Defend and diversify: why bonds are critical in any portfolio

Chris Rands

Yarra Capital Management

COVID-19 has had many ramifications, including an increase in the number and size of the federal government’s debt programs. While these programs assist people and businesses that are struggling, they also need to be funded – and this is where government bonds come in.

Bonds are the way governments raise money. In the current environment, there’s strong demand for them – especially for the AAA-rated Australian bonds – and for very good reasons. Government bonds are the most liquid assets around, and much less susceptible to market volatility than equities. They also provide certainty over how much income you’ll make over the life of the investment, which is an important confidence boost in uncertain times.

But they have other attributes too. Which I provide a comprehensive overview of here, including where interest-rate movements fit in.

What are government bonds?

When governments spend more than they receive in revenues (taxes), they borrow money to fund expenditures. When a government wants to borrow, they sell (issue) a bond. The bond exists for a set period, e.g. three years or 10 years, and pays a set rate of interest (a coupon) during that period. At the end of the period, the original amount (the principal) is repaid. Bonds can be bought or sold on a market, and prices are set by supply and demand, so values can rise and fall.

The types of bonds available

Government bonds can be issued by any government globally, with the largest and most recognised market being United States Treasury Bonds. In Australia, the government bond market includes three broad groups of issuers:

- Australian Commonwealth Government Bonds (ACGBs) – These are bonds issued by the federal government and currently have an AAA rating. They are the most liquid securities and offer the lowest yield.

-

Semi-government bonds (Semis) – These are bonds issued by state governments (such as NSW) and are currently rated AA or AAA. They are slightly less liquid than ACGBs, but offer a higher yield.

-

Supranationals (Supras) – These are bonds guaranteed or supported by foreign governments and are typically rated A, AA or AAA. They are the least liquid of the government securities but are the highest yielding.

