Desknote: Veris Limited rebuild is gathering pace

Following recent management meetings, we think Veris could be a standout

microcap (VRS.ASX $0.075 Mkt Cap $30.4m). Looking forward, VRS

could be approaching

turnover toward $100m, and EBITDA of $10-15m, or 2-3x’s. They

are the largest

surveying company in Australia, and whilst not a "hot sector", we like the structural tailwind of both infrastructure,

resumption of residential/commercial construction and a focus on Defence

projects. They have the scale and presence to compete well for the larger

contracts. Following a significant restructuring, they are in a good position to

capitalise on this tailwind with lower debt and a structure

that sees margins improving across the business.

About Veris (VRS.ASX $VRS)

There are two divisions. 1. Veris Australia is a leading national surveying, digital and spatial and planning business. 2. Aqura Technologies is an industry leader in the provision of innovative technology solutions (think high end unified communications systems - as per the $1.9m Bunnings contract announced today).

Price History - 5 years tells the story of a restructure

Background – Painful – Lacked Execution - Back to their roots

- Veris was a roll-up of

several companies that encountered integration problems.

The new CEO Michael Shirley has been fixing the problems since late 2019.

- In a nutshell, managing a

largely East Coast rollup from an office in WA did not work.

It did not work geographically, and the roll-up execution did not

work as hoped. The main issue has been around the management of staff many of

whom work remotely in the field in challenging terrain with customers’

needs that are constantly changing. The delivery systems were poor and work was opened to being billed incorrectly (loss making). This issue has been

addressed with several management changes and some wholesale redundancies

of middle management and finance roles. The business in NSW slipped into

losses during this period but is now running back at breakeven following

the changes.

-

Elton

Consulting was a

profitable business acquired back in early 2018. Such was the breakdown in

the execution of the roll-up strategy, this business had to be sold in

late 2019 to shore up the balance sheet.

-

Instos

Lost – VRS

lost its institutional base, Perennial left back in June, and Paradice and

others in March/April.

- Michael Shirley has made a number of changes that have seen the business return to profitability despite the challenges of a Covid economy.

Looking Forward – there is plenty to start to like.

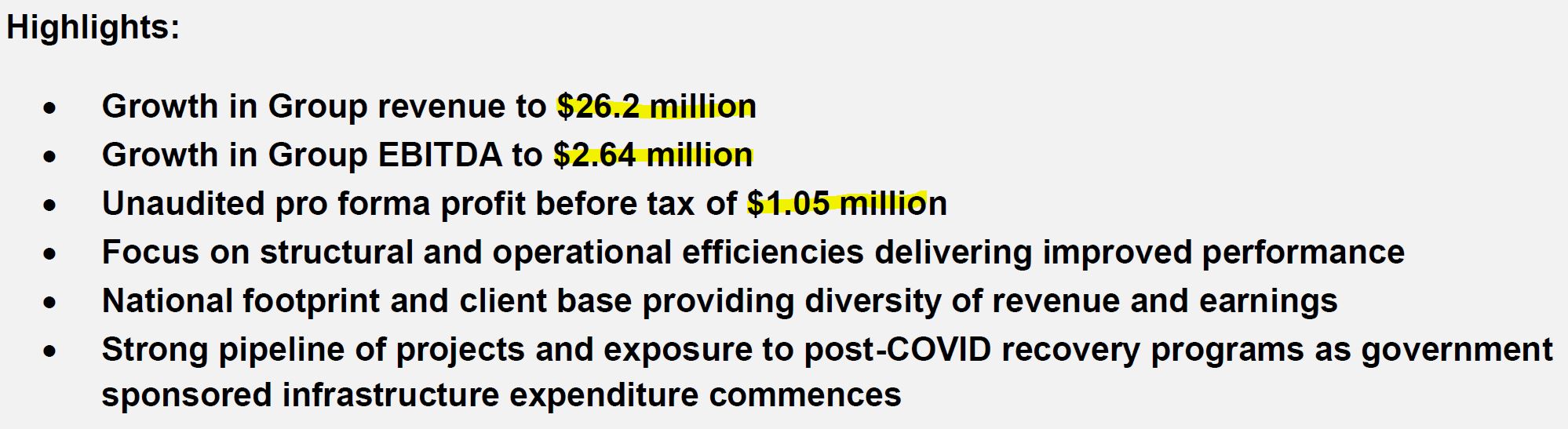

- An inflexion

point was the Q1 FY21

Update back in October – key highlights below – and

note this excludes uplift from any Jobkeeper payments. The backlog

of projects is $40m and the pipeline of tendered

projects over $80m.

