COVID’s winners and losers in Australian real estate

Since the onset of the COVID-19 pandemic, the listed property sector has been amongst the most impacted. The S&P/ASX 300 A-REIT Index was down 35% in March before recovering 20% in the June quarter as restrictions were eased. The majority of the volatility was driven by discretionary retail landlords, which dominate the Index and are now trading at 40%-50% discount to NTAs.

This highlights the risks in the Australian Real Estate Investment Trust (AREIT) index, which is highly concentrated with the top 8 stocks making up more than 80% of its market capitalisation, and heavily biased towards retail assets.

There are 2 key benefits from investing outside the index into “alternative” real estate sectors;

1. Diversification from the traditional core sectors such as retail, office and industrial

2. Long term sustainable growth driven by secular trends

Diversification has never been more important; we saw how COVID-19 clearly impacted sectors which rely more on social gatherings, than others. COVID-19 has also accelerated previous structural changes, such as the adoption of on-line retail and more flexible working environments (such as WFH). These structural changes create new investment opportunities into logistics warehouses for example, which form part of the supply chain for on-line retail. Online penetration in Australia is expected to rise from 11% to 19% by FY24. We believe this will put further pressure on physical stores with vacancies expected to increase, and rents forecast to fall by 20% for discretionary shopping centres.

Data centres are another good example, as demand for social media, on-line transactions, streaming and cloud computing increases. Cisco is forecasting global data centre traffic will triple from 6.8 Zettabytes in 2016 to 20.6 Zettabytes in 2021, with the majority of the growth from the adoption of cloud computing. In fact, Cisco estimated that 94 percent of workloads and compute instances will be processed by cloud data centres by 2021. This trend is further accelerated by the surge in data storage and processing requirement resulting from increased levels of remote working.

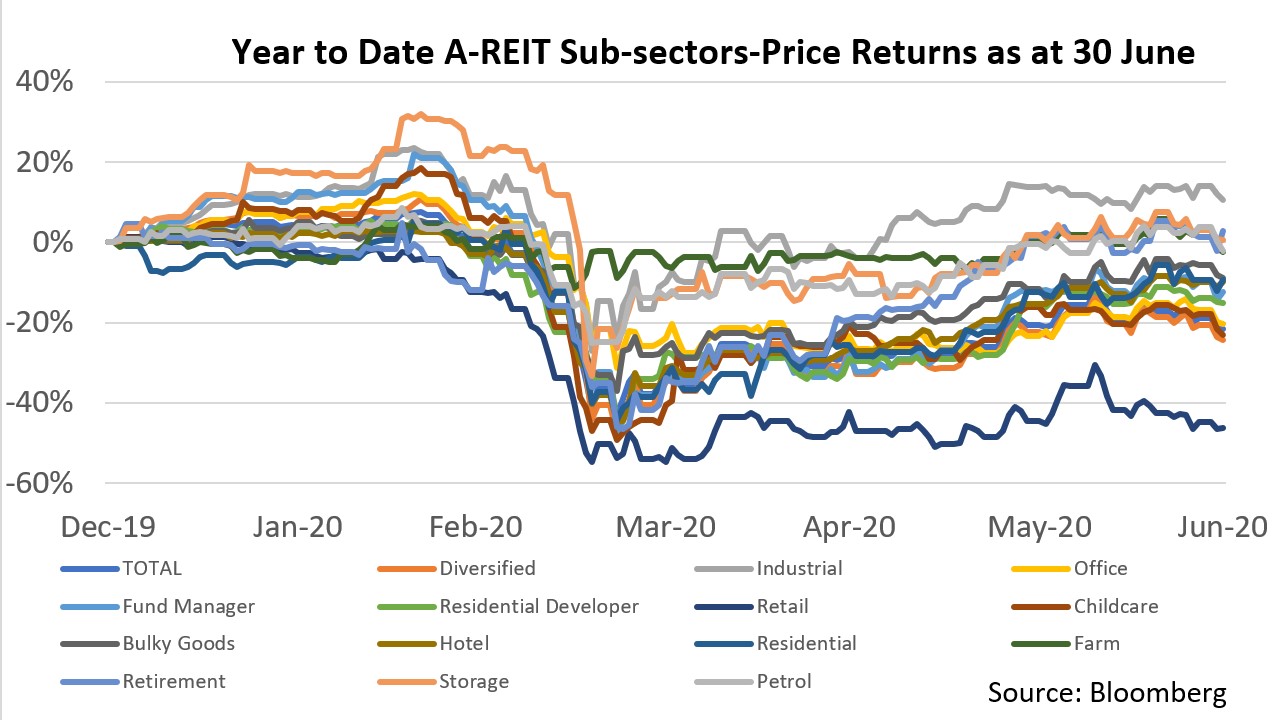

The need for diversification can clearly be seen when deconstructing the performance of the A-REIT market during the pandemic. Performance amongst the sectors differed considerably, with retail and residential sectors being most impacted, whilst industrials, fund managers, farms and storage were more resilient.

Looking at the longer-term impacts of the pandemic, there will be a cyclical headwind from higher unemployment, lower GDP growth and a consequent impact on tenant demand, vacancy rates and market rents. Typically, the core sectors such as retail (particularly discretionary), office and industrial are more cyclical and tend to perform in line with each other. Alternative real estate sectors tend to be less cyclical as they are driven by secular and structural trends. These secular trends, such as increasing urbanisation, ecommerce, ageing population, immigration and climate change, underpin property demand in sectors such as childcare, seniors living, healthcare, data centres, transport and agriculture.

In addition to providing diversification and less cyclical earnings, alternative property sectors may also provide more defensive earnings streams as they typically have longer lease terms. For example farms have a weighted average lease expiry (WALE) of 12 years, petrol stations of 11 years, childcare centres of 12 years and data centres of 12 years, compared to core asset classes of 4 to 6 years.

The outcome of the pandemic is fluid in the short to medium term, with the risk of further outbreaks in the longer term. In the face of this uncertainty, one must remain focused on building a portfolio that provides capital security and income yield. The ability to invest outside the index into alternative real estate sectors broadens the investment universe and further enhances the ability to deliver on such investment objectives.

Learn more

Stay up to date with my latest high conviction opportunities in the property sector by hitting the follow button below. or contact us to learn more about the Pengana High Conviction Property Securities Fund.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Amy is portfolio manager of the Pengana High Conviction Property Securities Fund, and has over 20 years of property funds management experience.

Previously, Amy has worked at Charter Hall/Folkestone for 6 years, managing a high conviction AREIT strategy. This team won several industry awards including Financial Standards Property Fund Manager of the Year 2019, Money Management/Lonsec Australian Property Securities Fund Manager of the Year 2018, and Financial Standards Property Fund Manager of the Year 2017.

Amy has held several senior positions including head of property securities at IAG and portfolio manager at Deutsche Asset Management and Perpetual Funds Management. She began her career as a quantitative analyst at Legal & General.

5 topics

Amy is portfolio manager of the Pengana High Conviction Property Securities Fund, and has over 20 years of property funds management experience. Previously, Amy has worked at Charter Hall/Folkestone for 6 years, managing a high conviction...

Expertise

Amy is portfolio manager of the Pengana High Conviction Property Securities Fund, and has over 20 years of property funds management experience. Previously, Amy has worked at Charter Hall/Folkestone for 6 years, managing a high conviction...

Expertise

Comments

Comments

Sign In or Join Free to comment