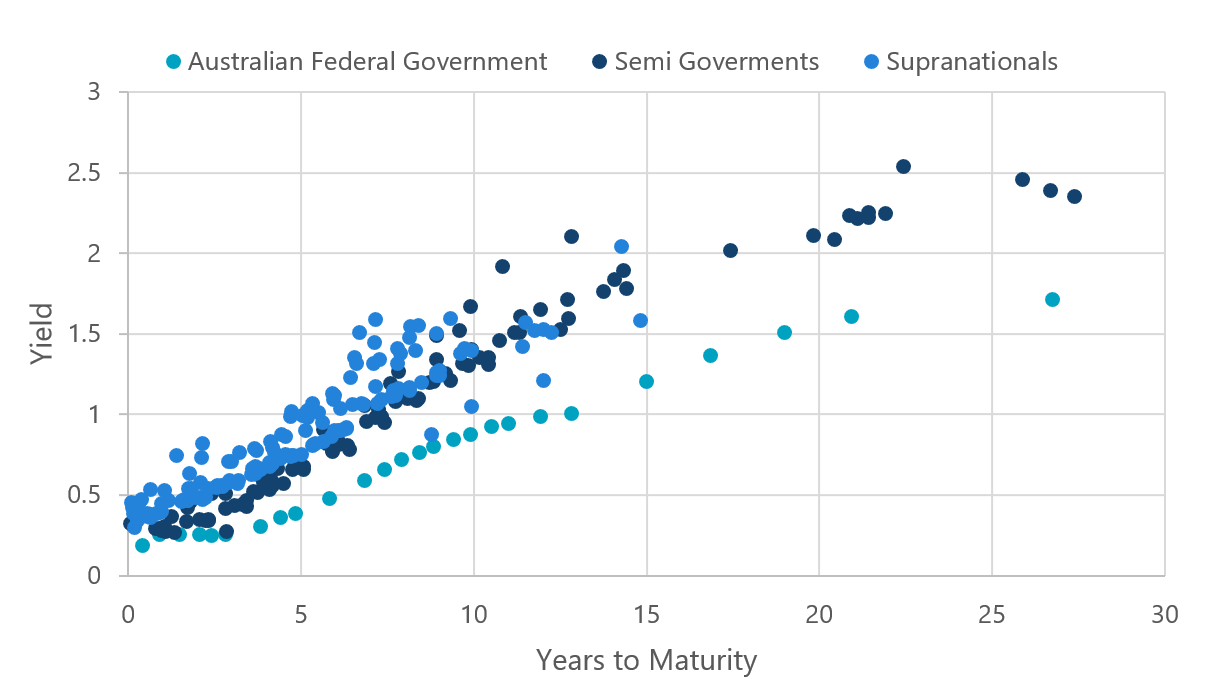

The government bond market is typically displayed as a yield curve, which is shown in Chart 1. On the horizontal axis are the years to maturity of the bond and on the vertical axis is the yield. Each dot represents a bond on issue.

Chart 1 – Australian government bond yield curve

Source: Bloomberg, Nikko AM

The role of government bonds

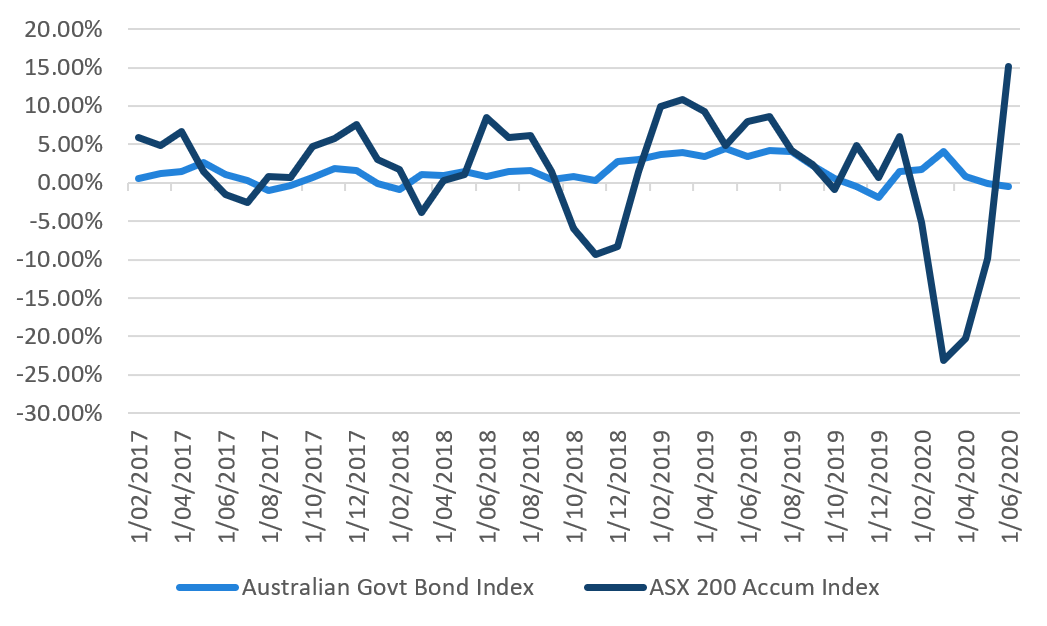

Government bonds are typically used as a defensive asset and to diversify against adverse moves in riskier assets, such as equities. While government bonds pay lower levels of interest than riskier assets, they are backed by the full faith of the government and hence have minimal risk of not be repaid. Typically when risk markets are performing poorly or economic conditions are recessionary, investors can sell assets with uncertain cash flows (such as equities) in order to move into lower risk investments like government bonds. An example of this can be seen during the March 2020 equity rout, where government bond returns were in low single digits while the ASX Accumulation Index fell over 20%. Furthermore, during this period the government bond market was one of the key asset classes used as a source of liquidity.

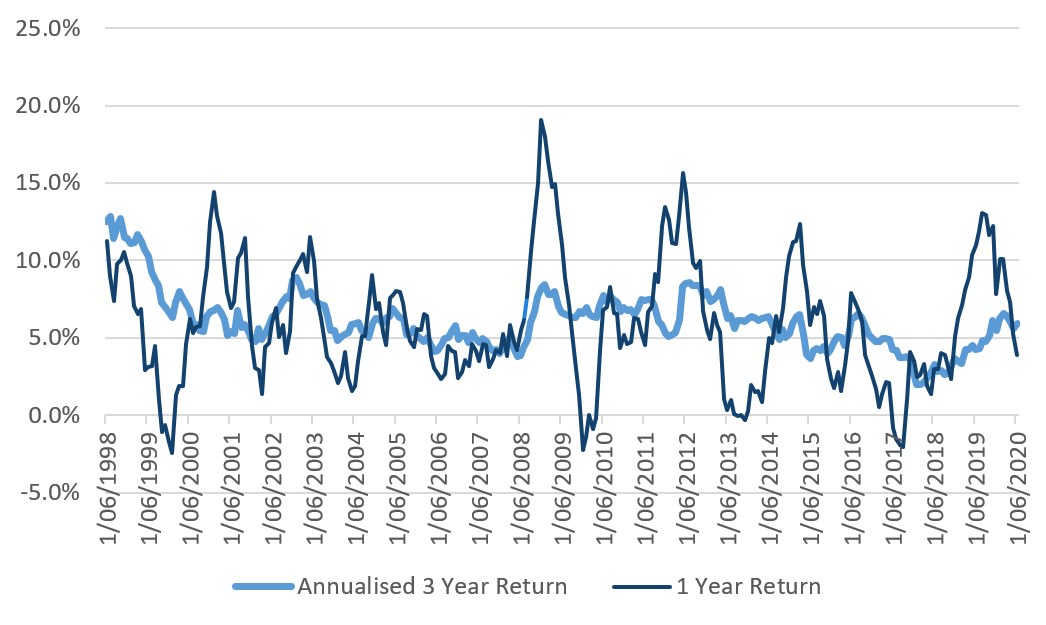

Chart 2 – Rolling 3-month returns

Source: Bloomberg, Nikko AM

Additionally, government bonds can be used as both capital protection and an income generating security. The capital preservation comes from the fact that it’s extremely unlikely for a government bond not to repay. This would require the government to default. In Australia, the government has never defaulted on the interest payments on its issued bonds or on the repayment of principal.

On the income side, government bonds pay periodic coupons, which are usually at a higher rate of interest than the cash rate, but a lower rate than riskier assets, such as corporate bonds or equity dividends. This makes them a more stable source of income for investors.

What returns to expect

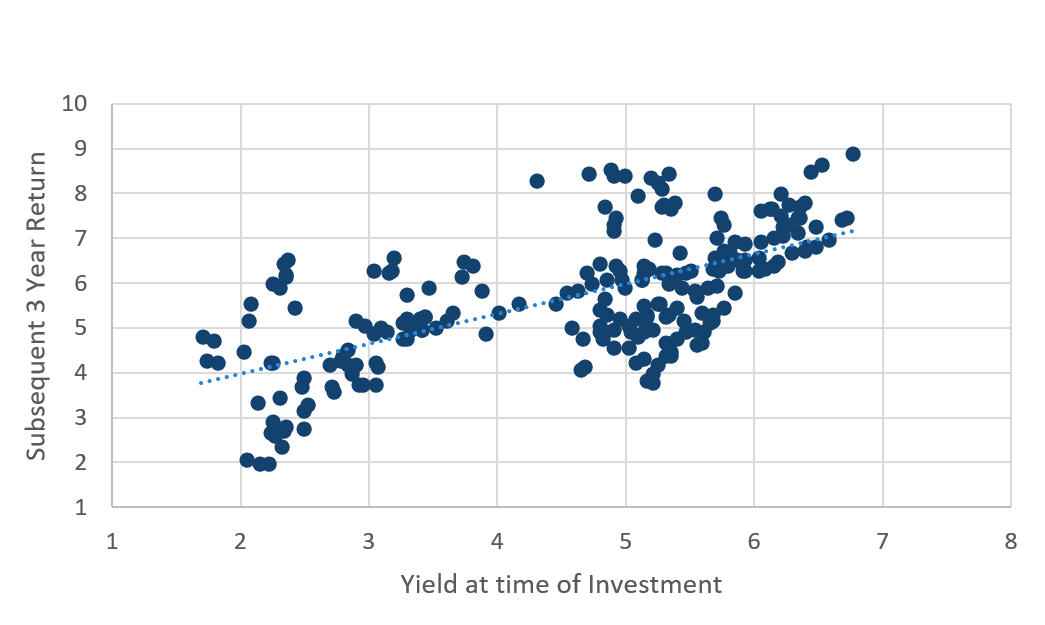

As the name of the asset class suggests—fixed income—the biggest component of returns over long periods of time will be the income that investors receive, as the capital amount paid at maturity (principal) does not change over time. Chart 3 demonstrates this by comparing the yield at which the government bond index was purchased (on the horizontal axis), with the subsequent annualised 3-year return (vertical axis). The upward sloping chart shows that the yield at which an investor purchases the asset class will go a long way in describing longer term returns.

Chart 3 – Year return on government bonds index

Source: Bloomberg, Nikko AM

This is because when a long-term investor buys a government bond, they will know in advance what they are set to receive. For example, if an investor were to buy $100 of a 5-year bond at par that pays a 2% coupon annually, they would receive $2 each year for five years and get $100 back at maturity. Regardless of what interest rates do over that 5-year period, the investor who holds to maturity has a degree of certainty around their expected return—in this example it’s ~2%.

Over the shorter term, however, government bond returns are affected by interest rate movements. These interest rate movements will affect the capital price of holdings. The longer the time to maturity the greater the effect.

Here is a simple way to think about it. Imagine if an investor invested $100 for 10 years at 5% and the day after interest rates rose to 6%. In this scenario, they would receive $5 p.a. while the market is offering $6 p.a. If they tried to sell the security (which is offering $1 p.a. less than the market) they would need to do it at a discount to compensate the buyer for the interest they are giving up. This creates a capital loss.

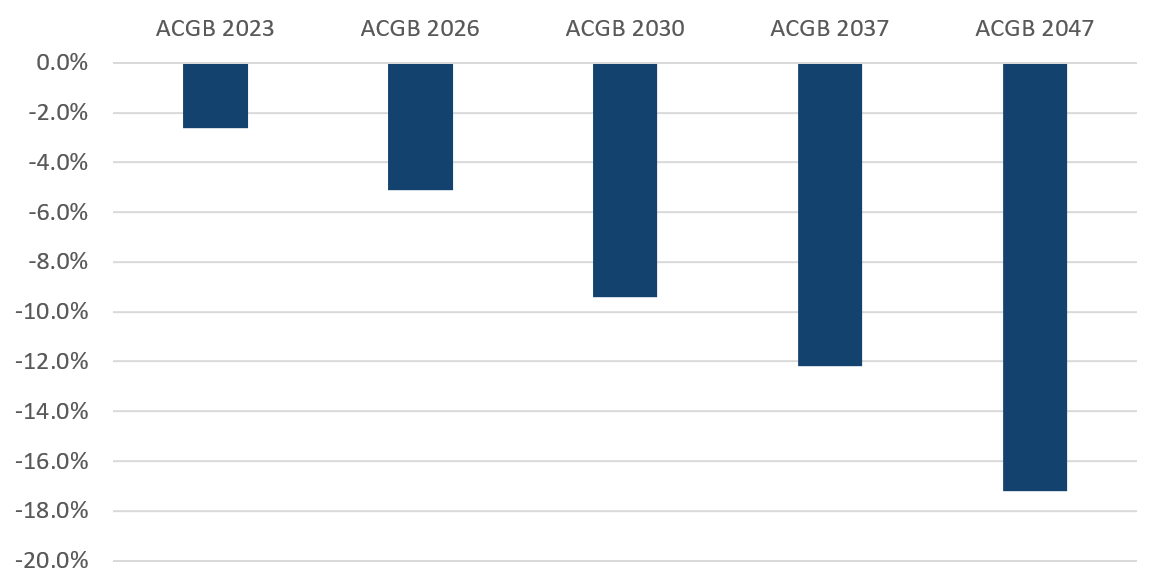

The longer they had locked in that 5% rate, the more this would cost to exit. Chart 4 shows the estimated price change on different maturity government bonds for a 1% increase in yields.