Since that October update, they have secured $6.3m in announceable contracts

- Aqura Technologies - $2.0m contract to supply advanced LTE equipment for the Iron Bridge Magnetite Project, a joint venture between Fortescue Metals Group (ASX:FMG) subsidiary FMG Magnetite Pty Ltd and Formosa Steel IB Pty Ltd

- Veris - $1.2m contract over 5 months with APA.ASX to provide surveying and associated services for the new Northern Goldfields Interconnect (NGI) pipeline in Western Australia.

- Veris - $1.2m Defence Sector contract across projects in Victoria, New South Wales and Western Australia.

-

Aqura signed a

$1.9m contract with Bunnings (today) . The contract period will run 3 yrs

with a 2yr option.

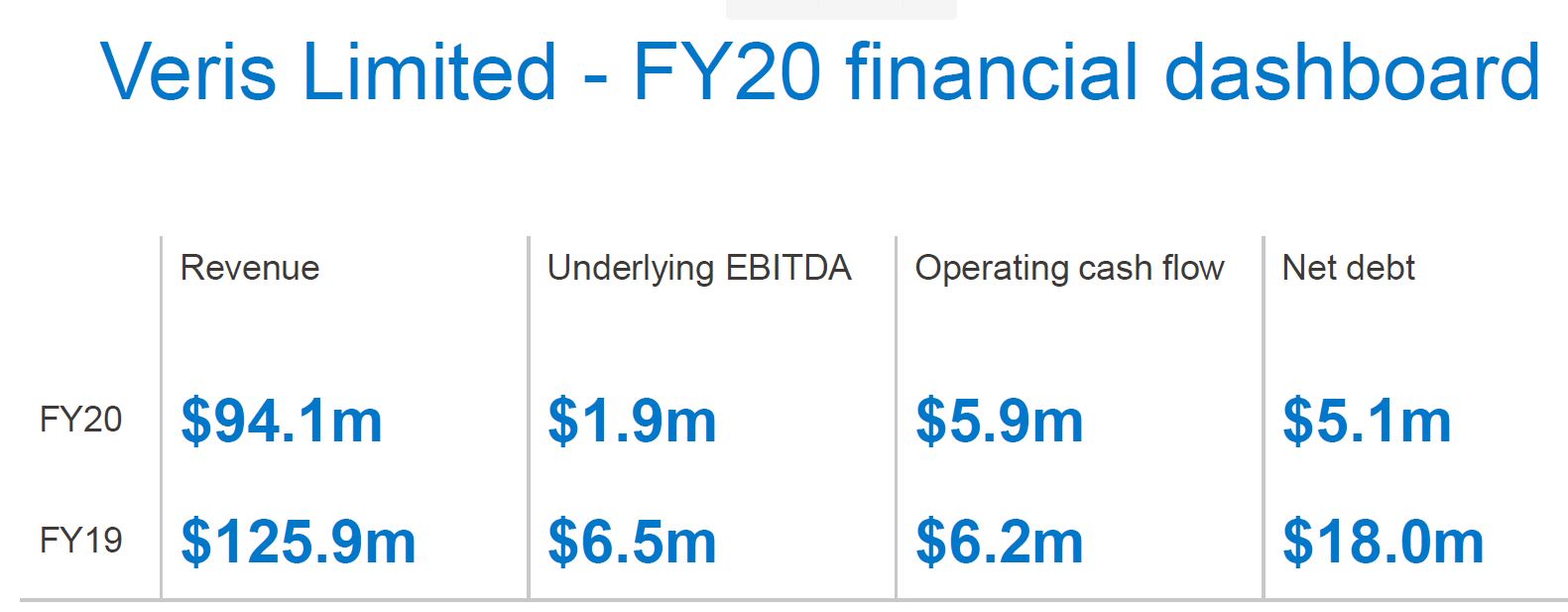

The AGM commentary

was very positive and highlights the real potential of the scaled-down

business as infrastructure work starts to build in 2021. It is clear the

business is transitioning back to profitability. (table from AGM Presentation deck)

-

The

end markets the

group serves are approximately - mining 35%, property 35%, Defence 5% and

infrastructure 25%. All have potential tailwinds over

the near and medium term.

