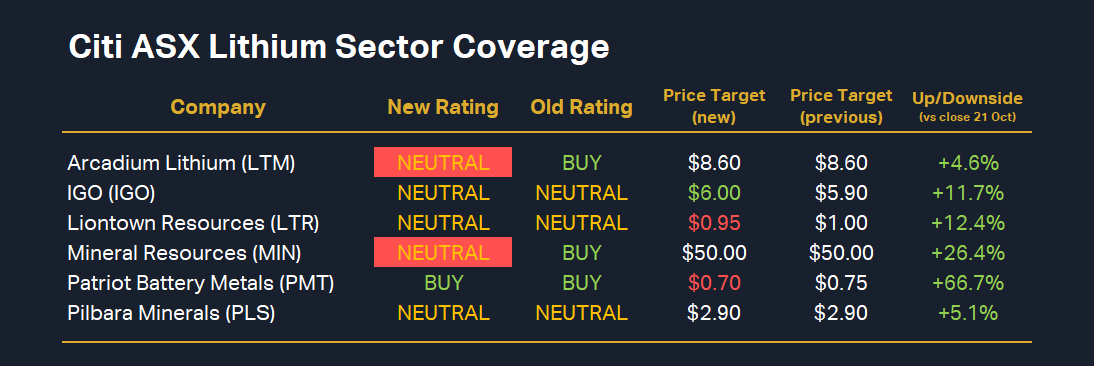

This means a downgrade in the broker’s ratings to NEUTRAL from BUY for Mineral Resources (ASX: MIN) and Arcadium Lithium (ASX: LTM), as both stocks are “now trading close to our unchanged price targets”, notes Citi.

Various ratings for Liontown Resources (ASX: LTR), Patriot Battery Metals (ASX: PMT), Pilbara Minerals (ASX: PLS), and IGO (ASX: IGO) were left unchanged, however, LTR and PMT saw moderate cuts to their respective price targets, while PLS was left unchanged, and IGO saw a very small increase. The changes to Citi’s ASX lithium coverage are summarised in the table below.

Despite PMT remaining as Citi’s only BUY-rated ASX lithium stock, the broker notes that PLS is its “preferred name” for larger capitalisation lithium exposure.

PLS is the “most exposed to any change in market sentiment such as an EV stimulus”, Citi notes, adding “We see the stock as the cleanest exposure to lithium in the ASX200”. Whilst Citi likens PLS to “the lithium ETF” of the ASX200, it still saw fit to cut EBITDA forecasts for the stock by over 40% in FY26-FY27.

The final and possibly most interesting observation Citi makes in its research note is with respect to whether the sector deserves a more general re-rate due to Rio Tinto’s (ASX: RIO) takeover of LTM. The short answer is ‘no’.

Citi has plugged in bid metrics to other ASX lithium names and could not find any reasons to support a re-rate. “In our view, LTM was the only target for a major looking for lithium scale, low-cost position”, the broker notes.

If they squint, however, Citi does see some “corporate appeal” in PMT given that company’s highly prospective projects in the Eeyou Istchee region.

This article first appeared on Market Index on Tuesday 22 October 2024.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

%20chart%2021%20October%202024.png){kind=link}

{kind=link}

{kind=link}

5 topics

6 stocks mentioned

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment