Deep Diving For Asymmetric Upside - New Idea

A lot can be said for understanding what you own, and why you own it. Investors look at stocks like Afterpay, Appen, Altium or A2 Milk and dream of finding such companies before the crowd. While difficult, it is not impossible.

To find investments like these early on it requires tremendous foresight and a deep dive to understand how these companies’ products or services could grow. To do this, investors need a detailed understanding of the business model and what sets such companies apart. What is their moat, and why has the broader market not caught on yet?

If there is a fundamental problem a company successfully solves, it usually results in a rapid appreciation in share price. When there is high demand for a service/product accompanied by a strong moat (i.e. no or limited competition) it typically allows companies to scale up revenues and profit exponentially. As the investment crowd starts to take a deep dive on such companies, the demand for the product or service offered then becomes a demand for the company shares and the corresponding share prices tends to appreciate rapidly.

We believe we could have identified one such opportunity. A product with huge potential demand, a significant moat and the ability to scale and grow exponentially.

That company is Paradigm Biopharmaceuticals (PAR.ASX)

Paradigm is repurposing a drug called Pentosan Polysulfate Sodium (PPS) and its leading indication is in the multibillion-dollar disease of Osteoarthritis (OA). Our recent research outlines the significant moat we believe investors have missed around the exclusive supply agreement Paradigm has with the only FDA approved supplier of PPS - bene pharmaChem. Many investors seem to believe PPS is an easily accessible generic drug and therefore, they discount Paradigm. However, this is not accurate.

In fact the situation with PPS is very unique and to understand this ‘generic’, a deep dive is required. What most perceive as a risk, is actually a significant moat. PPS is a generic in the same way A2 Milk is just like other milk – a deeper understanding is needed before making such assumptions.

Image of bene pharmaChem facilitity that we visited while researching PPS & Paradigm on due diligence trip to Germany

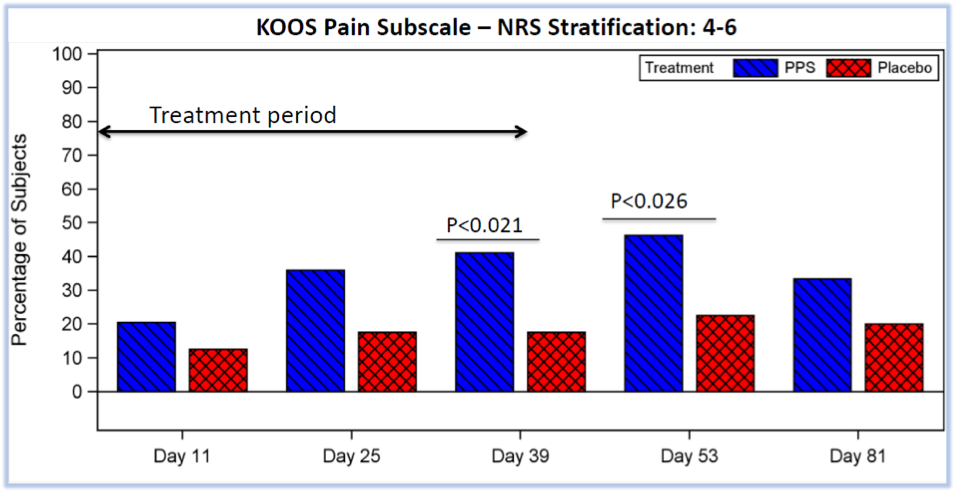

Paradigm has recently passed a Phase 2b trial for their headline indication - OA. This means the company has passed a major hurdle and is now one step closer to successfully commercialising their OA drug (Zilosul®). Current treatment for OA is very limited and as the disease progresses, it would usually result in surgery to replace joints. With limited treatment options for OA, the early indications are pointing towards Zilosul® becoming a blockbuster drug (selling over $1b per year in product revenue).

Statistically significant results meeting the primary endpoint from Paradigm’s recent Phase 2b placebo-controlled trial using Zilosul® to treat the blockbuster indication of OA.

Paradigm has also collected significant real-world evidence by treating patients in Australia under the TGA's Special Access Scheme (SAS). So far Paradigm has treated over 500+ patients under the SAS (more results to be released), purely from word of mouth and positive experiences from treatment. People are already ‘lining up’ for a repeat dose, which is a great sign that patients are seeing a positive impact from treatment. This also highlights the critical unmet need and lack of effective treatment options for people suffering from OA.

Something else people don't realise is that Paradigm may soon receive "Provisional Approval" under a new regulation implemented TGA in Australia (this regulation allows drugs to be sold commercially prior to being formally approved if the TGA deem the benefit of providing the medicine outweighs the inherent risks). This approval would allow Paradigm to bring Zilosul® to market prior to completion of their Phase 3 trial. Given the significant number of patients already being treated under the SAS program, and that Zilosul® had no serious adverse events in the recently successful phase 2 trial, we believe Paradigm is a good chance of receiving such approval. This could mean first revenues as soon as next year (2020).

We believe that Paradigm could price Zilosul® at around $2500 per 6-week course of treatment. With over 2.1 million people in Australia suffering from OA and around 550,000 of those reporting as "poor/fair condition" we believe the sales of Zilosul® could ramp up very quickly. Treating only 10,000 people in the first year, Paradigm could generate $25m in revenue. As the treatment lasts for around 6-12 months on average it would result in those deeming it successful to seek follow up treatment (as is being seen in the SAS program). This is a drop in the ocean when looking at the global market of people suffering from OA and is a potential blockbuster revenue opportunity for Paradigm.