- At the AGM

the comment was made that revenue is annualising at around $100m with

margins currently at 10% with still an underperforming

operation in NSW. A key metric is the utilisation rate which is running at

around 65% with hopes to get to 75% for the 2022 year. Using their

targeted group margins of at least ~15%, which on the current order book

could see the company make at least $10m EBITDA this year rising to $15m

in 2022.

- The balance sheet

is in reasonable shape with around $5m of net debt which is being repaid

quickly (down from $18m).

- Back of the envelope, a EBITDA

multiple of 4x 2022’s earnings values the business at $60m versus

the current market cap of $30m. These sort of numbers are dependent on delivering on their order book and maintaining their margins. So, there is scope for shares to perform if management can deliver on these targets.

- The shutdown in Victoria has also had an impact on this year’s earnings is unlikely to be repeated in 2021.

- Alongside the Veris Australia business is a smaller technology business Aqura Technology. This business is profitable and growing with some recent contract wins and reasonable margins. Revenue is around $20m with margins currently around 5%.

In Summary

Following periods of underperformance, due to poor

execution, poor management or structural issues, companies rightly need to

prove themselves again. So the share price gains are often incremental as

management can show things are back on track. We see VRS as one of those

situations. We like that they are large, operate across many states, and have

the scale to compete and win the larger contracts (refer to recent contract wins - APA, Bunnings, Fortescue and Aust Gov/Defence). This scale relies on management systems to execute, particularly when you are in a contracting business (no good winning a contract only to lose money on it). And with better

financial management, the margins can continue to improve. With the balance sheet back in order, this also reduces an element of risk.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Author. Tom Schoenmaker

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tom is a Founder and Head of Wealth Management. Since 2012, he has been running the Alpine Model Portfolios, focusing on macroeconomics and tactical equity positioning. These portfolios were initially created as a solution for "core wealth management" for Alpine's HNW clients, and are now openly available online through the website. Everything starts with the macro, and then we work back from there in terms of asset allocation and positioning for risk. We work with leading independent research providers and have a structured approach that has worked very well over time. Outside of the core portfolios, we look for opportunities in the small to mid-cap sectors of the market, where our experience can add value.

........

Disclosure - The author of this note owns shares in VRS. Wentworth/Author has not been paid any fees by VRS or any of their associated parties in relation to the publishing of this note.

This is not a research note, not personal advice or a recommendation to buy the Company mentioned (VRS) and VRS should be considered high risk and very speculative. Many risks are not discussed in this note. Nothing in this note should be viewed as personal financial advice to you, it is not written for you personally, and in no-way considers your personal situation. Whilst this note may discuss markets, macro and companies, and look to raise ideas and discussions, you should not act on the content of the note without seeking your own professional financial advice. The content is general in nature. As a general rule, you should always consult with a financial advisor prior to making any decision on buying or selling an investment. Wentworth has not independently verified information contained in this note. Wentworth assumes no responsibility to provide further updates regarding this Company.

4 topics

1 stock mentioned

Tom is a Founder and Head of Wealth Management. Since 2012, he has been running the Alpine Model Portfolios, focusing on macroeconomics and tactical equity positioning. These portfolios were initially created as a solution for "core wealth...

Expertise

Tom is a Founder and Head of Wealth Management. Since 2012, he has been running the Alpine Model Portfolios, focusing on macroeconomics and tactical equity positioning. These portfolios were initially created as a solution for "core wealth...

Expertise

Comments

Comments

Sign In or Join Free to comment