Currency hedging - what to consider

When investors choose to invest internationally, they need to consider the implications of movements in the Australian dollar relative to the associated foreign currency exposure.

As a baseline, investors who think the Australian dollar is likely to increase should currency hedge and those that are bearish should remain unhedged. To form a decision, investors should consider the following points.

Investment time horizon

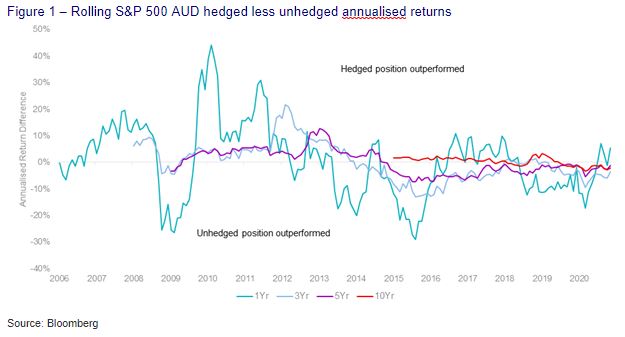

Investment return differences between currency hedged and unhedged equity exposure are more volatile over shorter periods. It may be tempting to try to influence returns by timing the exposure to a currency but there is material downside risk over the short term if the outcome is different to that expected. Over the long term, differences between currency hedged and unhedged returns diminish. The graph below illustrates differences between AUD currency hedged and unhedged annualised returns for US exposure represented by S&P 500 over various periods.

Timing the entry and exit point

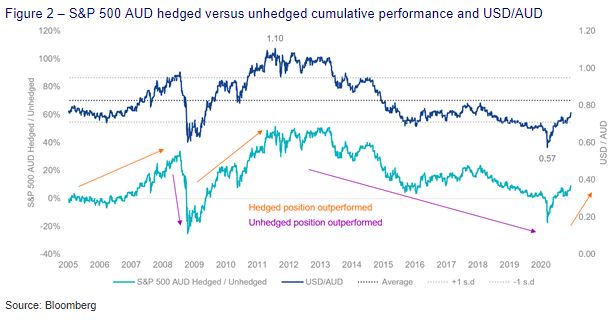

The Australian dollar has oscillated between 0.57 and 1.10 US dollars over the last 15 years. When deciding whether to currency hedge or not it is important to consider where you think AUD is valued now relative to your end investment time. If you think AUD is at the lower (upper) bound, you should hedge (not hedge).

Likewise, if you think AUD will be valued at a similar level to your end investment date, you should be indifferent to taking a hedged or unhedged currency position. Below is an illustration of how AUD/USD currency movements has influenced S&P 500 AUD hedged and unhedged returns.

Diversification benefits

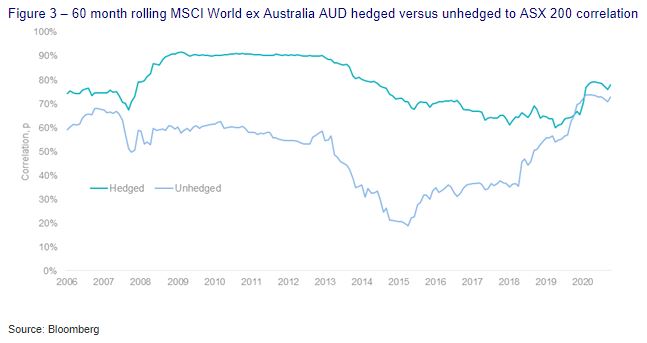

Unhedged currency international equity exposure has historically provided more diversification benefits, illustrated by having a lower correlation to Australian equity returns compared to international currency-hedged exposure. Below is a comparison of AUD hedged and unhedged international equity correlations to Australian equity returns represented by MSCI World and ASX 200 respectively.

Type of international exposure

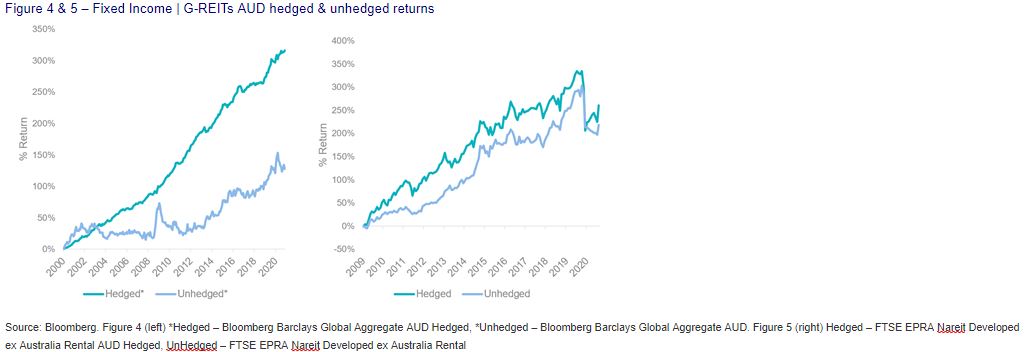

Market consensus is to currency hedge exposure of high-income, lower volatility assets, such as global fixed interest, infrastructure and REITs. Income-producing assets’ cash flow is largely sourced domestically so it makes sense to remove currency exposure. Currency-hedged exposure has historically produced stable returns as shown below.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Russel is Head of Investments and Capital Markets at VanEck in Australia. An actuary with over 25 years’ experience in financial services, specialising in asset and wealth management.

........

Issued by VanEck Investments Limited ACN 146 596 116 AFSL 416755 (‘VanEck’). This is general advice only, not personal financial advice. It does not take into account any person’s individual objectives, financial situation or needs. Read the PDS and speak with a financial adviser to determine if a fund is appropriate for your circumstances. PDSs are available here. No member of the VanEck group of companies guarantees the repayment of capital, the payment of income, performance, or any particular rate of return from any fund.

3 topics

Russel is Head of Investments and Capital Markets at VanEck in Australia. An actuary with over 25 years’ experience in financial services, specialising in asset and wealth management.

Russel is Head of Investments and Capital Markets at VanEck in Australia. An actuary with over 25 years’ experience in financial services, specialising in asset and wealth management.

Comments

Comments

Sign In or Join Free to comment