The biggest pharmaceutical market in the world is the USA and Paradigm have their sights firmly set on this market. This year they plan on treating 50 ex-NFL players with Zilosul® in an American version of the SAS program. If they can replicate the success, they saw with ex-AFL players in Australia, it would likely garner significant media attention and propel Paradigm onto the big stage.

Super Bowl star Todd Gurley (contracted for $57.5m) has just learned he has an arthritic knee. Successful treatment of such players will garner a lot of media coverage in the USA as it did with AFL players in Australia.

A non-opioid treatment for OA is considered the holy grail, and many big pharma companies have attempted the last crusade to find it - so far with limited success. The most comparable drug in clinical trials is an anti-NGF (Nerve Growth Factor) drug called Tanezumab which was valued at US$1.8b when the deal was struck (a partnership between Pfizer & Eli Lilly). When comparing the results of Tanezumab to Zilosul® it looks very similar in terms of efficacy towards pain, but Tanezumab had a higher level of adverse events. The adverse events are a major issue for Tanezumab that is likely to impact its commercial success (i.e. patients and clinicians are likely to be cautious in using & recommending the drug if it has material side effects).

Paradigm will likely use this deal as a benchmark for any Big Pharma deals when looking at partnering for their upcoming Phase 3 trials. (e.g. if Zilosul® will outsell Tanezumab should both reach commercialisation which one would a Big Pharma rather own?).

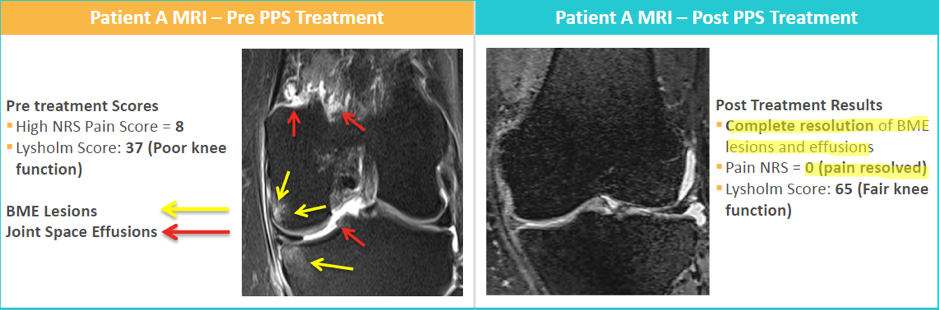

While Paradigm has so far released their Phase 2 top line OA results, they are expecting to release the secondary endpoints from the trial by the end of March. If Paradigm’s secondary endpoints can also show that Zilosul® is reversing the effects of the disease in the MRI data, this would be a major scientific breakthrough when compared to the NGF drugs (i.e. not just treating symptoms but acting on the cause of the problem).

MRI scans previously released showing PPS impact on potentially reversing the cause of OA as well as treating symptoms, a major breakthrough if it can be replicated in secondary data from phase 2 clinical trial.

So, while the risks for the business have materially decreased due to the success in the phase 2 trial, the share price has yet to respond as you would have expected. We suspect that the market conditions at the time the results were released (just prior to Christmas) and a lack of understanding around the business are potential factors.

But ultimately, Paradigm appears under the radar of most investors. As more begin to take the deep dive and understand the pipeline ahead, it feels like the company will begin to re-rate in line with other high growth companies that have strong moats and multibillion-dollar revenue opportunities.

Should the company sign a billion dollar deal this year to fund their upcoming phase 3 trials, the market may very quickly understand the commercial significance of what they have achieved. Further to their OA indication, they have also got a pipeline of indications that appear to have a high chance of success in clinical trial, in particular their recent in-license for the indication of MPS.

While there are still risks in future clinical trials, the rewards look very asymmetric for investors with a little foresight. Successful phase 3 results and successful drug commercialisation in any of their indications will likely see Paradigm as the next Australian Blockbuster Biotech.

Disclosure: This is not a recommendation to buy Paradigm and investors should undertake their own research and discuss their financial position with a qualified advisor before purchasing shares in any company.

All views and information provided should be considered general in nature and are the opinion of Fiftyone Capital and are not to be considered statements of fact. Our fund owns shares in Paradigm and has previously received compensation in the form of options. As such any appreciation in the share price will result in financial gain for the fund and individual unitholders in the fund.

Please undertake your own research and seek profressional advice when considering if this information presented is relavant for your own situation.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott is the Executive Chairman at Fiftyone Capital. As the previous CEO, Scott founded the company to manage not only his own wealth, but the wealth of other investors and families looking for a safe harbour for their capital.

1 topic

3 stocks mentioned

Scott is the Executive Chairman at Fiftyone Capital. As the previous CEO, Scott founded the company to manage not only his own wealth, but the wealth of other investors and families looking for a safe harbour for their capital.

Scott is the Executive Chairman at Fiftyone Capital. As the previous CEO, Scott founded the company to manage not only his own wealth, but the wealth of other investors and families looking for a safe harbour for their capital.

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

This recently triggered market signal has never failed to predict gains

Ophir Asset Management