Costa Group: How does it stack up against its peers?

Costa is Australia’s leading grower, packer and marketer of premium quality fresh fruit and vegetables. Their produce is supplied to all the major Australian supermarket chains, as well as independent grocers and a range of food industry stakeholders.

They also export to Asia, North America and Europe. As a fresh produce producer and supplier, all year round, they have forged strong relationships with strategic alliance partners.

These growers supplement and extend the offering provided by Costa’s own farms. In addition, Costa Farms and Logistics operates wholesale markets for fresh produce and provides value added supply chain and logistics services. Costa has key business segments; Produce (including Mushroom, Berry, Citrus, Tomato, Avocado), Logistics & Licencing as well as International (Morocco, China).

FY18 Result (& Moroccan Blueberry Issues)

Costa Group reported an underlying FY18 Net Profit After Tax after Significant items (NPAT-S) growth of 26.3%however missed expectations by 5% on the back of a poor harvest in the group’s Moroccan Blueberry business. The miss was supposedly due to a 1 in 40-year weather event. Morocco experienced prolonged cold weather throughout spring and early summer causing an eight-week delay in crop maturity and a shortened harvest period As such, Costa’s International division saw EBIDTA fall by -8.4% on FY17.

Positively, the produce division outperformed expectations and management guided to “low-double-digit" net profit growth over the next 3-5 years. Result highlights:

- Revenue growth of 10.2% on FY17 to $1 billion ($1b revenue milestone)

- EBITDA before material items growth of 30.9% to $150.8m

- EBITDA margin improvement from 12.7% to 15.0%

- NPAT before material items growth of 26.3% to $76.7m

- Leverage at 1.2x EBITDA with Net Debt of $176.1m and increase of 91.9% primarily due to the payment for African Blue acquisition

- Final Dividend of 8.5 cents per share, fully franked (full year 13.5 cps) up 22.7%

Future Growth

Berry Expansion

Berry expansion plantings across Australia, China and Morocco continuing on track. Tailwinds are expected due to a 10% (97ha) increase in new plantings in FY18. In FY19, Costa has outlined a panting program of an additional 45ha of berries. Further benefits will come via the ongoing volume shift to ‘shoulder periods’ which are outside the usual seasonality of berry production and attract a higher margins. This is achieved by geographically diversifying their production footprint. Also, and the new Arana premium berry products attract a 20% price increase.

Avocado Vertical Integration

CGC has become the fifth largest avocado producer and largest marketer in Australia. Costa is well on their way to establishing avocados as its 5th vertically integrated produce category with 6 acquisitions completed over the past 18 months. Management has stated they have not finished making acquisitions and will likely be active in M&A over the next 18 months. Next year Costa will account for around 20% of the total avocado market (not including potential acquisitions). Key goal has been to diversify growing regions to enhance seasonal coverage as well as sourcing produce from third parties (reducing risk).

Mushroom Expansion

The Monatro mushroom farm expansion is going to plan. The project was announced in Feb17 with the intention of doubling the current facility capacity of 120 tonnes to 240 tonnes per week. The project will cost $71m in total with and will be complete in Q3 2019; $15m has been spent to date with another $57m over the next 12 months. Costa is expecting roughly 20% Return on Invested Capital (ROIC) p.a. over the next 5 years. According to management, the mushroom market remains undersupplied, which should lead to higher prices.

Tomato Glasshouse Expansion

In August the Board approved construction of a further 10ha glasshouse for snacking tomato production (higher margin products). The new 10ha will provide optionality to internalise production that is currently outsourced to 3rd party glasshouses. The project will also encompass expansion in nursery capacity and enhanced packing capability across Costa’s total 40ha of tomato production. The expansion will cost $67m and will be funded from cash flow and debt, with production expected to begin in May 2020; management is targeting 15% ROIC within 5 years.

International Growth Projects

China; Costa’s expansion into China is progressing well, with 100ha of berries planted by the end of FY18 (blueberry, raspberry, and blackberry planted across 3 farms). Management have reiterated their plans for an additional 246ha of Chinese plantings over the next few years with 65ha to be planted in FY19 at a cost of $31M.

Morocco; Expansion remains strong with 294ha worth of berries planted by the end of FY18, increasing by 15%. Costa now has 6 farms and has diversified into southern Morocco for season extension.

Our view

Broadly speaking, we view management's ambition to provide Australian retailers with 52 weeks supply across its 5 key segments (mushrooms, tomatoes, citrus, berries and avocados) as positive and believe that Costa is making good progress to achieving this goal.

They have been investing in international and domestic geographical diversification allowing them to grow all of their 5 key produce segments at any time of the year. Another positive growth catalyst is Costa’s continued exposure to the higher growth snacking category (e.g. Arana premium berry products), which now account for 25% of planted volume.

Notwithstanding that over 50% of production is under greenhouses (berries, mushrooms and tomatoes), there is still one clear structural risk facing the business; exposure to weather events as witnessed by the recent weather events in Morocco . However they are doing a good job of minimising impacts by diversification.

Financials and Outlook

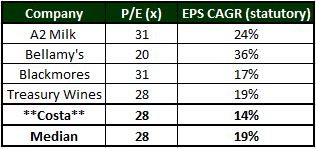

Although we believe Costa has a good growth story over the long term, at current values the company looks to be trading in line with its ‘’high growth’’ peers.

Notwithstanding the recent share price depreciation, the business is still trading on a FY19 forward P/E of 28x and it appears that the future growth is being priced in. Also, to fund ongoing expansion, Costa is taking on large amounts of debt with net debt increasing 91% over FY18.

Costa Group vs. Peers (with Chinese exposure)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

1 stock mentioned

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Comments

Comments

Sign In or Join Free to comment