Chart 4 – Estimated price change of a 1% increase in rates

Source: Bloomberg, Nikko AM

Alternatively, if rates fell to 4%, they would have a 5% coupon when the market is only offering 4%. In this case, if they were to sell they would receive a premium—a capital gain.

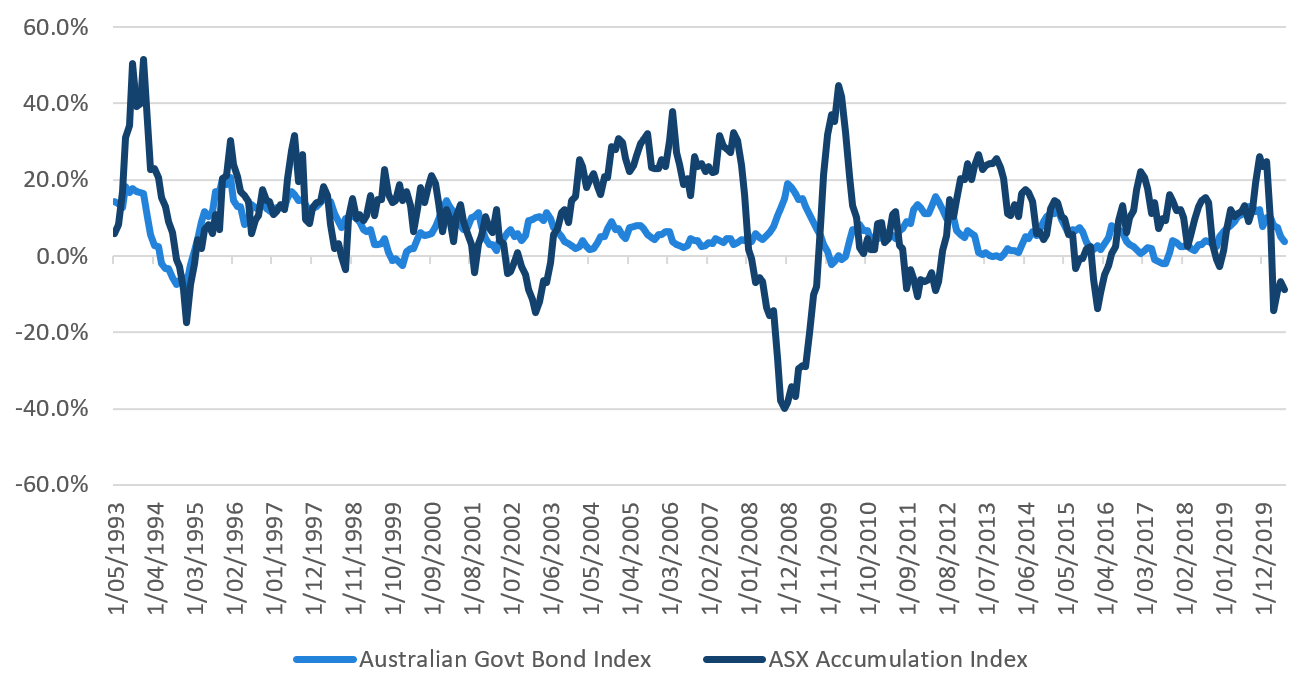

This is why it’s important to understand an investment horizon. Over short periods of time, government bond returns can be relatively volatile. However, over longer periods of time the returns move closer to the yield offered on the securities, as depicted by the return series in Chart 5.

Chart 5 – Australian government bond index return

Source: Bloomberg, Nikko AM

One of the most liquid assets in investment markets

In financial literature, government bonds are described as a ‘risk free’ asset and this certainly shows in the returns of the past 20 years. Over this period, there have been only five periods of negative year-on-year returns (1994, 1999, 2010, 2013 and 2017) with the worst return being -7.5%. The typical drawdown has been about -1 to -3%.

Chart 6 – Year-on-year returns

Source: Bloomberg, Nikko AM

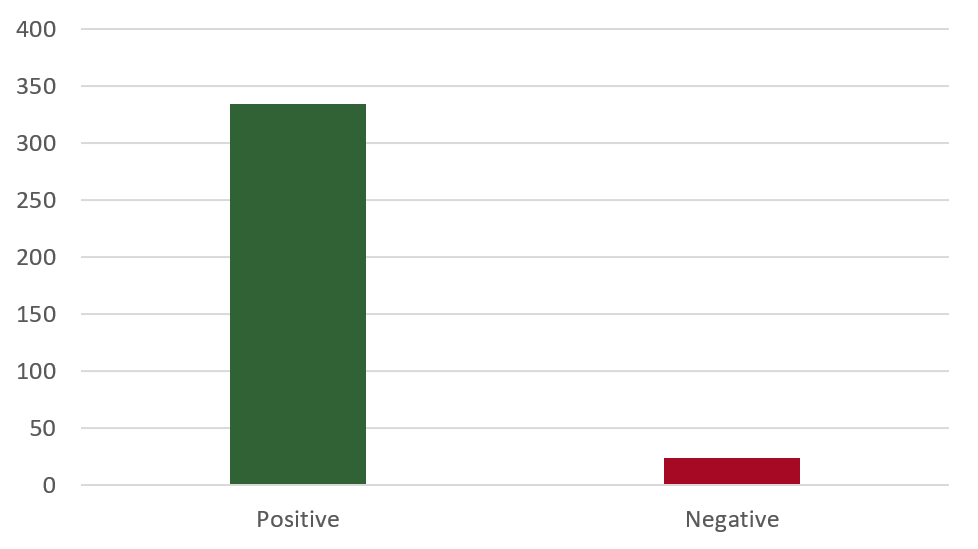

Over this 20-year period, there have only been 24 months of year-on-year negative returns compared to 334 months of positive year-on-year returns.

Chart 7 – Number of months with year-on-year returns

Source: Bloomberg, Nikko AM

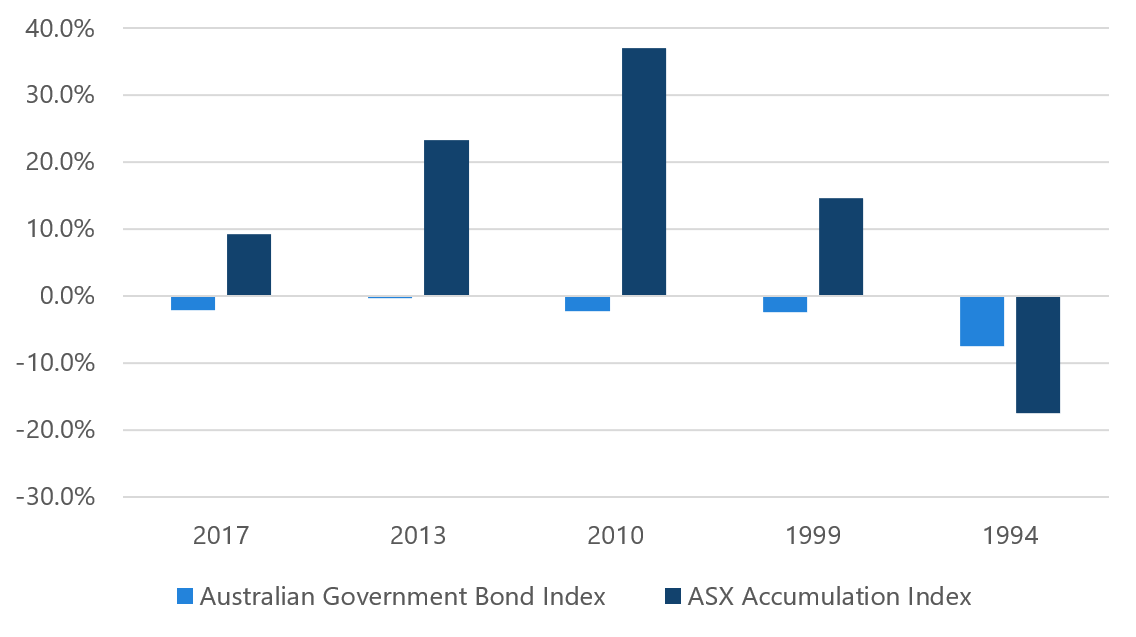

Looking forward, the key risk for government bonds will be if interest rates rise quickly and for a prolonged period of time. For interest rates to be rising, it implies a strong economy that would potentially bring with it positive equity market returns. Chart 8 provides an example of how this typically plays out, showing the year-on-year return of both Australian government bonds and the ASX accumulation Index at the point in time when bonds had their worse performance in that year. Only in 1994 did both bonds and equities exhibit negative returns at the same time.

Chart 8 – Asset class returns during the worst periods for bonds

Source: Bloomberg, Nikko AM

Government bonds are one of the most liquid assets in investment markets, allowing investors to buy and sell hundreds of millions of dollars in value at minimal cost. This is why government bonds were used throughout March this year for raising cash as markets were selling off—they are more liquid and so less expensive to sell.

When thinking of liquidity from extremely liquid to extremely illiquid, at one end would be illiquid real assets such as real estate, which can take months to sell with large commissions involved. At the other extremely liquid end is government bonds, giving investors access to hundreds of millions of dollars in liquidity, which can take only seconds to execute.

Stay one step ahead of the crowd

Unlike traditional duration and credit spread managers, we don’t have to rely on picking market direction to capture returns. Instead, we look for the best relative value between securities and sectors that will deliver consistent positive returns for investors. To find out more, use the contact button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris is responsible for portfolio management, including portfolio construction and trading for various Australian fixed income portfolios including the Nikko AM Australian Bond Fund at Yarra Capital Management (Nikko AM was acquired by Yarra Capital Management in April 2021). Chris has over 9 years of experience in the fixed income market. He is also co-host of the popular Australian podcast series The Rate Debate.

Featuring

Chris Rands,

Yarra Capital Management

Chris is responsible for portfolio management, including portfolio construction and trading for various Australian fixed income portfolios including the Nikko AM Australian Bond Fund at Yarra Capital Management (Nikko AM was acquired by Yarra Capital Management in April 2021). Chris has over 9 years of experience in the fixed income market. He is also co-host of the popular Australian podcast series The Rate Debate.

........

This material was prepared and is issued by Nikko AM Limited ABN 99 003 376 252 AFSL No: 237563 (Nikko AM Australia). Nikko AM Australia is part of the Nikko AM Group. The information contained in this material is of a general nature only and does not constitute personal advice, nor does it constitute an offer of any financial product. It does not take into account the objectives, financial situation or needs of any individual. For this reason, you should, before acting on this material, consider the appropriateness of the material, having regard to your objectives, financial situation and needs. The information in this material has been prepared from what is considered to be reliable information, but the accuracy and integrity of the information is not guaranteed. Figures, charts, opinions and other data, including statistics, in this material are current as at the date of publication, unless stated otherwise. The graphs and figures contained in this material include either past or backdated data, and make no promise of future investment returns. Past performance is not an indicator of future performance. Any economic or market forecasts are not guaranteed. Any references to particular securities or sectors are for illustrative purposes only and are as at the date of publication of this material. This is not a recommendation in relation to any named securities or sectors and no warranty or guarantee is provided.

Please refer to our Financial Services Guide for more information https://www.nikkoam.com.au/adviser/fsg

2 topics

Chris Rands

Co-Portfolio Manager, Fixed Income

Yarra Capital Management

Chris is responsible for portfolio management, including portfolio construction and trading for various Australian fixed income portfolios including the Nikko AM Australian Bond Fund at Yarra Capital Management (Nikko AM was acquired by Yarra...

Expertise

Comments

Comments

Sign In or Join Free to comment